Source: JP Morgan Chase

by Generate KiwiSaver

By Greg Smith

After a period of heightened geopolitical tension and market volatility, global equities rebounded sharply in April, with the MSCI World Index rising 9.5% in US dollar terms - its strongest monthly gain since November 2020. Indices such as the S&P500 and Nasdaq have also been posting new record highs in May.

For those who remained invested through the uncertainty, the recovery provided not just relief, but validation.

It was a textbook example of how markets behave under stress - and why long-term discipline matters.

The month began under a cloud of uncertainty. Escalating tensions in the Middle East had pushed oil prices higher and rattled investor confidence.

Markets sold off as investors grappled with the possibility of a prolonged conflict and its potential economic fallout.

But by April’s end, and half-way through May, the narrative had shifted.

A ceasefire agreement between the US and Iran helped ease fears of further escalation. While the situation remains fragile, the move from confrontation to negotiation was enough to restore some confidence. Risk appetite returned quickly, and equity markets surged.

This rapid turnaround highlights one of the most challenging aspects of investing: markets often recover before the outlook feels comfortable again.

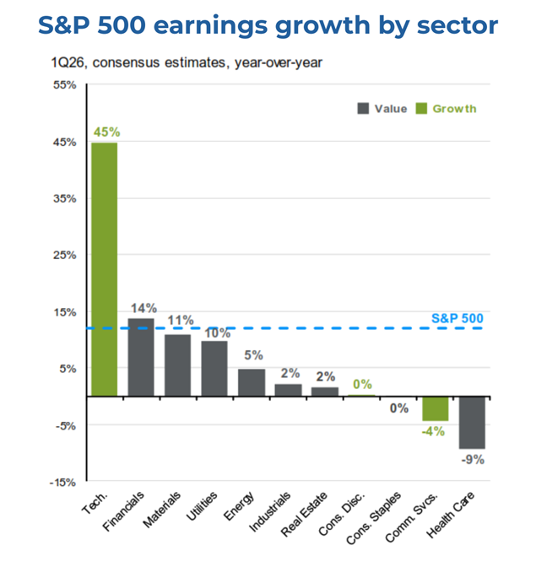

While geopolitics dominated headlines, the underlying driver of April’s rally was far more grounded - corporate earnings and economic resilience.

In the United States, earnings season exceeded expectations. More than 80% of S&P 500 companies that have reported in the past 6 weeks have beaten forecasts, with the technology sector leading the way. First-quarter earnings growth in tech is tracking above 40%, fuelled by continued investment in artificial intelligence and cloud infrastructure.

Source: JP Morgan Chase

Companies such as Microsoft, Alphabet and Amazon delivered strong results, reinforcing the strength of structural growth themes. The AI story, in particular, remains intact - and importantly, still in its early stages.

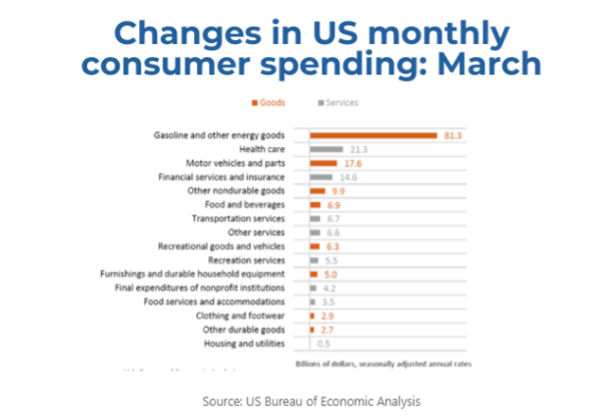

Beyond technology, the broader US economy continues to show resilience. Consumer sentiment may be at all-time lows, but spending has held up (of course there is a lot more of it at the pumps), business activity remains in expansion, and while the labour market is cooling slightly, it is doing so in a controlled way. This balance is helping to ease inflation pressures without derailing growth.

In short, while uncertainty remains, the fundamentals underpinning markets are still solid.

Another key factor supporting markets has been the response from central banks.

Despite rising oil prices and geopolitical risk, policymakers have largely resisted the urge to react aggressively. Instead, major central banks - including the Federal Reserve, European Central Bank, and Reserve Bank of New Zealand - held interest rates steady during April.

This “wait-and-see” approach reflects an important distinction: the current inflation pressures are largely supply-driven, particularly from energy prices, rather than a surge in underlying demand.

By avoiding knee-jerk policy tightening, central banks have helped anchor expectations and provide stability. This has allowed investors to focus on earnings and economic data, rather than worrying about an abrupt shift in monetary policy.

That said, uncertainty remains. Fixed income markets have been more volatile, with expectations shifting between rate cuts and potential hikes depending on how inflation evolves. Bond markets are also increasingly concerned about ever growing fiscal pressures (President Donald Trump wants to up the defence budget next year by over 40% to US$1.5 trillion). It’s a reminder that while stability has improved, the outlook is still complex.

While the US led the rally, gains were broad-based across global markets.

While Europe lagged, Japan’s Nikkei surged more than 16% in April, supported by improving corporate performance and ongoing policy normalisation. China showed signs of stabilisation, with GDP growth around 5% and stronger industrial output, although domestic demand remains uneven. South Korea was a standout, with its market soaring over 30%, driven by strength in semiconductor stocks linked to AI demand.

Closer to home, Australia delivered modest gains, while New Zealand underperformed slightly. The NZX 50 finished April broadly flat, reflecting softer domestic conditions and pressure on consumer-facing sectors.

The New Zealand economy continues to face headwinds.

Inflation remains above the Reserve Bank’s target, driven in part by rising fuel and energy costs. At the same time, domestic pressures - particularly in housing and utilities - remain sticky. Business confidence has weakened, and consumer spending is under strain from ongoing cost-of-living pressures.

The Reserve Bank has adopted a cautious stance, holding rates steady and signalling a willingness to look through short-term energy-driven inflation. Like its global peers, it is focused on whether these pressures become more persistent.

Our money markets, and many economists, did get slightly ahead of themselves. Earlier in the month, pricing implied around a 60% chance of a rate hike at the May meeting - this has since eased closer to 40% as expectations have been recalibrated. Thankfully, the RBNZ’s messaging suggests a more pragmatic approach, with policymakers reluctant to respond aggressively to what is largely a supply-driven shock, particularly given the softer domestic growth backdrop.

There are, however, some bright spots. The export sector remains strong, supported by solid dairy prices and a weaker New Zealand dollar. Tourism has also rebounded, with visitor numbers approaching pre-Covid levels.

Even so, the domestic environment remains challenging - and that has been reflected in the local market’s performance.

For investors, April offered something more important than strong returns - it offered perspective.

When markets sold off earlier in the year, the temptation to reduce risk or move to the sidelines was understandable. Uncertainty was high, headlines were negative, and the path forward was unclear.

But as noted in March’s article history tells us that these moments are not unusual. Whether it’s geopolitical conflict, economic shocks, or global crises, periods of stress are a regular feature of financial markets.

What is consistent, however, is how markets respond over time.

Short-term movements are often driven by fear - what might happen. Long-term returns, on the other hand, are driven by fundamentals - what actually does happen.

April’s rebound is a clear example of this dynamic. Markets recovered quickly, and those who remained invested were rewarded. Those who attempted to time the market faced a much harder challenge: knowing when to get back in.

Periods of volatility don’t just test discipline - they also create opportunity.

During the market weakness, our investment team remained active, selectively adding to high-quality companies where we have strong long-term conviction. This included increasing exposure to businesses benefiting from structural growth trends, particularly in artificial intelligence, where adoption continues to lag capability, despite all the hype (less than 20% of US businesses are using AI).

Companies such as Nvidia, Microsoft and Micron continue to play a central role in the AI ecosystem, while newer positions like ARM Holdings offer additional exposure to this theme. Importantly, our activity was not limited to technology - we also added to companies like United Healthcare, reflecting a broader opportunity set.

This approach - combining long-term conviction with active management - allowed us to take advantage of short-term dislocations while remaining aligned with long-term trends.

It’s a reminder that volatility, while uncomfortable, can be a powerful tool for investors who are prepared.

While the rebound over the past 6 weeks or so is encouraging, it does not mark the end of uncertainty.

Geopolitical developments, particularly in the Middle East, will continue to influence markets - especially through energy prices. Central banks remain a key variable, navigating the delicate balance between inflation and growth.

Economic data will also be closely watched. In the US, labour market trends and inflation readings will shape expectations for the Federal Reserve. In New Zealand and Australia, domestic data will provide further insight into economic momentum. The upcoming RBNZ decision and budget will be closely scrutinised.

Earnings will remain another critical driver, as the reporting season winds down in the US, and gets underway in New Zealand.

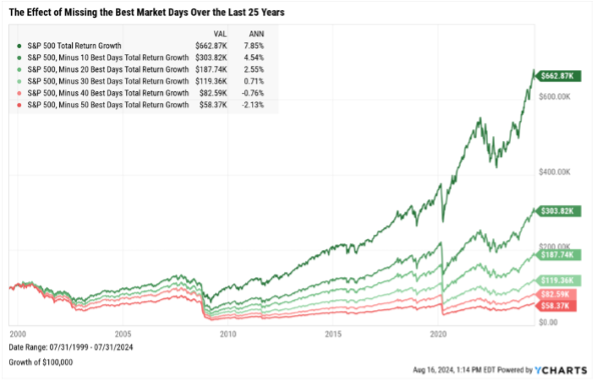

If there is one clear lesson from last month, it is this: staying invested matters.

Markets will always face uncertainty. Volatility is not an exception - it is a feature. But over time, markets have consistently rewarded those who remain focused on the long term.

Trying to time the market - getting out before a downturn and back in before a recovery - is incredibly difficult. Missing even a handful of the best days can significantly impact long-term returns, and those days often come when sentiment is at its weakest.

The rebound is a timely reminder of that reality.

For long-term investors, the most effective strategy is often the simplest: stay disciplined, stay invested, and stay focused on the bigger picture.

Because while markets may be unpredictable in the short term, the long-term trend has always been one of growth - and those who stay the course are best positioned to benefit.

Generate is a New Zealand-owned KiwiSaver and Managed Fund provider managing over $9 billion on behalf of more than 190,000 New Zealanders. With a team of specialist advisers and a track record of strong long-term performance, Generate aims to help Kiwis make informed decisions and build a stronger financial future.

This article is intended for general information only and should not be considered financial advice. All investments carry risk, and past performance is not indicative of future results. To view Generate’s Financial Advice Provider Disclosure Statement or Product Disclosure Statement, visit www.generatewealth.co.nz/advertising-disclosures. The issuer is Generate Investment Management Ltd.

| « Macro Shocks and Micro Risks | What moving to New Zealand taught me about KiwiSaver » |

Special Offers

No comments yet

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved