That means in the last year, the OCR has risen 125 basis points and the economist are predicting more. But is it an effective tool to control inflation in the NZ economy?

Is the Reserve Bank steering the New Zealand economy with only one paddle?

I ask this because the RB chooses not to exercise control over the exchange rate and it has very little control over the mid to long term fixed interest rates (as these are effected by the international interest rate market) so all that is left for it effect through its adjusting the OCR is the 90 day bill rate and the flow through to the floating rates and the 6month and one year fixed rates.

Just look at ANZ’s published rates at time of writing.

Floating 6 mth 1 yr 2 yr 3 yr 4 yr 5 yr ANZ 8.5 % 7.75 % 7.75 % 7.75 % 7.75 % 7.75 % 7.75 %

My borrowing clients merely fix for the best rates around the two years and wait for the Reserve Bank to reverse its heavy handedness as commented on by the ANZ economics departments publication dated 28th May 2004 commenting on the poor control exercised by the Reserve Bank of New Zealand.

“..the market is also wary of the undulating nature of the OCR since 1999. Up in 2000, down 2001, up 2002, down 2003, up 2004…bets anyone on 2005”

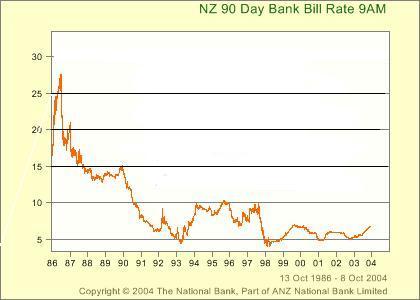

This is depicted in graph form below

Background From about 1989 to March 1999 the Reserve Bank used the Monetary Conditions Index (MCI) to control the economy. It required balancing the exchange rate against interest rates. If one went up the other had to go down. In fact, countering a falling currency with rising interest rates during the 1998 Asian crisis pushed New Zealand into a recession and led ultimately to the abandonment of the MCI as a control mechanism.

The MCI could be seen as New Zealand’s economic accelerator. A lower TWI (The trade-weighted index (TWI) is a measure of the value of the New Zealand dollar (NZD) relative to the currencies of New Zealand's major trading partners. The TWI is the Reserve Bank's preferred summary measure for capturing the medium-term effect of exchange rate changes on the New Zealand economy and inflation. www.rbnz.govt.nz) meant cheaper New Zealand exports and rising demand for our products. This stimulated economic activity and so interest rates were increased to put brakes on the economy and keep inflation in check.

The OCR The OCR replaced the failed MCI and the Reserve Bank hoped this would be a more effective control mechanism (maybe it would be if used effectively, see comment above). The market uses the OCR and it’s anticipated direction to price the 90-day bill rate (the interest rate that is charged on money borrowed or lent for 90 days) The market sets the 90-day bill rate and the market moves this rate in the direction it anticipates the OCR going. The rate at time of writing is 6.68 % so the market is anticipating future rate rises. With the banks wishing to maintain their margin of 2 % over their cost of funds, floating housing rates will probably rise to around 9 % or higher by the end of the year.

With Mortgage Brokers having an impact in placing mortgages at somewhere between 22 to 30 % of the total mortgages written in New Zealand and the competition of non-bank lenders willing to accept smaller margins this will probably help to keep the floating rate generally a little below what the main stream banks would like and are used to getting away with.

So the OCR has risen 125 basis points in the last year, with the average household debt-to-income ratios in New Zealand now at around 130%, about twice as high as a decade ago the impact of any OCR increase now in theory would have double the effect in slowing the economy. Couple this with the highest interest rates in the OECD leading to our currency appreciating and the dampening effect on demand on our exports and inbound tourist, One could argue that the economic tightening has already gone to far.

CPI Monetary control exists because of the inflation bogey, i.e. when the cost of something keeps rising and is measured by the Consumer Price Index. If that was a true measure and took into account everything we have to pay for it may have more relevance. I advocate that it should measure the cost of living and take into account Government fees, taxes, rent, cost of money and anything else that rises and takes money out of my pocket. The Government and Reserve Bank however have chosen to distort this to meet their own ends.

MER Dr Brash in his old role (Governor of the Reserve Bank) made the following comment in his address to the Counties Kiwifruit Growers Association in 22 August 1997

“But of course neither we nor any other central bank can control the mix of monetary conditions. In other words, we can tighten monetary conditions, but we can not determine whether that tightening takes the form of an increase in interest rates with little or no increase in the exchange rate; or an increase in the exchange rate with little or no increase in interest rates; or an increase in the exchange rate with a decrease in interest rates; or an increase in interest rates and a fall in the exchange rate. The mix depends on the perceptions and reactions of a great many people, here and abroad, and indeed on what other central banks are doing or are expected to do.”

Confused by his comments? That is not surprising and it is no wonder the Reserve Bank has not proved particularly successful in controlling inflation in NZ either, when it chooses to only manage one side of the mix. Using only one oar to steer a ship is so much more difficult than having a rudder at the back or at least using two oars.

One should ask why we do not have a managed exchange rate and review the rates at the same time the OCR is reviewed. Malaysia handled the Asian currency crisis extremely well by fixing its currency and China has had its currency fixed to the US dollar for a number of years. New Zealand is such a small player on the world stage I believe we can thrive with having a Managed Exchange Rate. The missing other Oar possibly?

I asked the Reserve Bank this back in February this year and got the following reply

“Would that not lead us back into the world of attacks on the currency as we saw after the 1984 election whenever a devaluation is potentially in the offing? Not a good look I would have thought?”

If it was managed, how could it be attacked I wonder? I did not pursue the point.

If the Reserve Bank choose to manage the currency at say around USD 60 and AUD at 85 or around our historical averages would that not have a positive effect on our exporters who create wealth for New Zealand. Couple this with the use of the OCR all business could plan ahead with a lot more certainty.

Summary While the New Zealand economy is humming along, (and it looks like this will continue for quite some time yet), the pressure on production capacity, skilled staff and other resources will translate into upward pressure on inflation (wages go up in order to secure the reducing amount of skilled labour). The Reserve Bank has a brief to keep inflation under 3 % and to date while the inflation rate has been relatively well maintained by the Reserve Bank, it has not managed to control the growth of the New Zealand economy very well and the OCR has been turned into a Yo-Yo.

The Reserve Bank also has in it’s collective thinking that New Zealand can not grow faster than 3 % a year without inflation getting out of hand and makes it’s monetary management decisions based on this untested theory.

If we look at the last 3 years of growth in New Zealand, thankfully the average would be well ahead of the plodding 3 %. I would have thought that inflation has not raced away and damaged New Zealand’s terms of trade or competitiveness.

I ask that the RBNZ let the economy grow and use two oars to manage growth and inflation.

David Weusten is a regular contributor to various publications and brings with him over 25 years experience in the finance industry, both in NZ and overseas. He has been published in the Sunday Star Times, The Southland Times, the New Zealand Franchise Magazine RD1.com and other publications. He would be happy to answer any questions you may have related to Business, Finance, Franchising and Banking. Email him at dweusten@fspnz.com. If you would like to know more about his company, Financial Service Providers visit their website www.fspnz.com.

Special Offers © Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved

« New broker association being born Slowdown may make banks love brokers: AMBL » Commenting is closed

www.GoodReturns.co.nz