The Co-operative Bank chief executive Bruce McLachlan says there is significant discounting happening amongst lenders.

“Rate cards are quite high in my view,” he says.

Borrowers need to be asking for the best possible deal when they take out a loan or refinance an exiting one.

“The poor old customers who don’t challenge are missing out,” he says.

ANZ economists agree competition has stepped up in the past few weeks.

“All power to the borrowers!”

“Competition is more aggressive in the Auckland and Christchurch area; precisely those regions that are the house price hot-spots,” they say in the latest Market Focus report.

One of the reasons is that lenders have got their minds around the Reserve Bank’s lending restrictions and have realised there is room to increase their activity in this area.

McLachlan says just under seven per cent of The Co-operative Bank’s lending is in the low equity space and he would like it to be around 8%.

ANZ says: “The initial knee-jerk reaction post the implementation of the 10% limit on high LVR lending partly reflected uncertainty surrounding how the swathe of pre-approved loans would roll off. Six months on and financial intermediaries have managed that pipeline so high LVR lending can tick back up closer to the 10% threshold.”

The other reason is that a sizable chunk of fixed rate mortgages rolling off at present which presents an opportunity to gain market share.

McLachlan is critical of the discounting happening in the market and says The Co-operative Bank does minimal discounting and tries to be “transparent” with its pricing.

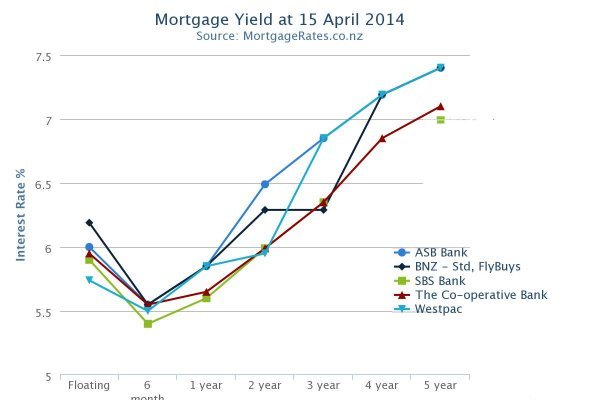

How they compare

The following graph illustrates the differences in pricing at the moment. For practical reasons we have selected a sample of lenders rather than trying to graph all of them.

| « Welcome Home Loans to expand | Economists: Expect another increase » |

Special Offers

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved