Changes to banking rules are set to have a meaningful impact on New Zealand’s fixed interest market in 2019

Tuesday, February 5th 2019, 11:01AM

by Harbour Asset Management

Simon Pannett

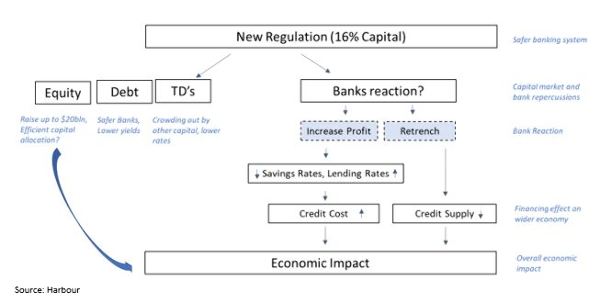

A proposed rule forcing banks to hold more equity capital will make the banking sector more stable, however it will come with a raft of second round impacts. Chief among those will be the impact on banks’ willingness to lend. This is what we are watching most closely;

Separately, we may see explicit preference for depositors over bond-holders in the event of default. If enacted, this may partially offset the credit benefit on senior unsecured paper of higher capital levels; and

We are also likely to see issuance of a new high-quality mortgage-backed security type.

This article examines these three changes.

I. Greater equity shores up banks, but secondary impacts abound

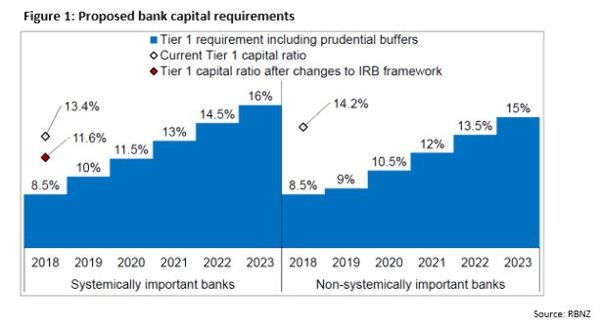

NZ registered banks are currently required to hold equity capital equal to at least 8.5% of their risk-weighted assets. The RBNZ is proposing to increase the required minimum to 16% for large banks and 15% for their smaller counterparts. The proposal will be phased in over five years. The RBNZ is also proposing that the larger banks use more conservative methodology in calculating capital ratios, such that the current stated average tier 1 equity ratio of 13.4% would reduce to 11.6%.

To put those numbers in perspective:

Against a backdrop of strong profitability, underpinned by very low loan losses and robust credit growth, the big four NZ banks have been increasing capital ratios at an average rate of 0.2% p.a. over the last few years. This has been achieved while paying around two-thirds of their profits in dividends. Under the capital review proposal, they will be required to increase the rate of capital build to over 1.0% p.a.

Estimating the dollar amount of capital required relies on assumptions of profitability, lending growth and lending composition. The RBNZ estimate suggests $12bn equity will be required to be raised, something they think is achievable if the big four banks reduce their dividend pay-out ratios to 30%. The RBNZ’s analysis assumes the banks are also able to replace their current alternative Tier 1 capital. If they are unable to do so, a further $6bn in capital above the $12bn estimate would need to be raised. Other broking analysts’ models point to a higher equity requirement than the RBNZ’s modelling; CSLA estimates $17.6bn is likely to be required.

The 2014 Murray inquiry into Australia’s financial system recommended that, in a small open economy reliant on offshore funding, it was important that the banks were “unquestionably strong”. APRA has recently defined ‘unquestionably strong’ as a capital ratio of 10.5%. Comparing capital ratios is fraught given different methodologies and accounting standards, however UBS estimates that 16% will place NZ’s banks as the highest capitalised in the world on a like-for-like basis.

Any way you look at it, 16% is a big number.

Why so big? Some see this as an opening gambit in what will become a negotiation with the banks. The RBNZ may change its stance, but we instead see it as the RBNZ’s true position, based on cited evidence. The RBNZ has set a very low risk appetite for bank failure given its view on the ensuing economic and societal costs. Capital has been set on the theoretical expectation that a bank failure will occur once every 200 years.

We liken banks holding significant capital to a nation’s electricity sector having spare capacity to protect against a blackout. Avoiding a blackout is of value to society. However, investing the capital necessary to build spare capacity comes at a cost. The capital invested in the banks could be put to alternative uses. We expect there to be significant political discourse on this matter, as high bank capital may crowd-out alternative investment uses of that capital.

Likely impacts:

Credit Positive: Equity capital protects lenders from losses and therefore the proposed changes are positive for bond holders and depositors. We think it is likely all banks will receive a standalone credit rating upgrade. This won’t impact the credit rating of securities issued by the big four banks as the securities already receive issue rating uplift from their parents. This serves to highlight that there are limits to the credit positive of the proposed changes, given the major banks derive some support from their parents. However, provided ratings agencies don’t offset the positive of higher capital with a lower presumption of support from the NZ Government, the smaller banks appear likely to have the credit ratings of the securities they issue upgraded.

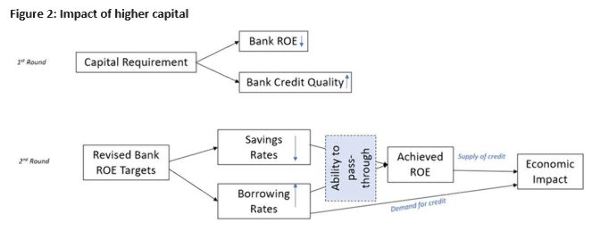

Beyond the obvious first round impacts, there are likely to be second order impacts as bank investors set a new return on equity requirement to reflect the banks’ lower risk profile. The banks’ ability to recoup this via higher net interest margins, as well as any constraints on capital availability, will influence the impact on credit growth in the economy.

Lower deposit rates for savers: With more equity, and potentially less lending (as explained below), there will be less need for the banks to raise debt funding. Another rule requires a portion of banks’ funding to be “sticky”. This ‘core funding’ includes both equity and deposits. Given deposits can be expensive funding for banks, we suspect the reduction in need for funding will be felt most in deposit markets where banks will have less need to compete for funding and hence deposit rates may fall. Additional to the reduction in supply, the banks will be safer entities and bond investors may require less compensation for their risk.

Higher mortgage & lending interest rates for borrowers and lower bank profitability: Having to share the profit pool around more equity will diminish the rate of return on that equity. This will be partially offset by lower borrowing costs (as above), but it is also likely that banks will attempt to expand the profit pool to restore ROE by increasing lending rates. The extent to which banks can recoup lower ROEs depends on competitive dynamics. A wide range of studies estimates that each 1% increase in capital increases lending rates by between 2bps & 15bps (0.02-0.15%). The Reserve Bank itself estimates a 6bps (0.06%) increase for each 1% increase in capital. If they cannot recoup profitability, there is a possibility the Australian banks sell their NZ subsidiaries.

Reduced lending growth: As above, lending rates are likely to increase. This will reduce demand for credit. But what is vitally important, and unknown at this stage, is the impact on supply of credit. If banks simply raise more equity (increase the numerator), the economic impact will be much more benign than if they instead shrink their balance sheets (decrease the denominator). We will be concerned about the economic impact if Australian banks are unwilling to raise equity in NZ or are unwilling to reduce dividends to their shareholder base (such a significant reduction in dividends from their NZ subsidiaries in order to organically build capital implies dividend cuts at the Australian parent level, absent a capital raise). While we expect lobbying from the banks in an attempt to dissuade the RBNZ from fully implementing the proposed changes, their response is what we will be watching closest. While the subsequent reduction in economic activity is a relatively less studied subject, we note the RBNZ’s expectation of a mere 3bps reduction in GDP is very much at the low end of estimates in the academic literature we have reviewed. While the long-term impact on economic output appears likely to be modest, and indeed with a safer banking system, downturns are likely to be less severe, our attention is on the adjustment period and whether banks respond by reducing lending appetite. If they do, there could be material impacts on economic growth and therefore monetary policy. We think it is premature to be judging the impact at this juncture.

Composition of lending: Overseas experience has shown that increases in capital lead to a larger reduction in lending to the riskier sectors such as commercial property and sectors where banks earn lower returns such as syndicated loans to corporates. There is also some evidence that banking sector competition is reduced when a transition to a higher capital ratio is mandated.

Other investment crowded out: There is an alternative use for capital invested in the banking sector. This opportunity cost will not be particularly acute to the NZ economy if it comes in the form of lower dividends to the banks’ Australian parents, however if it comes in another form it may instead have been invested in other productive assets.

A possible end to Tier 2 debt: With a significant increase in equity capital to protect senior creditors, the RBNZ is consulting regarding whether there is a continued regulatory need for the existence of subordinate debt. If the RBNZ decides that this layer of capital is no longer necessary, existing Tier 2 capital securities may benefit from their scarcity value as rare high-yielding securities in the New Zealand market. Harbour evaluates credit securities based on their return for risk, and we are therefore unlikely to purchase securities based on demand dynamics alone. In Australia, APRA has recently announced a proposal to substantially increase the amount of Tier 2 capital issued by banks. Most observers expect this substantial increase in supply will result in wider pricing. If such an adjustment is made, we will be appraising this for our funds whose mandates allow them to take advantage of such a cross-border opportunity.

II. Depositors to rank ahead of bond holders?

The RBNZ is in the early stages of consulting on NZ’s bank creditor protection framework. Unlike the bank capital proposal, we think this is an area where the bank is yet to formulate a firm view. One of the options, however, is to explicitly and legislatively favour depositors over bond holders in the event of bank failure.

Likely impacts:

Credit negative: Depositor preference would have a negligible impact on the probability of a bank defaulting, but it could significantly impact bond holders’ losses in the event of default. We expect this will most likely result in an immaterial impact on senior unsecured bonds in times of normal bank health but, as a bank’s creditworthiness deteriorates, senior unsecured bond holders will progressively have to factor in a smaller residual value. Therefore, senior bonds will likely trade with a greater sensitivity to economic health; moving a step closer to current Tier 2 debt instruments. As a positive offset, such a change would make the banks less likely to experience a run on deposits and therefore liquidity would be improved.

Credit ratings likely unaffected: Depositor preference is explicit in the majority of jurisdictions, including in Australia where deposits are assigned the same credit ratings as senior unsecured bonds. While less likely with current settings, it is possible in future deposit and bond ratings could depart for lowly-rated banks (as the chance of failure grew higher).

III. RMOs: a new high-quality mortgage-backed security

Since the GFC, banks have been able to post pools of mortgages with the RBNZ. These pools, or, ‘internal securitisations’, were ring-fenced but not issued as publicly-traded securities. While these securities can create bank liquidity (funding to enable banks to borrow short and lend long), they have a number of limitations:

There was very little standardisation and no price discovery meaning that the RBNZ could potentially have been exposing the Crown’s balance sheet to a higher contingent liability than desired; and,

To protect against the above, the RBNZ has hitherto imposed a significant haircut on accepting these securities, meaning that $1.23 worth of mortgages had to be posted for each dollar of assets recognised. This has limited the securities’ efficacy;

Owing to their low cost of issuance, there was little incentive for banks to issue public market securities and thus facilitate deeper capital markets.

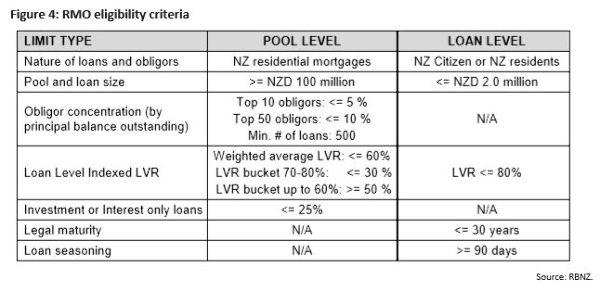

The RBNZ is finalising a review which is likely to see internal securitisations replaced through time by publicly-issued securities to be known as Residential Mortgage Obligations (RMOs). After consultation the RBNZ has proposed a relatively straightforward format for these securities.

The bank’s primary aim has been to reduce the Crown’s contingent liability by creating and facilitating a liquid market of transparent, high-quality securities. Indeed, the requirement for a minimum of 10% subordination or a AAA-rating at the senior tranche ensures a very high-quality security. By way of comparison, it is likely that the ratings agencies would require just 4% subordination for a AAA pool of prime NZ bank mortgages; in Australia the big four banks typically top-up this subordination to 8% for AAA tranches. The RBNZ has strict stipulated standards for mortgages eligible to be included but, importantly, these standards are not so strict in our opinion as to result in cherry-picking of the best mortgages at the expense of senior unsecured creditors. The banks are required to retain skin in the game by holding the first loss piece comprising a minimum of 8% of each issue.

Likely impacts:

Alpha opportunities: A new high-quality security type will provide active NZ fixed-interest managers greater scope to add value.

Increased funding costs: Compared with the inexpensive status quo, RMOs will increase bank funding costs. In Australia, as with many other markets, AAA mortgage-backed securities, offer investors higher yield than lower-rated unsecured obligations of the same bank. In part this can be explained by the relatively lower liquidity of securitised debt. RMO liquidity remains to be seen, however, the RBNZ has stipulated several measures aimed at enhancing liquidity. In part, greater spreads reflect an enduring stigma towards securitised debt following the GFC. This increase in funding costs will likely be, at least in part, passed on to borrowers, but given RMOs will likely constitute only a small amount of banks’ total funding (less than 5%) we anticipate the overall impact will be minimal.

Competitive impacts: There are fears that the new asset class may crowd-out further development of NZ’s nascent non-bank mortgage sector which increases mortgage competition and helps to serve a wider pool of borrowers. This sector is more meaningful in other countries. However, it is possible that RMOs encourage a wider pool of investors to invest in mortgage-backed securities.

What we are watching

We have spared readers numerous other nuanced impacts; such as the effect on offshore funding and hence the cost of hedging. While all three pieces of the puzzle are yet to be fully shaped, of most interest to us is the impact of higher capital on bank lending. This is difficult to estimate at present; however we deduce the Reserve Bank does not think it will have as large of an impact as does the balance of academic literature we have reviewed, and thus we see the risk to the economic outlook as skewed to the downside.

By: Simon Pannett, Director & Senior Credit Analyst

This column does not constitute advice to any person. www.harbourasset.co.nz/disclaimer/