As a starting point it is perhaps interesting to stand back and look at technology in a broader sense.

Essentially technology acts as a catalyst for the formation of new industries by enabling, or opening up, new opportunities. Technology is also central to extended periods of economic growth because it spurs complementary innovation, which then enables productivity gains in the broader economy. Historically, such technologies have included steam, rail, electricity, and computers.

Eventually technical advancements slow and lead to a period of slow expansion (or decline) until the next wave comes.

Have investors therefore missed the chance to plant their flags at the top of the current cycle?...Maybe not.

Analysis undertaken by our chief investment strategist suggests innovation waves throughout history have typically lasted 60 years. The current wave, driven by digital networks, software and new media, has only been going 10-20 years. The current downturn is also one of over-capacity rather than any lack of innovation. The conclusion: while bumpy and uncertain now, investors should look to many more peaks yet to come as innovation continues to reshape economies.

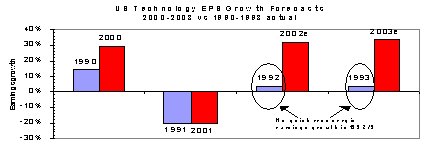

The problem is, short-term expectations are still too high (see graph).

If we review what happened in the last downturn in technology i.e. the 1990-1993 period, earnings did not rebound quickly but, as the graph indicates, forecasts for US technology company profit growth are for a rebound to 30% growth for the next 2 years. In contrast in 1992 and 1993 earnings growth rebounded to only 3-4%.

This willingness by analysts to call a substantial earnings growth recovery stems from the fact that analysts when forecasting these so-called hyper growth companies have in the past tended to under-estimate growth. Now they are over-estimating. Many also are failing to consider the real capacity that has been created by the rapid take-up of technology over the last few years.

Within the communications markets this is the most obvious. Telecom companies have been quick to build digital networks, while many new competitors have entered the market because of the new technology offering lower operating costs. There was also an abundance of capital ready to help fund these developments as investors looked for the next growth story.

And it was a good story - capacity take up was accelerating as dot coms proliferated and as the internet drove businesses on-line. Post expansion and the bursting of the tech bubble we find demand was overstated, dot-coms have disappeared and while the drive on-line continues at a fast pace, the pace is much slower. On the supply side, there is too much capacity. In the US there are now 10 long distance carriers and capacity utilisation is estimated at a mere 1%. The "build-it and they will come" is now being replaced by "marginal cost pricing" and high pricing pressure. This will, no doubt, lead to rationalisation but is negative for companies involved in supplying network components, as it could be some time before any major capacity needs to be built.

This example demonstrates that investing in technology companies comes down to the same fundamentals as investing in any other company: an assessment of potential returns, and just as in other sectors, of the risks. For technology companies, the latter is even more important as a major risk is obsolescence!

Risk adverse investors should therefore consider whether it might not be better to play the sector from the other side - the beneficiaries of using new technology. While perhaps not as exciting, it is easier to assess technology risk and productivity potential. In previous newsletters we have highlighted General Electric as one of the beneficiaries, but there are many others.

One trend we would look to take advantage of is the potential of an explosion of new consumer devices.

Just as colour TV's replaced black & white, eventually we believe the "web-tone" will replace the dial tone. With 3.0bilion devices having dial tone but only 350m with "web-tone", there is a 2.65 billion unit device opportunity to be exploited. These devices will range from your walkman, palm pilot or such device to the TV. Clearly the beneficiaries of this trend will be the manufacturers of the devices and also the PC vendors (as distributors of these products). Examples would be Sony and Intel on the manufacture side; Gateway, Hewlett Packard on the PC vendor side.

The other areas of technology innovation we like are software based, the most obvious being security and storage. But we would wait for further analyst downgrades to happen to dampen enthusiasm before targeting this area.

To assess this enthusiasm we suggest investors watch Investment Trust Technology (ITT) ratings vs. the overall Investment Trust (ITC) sector. While ITT's no longer trade at significant premiums to net asset values, the overall ITC sector trades at an average 10% discount to NAV. In our view, this premium rating most likely reflects investors buying the sector merely because the prices of most stocks have fallen significantly over the last year. NZ investors however, need only to look back to the 1980's when property companies used to command high prices based on their continuing asset revaluations. After halving during the stock market crash, many disappeared as investors came to the realisation that the growth in demand for space was unsustainable, asset values were not justified and did not always go up. Therefore just because stocks traded at higher prices last year does not necessarily mean those prices were realistic.

There will be a time to buy sector, but for now we prefer to recommend investors buy companies benefiting from the productivity gains, and wait for more rational pricing to return to the technology sector.

Where are we now? Manager views remain mixed.

Finsbury Technology, is bullish believing that the future of technology shines as brightly as ever. Dr Andrew Clark, the fund manager, feels that shrewd investors will follow the trend, not the fashion and buy quality stocks whilst they are at good prices. His view is that technology is going global and diversifying into every walk of life; in the home, the car, and the office. It is saving lives in hospitals, and the massive growth rates seen in mobile telecommunications bear witness to the allure of new technology.

A more reserved Sandeep Bhargava, manager of Fleming Technology has noted that, while valuations are looking extremely attractive in several technology and related areas he points to the NASDAQ up 30% since its low at the beginning of April. He agrees that it is time to reassess the outlook for global technology stocks and points to historical evidence that suggests that easing monetary conditions are good for stocks as the economy begins to recover and capital spending revives. And, given the usual lags between interest rate cuts and revival of consumer and business spending, he expects to see a pick up in demand for IT related products and services by the fourth quarter of this year. However, he still remains cautious and believes analyst expectations for a strong rebound in corporate earnings in 2002 are premature and warns against excessive optimism.

Brian Ashford-Russell, of Polar Capital Technology Trust concurs to an extent with this view and highlights that as investors look beyond the temporary slowdown in technology spending that has accompanied recent economic weakness, the sector should begin to recover. He refers to the sector's still unmatched capacity to generate superior earnings growth as the key driver to this recovery. However, in his recent report to shareholders he referred specifically to in the fact that the environment was still tough and that there is very little visibility of earnings, inventory levels are still high and the market still has to digest recession, over-investment in telecoms and the market's IPO excesses.

Quite clearly even the managers agree the way forward in the sector could be quite bumpy. But we still recommend investment trusts as an ideal way to hold an actively managed exposure to this part of the global equity markets. The closed-ended structure of investment trusts is particularly relevant in more volatile markets like technology as it allows the fund manager to take a long-term view of their portfolio. And, investment trusts, with their low charges, independent boards of directors, ability to gear and spread of investment risk have many unique advantages.

|

||||||||||||||||||||||||||||||||||||

| « Henderson's new tech managers outline their strategy | The nuts and bolts (or wire and solder) of tech funds » |

Special Offers

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved