Which KiwiSaver funds will weather the currency war?

It’s important to understand how different KiwiSaver Schemes manage foreign currency within their international share exposure. Michael Lang explains.

Monday, September 2nd 2019, 1:39PM

by Michael Lang

Michael Lang

Foreign currency movements have again been in the news with the United States Treasury labelling China a currency manipulator. These movements can also have an impact on clients’ KiwiSaver returns. This is dependent on how a Scheme’s manager treats the foreign currency exposure they get when purchasing international assets.

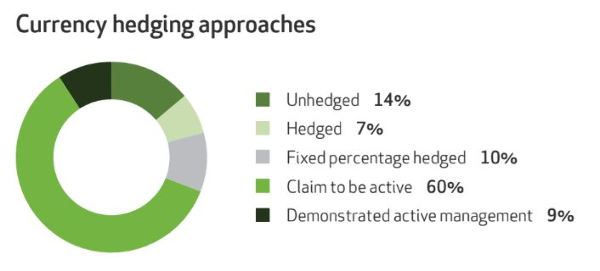

To understand how different KiwiSaver Schemes manage foreign currency within their international share exposure, we reviewed 77 KiwiSaver funds which have an international share exposure of greater than 40%. Information on these funds was sourced from their Fund Updates and their Statement of Investment Policy and Objectives (SIPO).

KiwiSaver Scheme managers treat foreign currency exposure in one of four ways. First, they can do nothing and when they purchase international assets, just hold those assets in foreign currency until they are sold. This is what the industry refers to as unhedged international assets.

The downside of this approach is evident. If the foreign currencies your KiwiSaver Scheme assets are denominated in collapse, so too will the value of your KiwiSaver investment. Eleven of the 77 KiwiSaver funds we reviewed followed an unhedged approach. Should the New Zealand Dollar recover, and trade at US$0.80 as it did from 2011 to 2014, these funds would underperform their peers by around 18%, all other things being equal.

Second, a manager may choose to permanently hold your investment in New Zealand Dollars, even when investing abroad. This is done by hedging all foreign currency exposure back into New Zealand Dollars. Investors receive the return generated on the assets they hold, for example shares in Amazon or Nestle, and forego any gains or losses from currency movements.

Third, your manager may decide there is merit in a bit of both and establish a policy of hedging a fixed percentage of your foreign currency exposure. A common approach is to hedge 50% of the exposure. This is a “point of least regret” approach. The manager is never wrong, but then neither are they ever right. The fixed portion approach is currently used by eight of the 77 KiwiSaver funds reviewed.

The fourth approach is for your KiwiSaver Scheme manager to actively manage your currency exposure. This is the most popular option with 53 of the 77 KiwiSaver funds reviewed saying they follow an active currency management approach.

Whether managers are truly active or not is difficult to judge. A number of managers outline large ranges, for example 0 – 100%, within their SIPO, but when looking at Fund Updates they only seem to vary their currency exposure by 5 – 10%. Other managers outline large ranges and a target exposure, but do not disclose their foreign currency exposure in their Fund Updates, making analysis difficult.

Some managers claim to be active but utilise external fund managers that have both hedged and unhedged options and use this to manage their currency exposure. To change their exposure, they change the external fund they access. This is not the same as active currency management, as we define it. These managers are not able to take a view on a specific currency, for example, be unhedged against the British Pound but remain fully hedged against the United States Dollar.

Few managers seem to have both the skills and will to implement their views in enough size to make a difference. If a manager is successful in adding value through active currency management, they provide their clients with another source of returns, and one that is independent from share market returns. Our analysis suggests Fisher Funds, QuayStreet Asset Management and NZ Funds all fall within this category.

Being hedged, unhedged or partially hedged can have a big impact on the returns a KiwiSaver member receives from their international assets. Over the three years to 30 June 2019, the global share unhedged index returned around 13.9% p.a. compared to 11.9% p.a. from a hedged index.

Active currency management can mitigate the difference between these two indices. For example, NZ Funds added around 1.2% p.a. to the return of its KiwiSaver Growth Strategy through active currency management over the same period.

Which strategy suits you and your clients will depend on the circumstances. Demonstrating to clients your knowledge of the different styles of currency management is invaluable.

Michael Lang is Chief Executive at NZ Funds and a member of the NZ Funds KiwiSaver Scheme. New Zealand Funds Management is the issuer of the NZ Funds KiwiSaver Scheme. A copy of the latest Product Disclosure Statement for the scheme is available on request and at www.nzfunds.co.nz

Michael Lang is Chief Executive at NZ Funds. New Zealand Funds Management is the issuer of the NZ Funds KiwiSaver Scheme.

| « Financial advisers want KiwiSaver to get SMarT | FSC KiwiSaver overhaul: Boost access to advice » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |