by Harbour Asset Management

Overall capital market volatility may increase in the near term from low levels as slight increases in inflation rates will allow central banks to unwind low official rates. Capital markets have weathered the transition of the removal of US quantitative easing actions relatively calmly, with European quantitative easing actions providing some offset. At this point in time central bankers are rightly taking a cautious stance in ‘normalising’ official interest rates, with economic data remaining mixed and the revival in inflation not wide spread. But a large amount of monetary stimulus has been removed – meaning even small interest rate changes have the potential to destabilise parts of the capital markets.

The valuation of low volatility, yielding parts of the equity market, that have benefited from fixed interest investors moving up the risk curve over the last three years to enhance their portfolio income yields, are stretched versus historic valuation multiples. The movement into low volatility, yielding equities globally over the last three years has been one of the largest capital market strategy changes seen in recent times. But against yield on fixed interest assets low volatility, yielding equities continue to provide an attractive yield enhancement. These bond proxy sectors may not receive the same degree of investment inflow going forward if fixed interest rates start to creep, even modestly, higher.

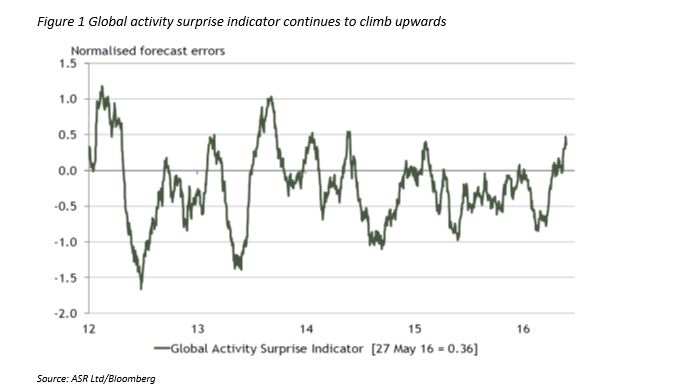

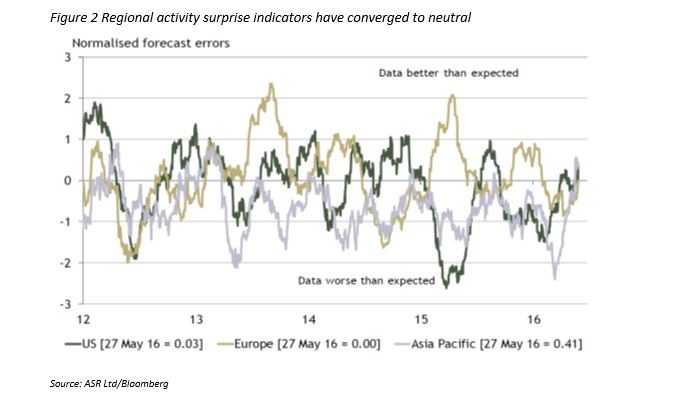

Global economic data remains stronger than many may have expected. As shown in figure 2, global activity surprise indicators produced by Absolute Strategy Research, who provide independent research to Harbour, suggest that global activity may move in to a modestly positive period.

Importantly, as shown in figure 2, the improvement in activity surprise is occurring across all regions. So while the improvement in activity may not be exciting (which is good, given that excitement would be bad in a world where global monetary policy settings are positioned for low inflation), it currently has a broader base than it has done over the last year.

Events such as Brexit and the US Federal elections may also increase near term market volatility as they increase investor uncertainty. While we need to be aware of the potential impact of such events on individual companies, our focus remains firmly on sectors and stocks rather than any event driven view. Such events often create attractive medium term investment opportunities.

Even though the local equity market may be fully priced, there are wide valuation dispersions between sectors and stocks. Investors, particularly passive index following investors, are paying a premium for companies with perceived earnings and dividend certainty – even where there are very real industry structural change risk, such as is the case with Sky Television.

In comparison investors are unwilling to pay for growth which, may actually be more idiosyncratic but requires a degree of near term patience as companies implement strategies, such as is the case for emerging growth companies Vista, a2 Milk and Pacific Edge.

In our view while market volatility may spike higher in the near term, and valuations are full, the New Zealand and Australian equity markets are likely to continue to keep grinding out positive returns in the near term. The latest result season was ‘boring’, with few big profit warnings, at a time when boring is good. Local company balance sheets are appropriately conservative, providing some protection should economic conditions deteriorate. And for now passive yield hungry investors keep pouring money into relative earnings certainty New Zealand and Australian stocks.

Growth and quality

We continue to focus on sustainable growth and quality. Our research shows us that in sideways or weak equity markets quality companies tend to out-perform the broader market. As overall investor confidence falls, companies with challenged operating fundamentals are exposed to the risk of capital being withdrawn by banks in the form of higher debt costs (or non-debt availability) or by equity investors in the form of a higher cost of equity funding.

Our research also shows that growth sectors perform through most cycles – but investors need to be patient. Growth rates for structural change beneficiaries such as those in the healthcare and technology sectors and beneficiaries of changing demographic trends, are often underestimated by investors who are caught up by short term equity market ups and downs.

Andrew Bascand, Shane Solly, Craig Stent

This column does not constitute advice to any person.

www.harbourasset.co.nz/disclaimer/

Important disclaimer information

| « A view of Brexit, from London | NZ equity management: Will the tight-five continue to dominate play? » |

Special Offers

No comments yet

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved