How active is your KiwiSaver manager?

Active v passive – a popular discussion topic. Michael Lang discusses the features and benefits of both options.

Tuesday, February 25th 2020, 8:00AM

by Michael Lang

Michael Lang

FMA ISSUES REQUEST FOR INFORMATION

Late last year, KiwiSaver managers received a request for detailed financial information on the investment management of the KiwiSaver funds that they are responsible for.

Initially this request came from a private organisation, but was followed up shortly afterwards by a more formal email from the Financial Markets Authority (FMA). The purpose of the exercise? To determine how active each KiwiSaver manager is.

IS ACTIVE MANAGEMENT NOW A CRIME?

The short answer is no. Worldwide, the investment management industry has long debated the merits of active management (managers actively altering asset allocation, managers and securities) versus passive management (a more static mix of assets, managers and securities, the allocations of which are determined by an index).

Neither form of asset management is wrong and, in NZ Funds’ view, both have merit.

WHAT ABOUT CLOSET INDEXING?

Again, the short answer is no. Closet indexing is the practice of having the mandate to make active decisions, but in practice following an index very closely.

Many institutional mandates, used in the management of large sums of money, put constraints on the managers to ensure the funds do not deviate too far from an agreed index. This is a valid and prudent asset management approach.

What may be misleading is marketing a fund as active (or passive) when the opposite occurs in practice.

For example, a manager could attract investors to an actively managed higher fee fund, and then only provide lower cost, passive management, pocketing the difference. Late last year, the regulatory authority in the United Kingdom fined a large fund manager for doing just that.

WHO IS ACTIVE AND WHO IS NOT?

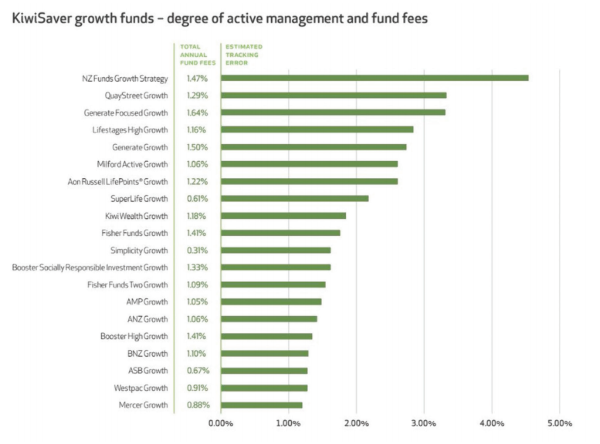

How active or passive a KiwiSaver manager is can be estimated by calculating how much their investment performance deviates from an index. This measure is called a tracking error. The lower the tracking error, the closer the fund is likely to perform to its index.

In the attached table, NZ Funds has estimated selected KiwiSaver growth funds' tracking errors using the funds’ disclosed performance and target asset allocation.1

The data shows NZ Funds, QuayStreet and Generate have been more active than their peers and on average charge more as a result.

In contrast, the major banks and larger institutional managers like AMP and Mercer have both a lower tracking error and a lower management fee. Booster’s High Growth Fund is an interesting exception.

A FINAL WORD ON FEES AND STYLES

The difficulty with comparing degrees of activeness with levels of members’ KiwiSaver fees is that fees go to pay for a lot more than investment management. For example, for the same annual fee some managers are providing access to financial advisers, financial planning software, research on responsible investing, and superior client communications and service levels, while others are not.

These additional services may be of considerably more value in helping clients achieve their long-term financial objectives than whether a manager is active or passive, or the degree that their fees are marginally higher or lower than a competitor’s.

Source: FMA, FE Analytics, Bloomberg. Total annual fund fees sourced from September 2019 fund updates. For more information on indices used and calculation methodology, contact NZ Funds.

1. The tracking error calculation is an estimate only. The tracking errors are calculated against a proxy market index using historical monthly data for three years to September 30, 2019. An otherwise passive manager, like Simplicity, may exhibit a higher than usual tracking error due to month end pricing times and dates, the choice of asset class indices in the calculations, and assumptions about currency hedging ratios, amongst other things.

Disclaimer: Michael Lang is Chief Executive of NZ Funds and his comments are of a general nature. New Zealand Funds Management Limited is the issuer of the NZ Funds KiwiSaver Scheme. A copy of the latest Product Disclosure Statement is available on request or by visiting the NZ Funds website at www.nzfunds.co.nz.

Michael Lang is Chief Executive at NZ Funds. New Zealand Funds Management is the issuer of the NZ Funds KiwiSaver Scheme.

| « Generate offers compensation | FSC questions fossil fuels decision » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |