Is default status a gravy train?

Michael Lang compares default and non-default KiwiSaver investment options.

Thursday, June 25th 2020, 6:20PM  2 Comments

2 Comments

by Michael Lang

Michael Lang

Last month, we questioned why the New Zealand regulatory environment 'gifts' billions of dollars of Kiwi savings to only nine of New Zealand’s 23 KiwiSaver managers, when all managers must demonstrate they are worthy of managing the public funds.

We showed that few of the default managers selected had New Zealandowned parent companies. Additionally, few of the managers selected specialised exclusively in funds management. And finally, we questioned whether, with hindsight, the managers which were

chosen had proven to be more stable and more compliant than the other managers in the market.

This month we examine what happens to the clients who are allocated to nine of New Zealand’s 23 KiwiSaver managers, and ask again whether awarding a selective group of managers monopoly default status is really in New Zealanders’ long-term interests?

Under the current KiwiSaver rules whenever a new employee joins an employer, they are automatically enrolled in KiwiSaver unless they are already a member. Where the employer has not proactively selected a KiwiSaver provider, which few have, the new employee

is allocated to one of the nine default providers at random and invested in their default fund.

According to a Ministerial press release dated December 7, 2006, one of the criteria by which default providers were selected is “competitive fee levels” so unsurprisingly, the fees in default funds are particularly low. However, this appears not to unduly impact the

profitability of default managers as many default members do not remain invested in the default funds for long. They bounce on into higher fee funds, in many cases operated by the same manager as their default fund.

By our calculations, approximately 68% of default members have subsequently made an active choice about their KiwiSaver fund. This makes sense, as the Government has mandated that all default funds must conservatively invest holding no less than 80% in cash and income assets. As a result, default funds are rarely the best place for members to invest over the long term.

This begs the question, if default members are going to bounce out of default funds into higher fee-paying funds over time, does the regulator look at the competitiveness of the default funds’ fees (which would be short-sighted), or the competitiveness of the fees charged across all the KiwiSaver funds the same manager offers (which would make more sense)?

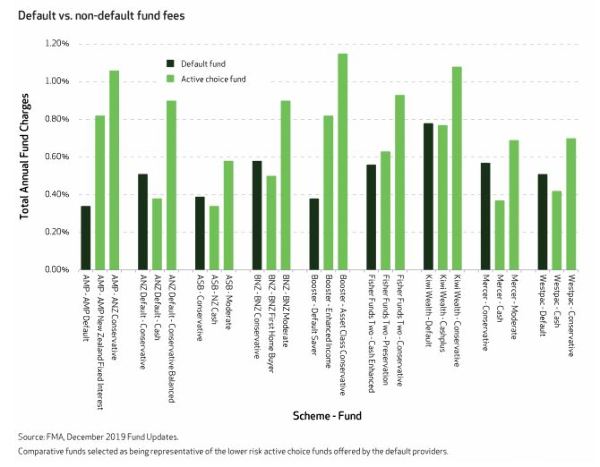

The degree to which default fund managers mark up the fees in their non-default funds is therefore of public interest. The graph below shows that in almost all cases, default managers charge KiwiSaver members more if they move to a non-default fund. The additional fee is often associated with a meaningful increase in growth exposure (and as growth assets are more expensive to purchase and manage than bonds and term deposits this makes sense) but in a select number of cases, members who switch receive little or no additional growth but a significantly higher fee.

Will the same thing occur in the newly proposed “balanced default funds” regime? Will members end up being switched out of balanced default funds into funds managed by the same managers, with the same or similar asset allocation or a lower exposure to growth

assets, but with markedly higher fees?

One would hope not but fear so. History teaches us that government mandated monopolies rarely deliver better long-term results than well supervised competition. It is therefore time that managers, advisers and investors, advocate for a level playing field instead

of a sloping one.

Michael Lang is Chief Executive of NZ Funds and his comments are of a general nature.

Michael Lang is Chief Executive at NZ Funds. New Zealand Funds Management is the issuer of the NZ Funds KiwiSaver Scheme.

| « Time for financial advisers to step up on KiwiSaver | KiwiSaver sector slams National proposal » |

Special Offers

Comments from our readers

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |

I think that the bigger issue is that only 68% of people have made an active choice. Providers seem to be doing a "good job" if they manage to convince 15% of their default customers to make an active decision every year.