CS First Boston's Peter Irwin says that 2001 was 'annus horribilis' for investment trusts, but this year looks better.

Thursday, January 17th 2002, 4:00PM

2001 was an "annus horribilis" for equity investors in general, and for the investment trust

sector in particular.

Without doubt, the year will be remembered

for the tragic events of September 11. But even without this,

followers of investment trusts would need rose tinted glasses

to look back favourably on the year in which the FTSE investment

trust Index (ITC) fell of 15.6% in NZ$ terms (19.9% in sterling

terms). This is the largest percentage fall

in the index over a calendar year since 1990. In that year, the

fall in the index was noticeably higher at 22%.

Thankfully, though it was not all gloom

and doom with a number of positive developments to look back on.

In addition, the overall state of the industry remains in good

health, with some successful new issues and increased commitment

to closed ended funds by a number of management groups.

Although

the near term outlook for equity markets remains uncertain, there is confidence that 2002 will be a better year for the investment

trust sector overall.

Key points from 2001 include:

The large fall in the ITC compared with

a decline in the MSCI World Index, in NZ$, of 12%. factors in

the underperformance of the ITC index appear to have been.

Level of gearing against a backdrop of

falling markets

Discount widening

Underperformance of UK smaller companies,

which make up a higher proportion of the ITC index than the MSCI

World. The FTSE Small Cap x IT Index fell by 18%.

Fallers:

Companies with high weightings in growth stocks and TMT lead

the declines. Fleming Technology saw the greatest

fall, down 56%, followed by two growth-orientated stock pickers

TR European Growth losing 50% and Henderson Smaller Companies

down 43%. M L New Energy, an even more esoteric technology play,

declined by 43% with Polar Capital Technology losing 36% over

the year. It may well be worthwhile keeping an eye on all these

stocks. There is no problem with any of the manager’s ability;

it was simply a situation of being in the wrong sectors. And,

as so often is the case, last year’s losers could well be

this year’s winners.

Risers:

Over the year the sector saw share price rises in 43 out of the

240 conventionally structured investment trust companies. These

included some of the emerging market specialists such as Baring

Emerging Europe, which rose 38%, and Genesis Emerging Markets,

which added 7%. Closer to New Zealander's hearts, the Australasian bets

paid off with Henderson Far East adding 40% to its price and

the New Zealand Investment Trust returning a stellar 31% against

a local index that was up a mere 8%. Surprisingly one could have

made money last in the US markets, as F&C US Smaller Companies

showed increasing its share price by 15%. Of the generalists,

2001 was Michael Moule’s chance to laugh back as Bankers

Investment Trust, up 4% the only one to show a positive return,

benefited from continued good performance of value stocks relative

to the TMT sectors. Many of the risers also saw narrowing discounts,

as investors bought into those investment trusts that performed

well.

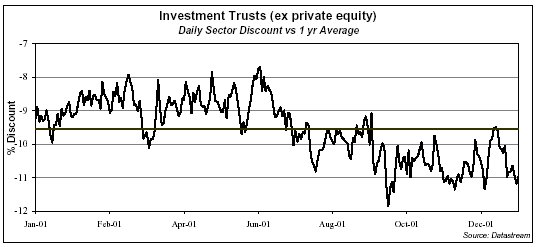

Discounts:

As one would expect, the average sector discount widened during

the year. However, the size of the widening was not as dramatic

as might have been expected given the weakness in global stock

markets this was also helped by share buybacks, which continued

over the year. The average sector discount rose from 9.2% to

10.9%. One of the largest changes was the rating on the TMT sub-sector,

where the average changed from a 16% premium to a 10.4% discount.

The European average discount moved from 6.7% to 7.8%, while

the international generalists’ average discount widened

only slightly from 11% to 11.4%.