Just as the stagflation of the early 1970s ushered in what became known as the Monetarist Counter Revolution of the late 1970s, the Global Financial Crisis of the late 2000s has apparently ushered in a Keynesian Counter Revolution of its own, or at least a return of ‘Big Government' in many countries in the West.

Tuesday, December 8th 2009, 9:00AM

A seminal moment

Clearly, governments through their various spending programmes, nationalisation of institutions and most of all through their large financial deficits, which now exceed levels witnessed even in war-time, have returned to a degree of prominence not seen for at least a generation.

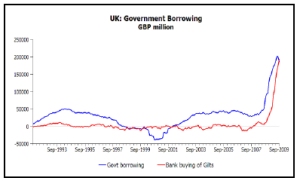

Funding these huge public deficits has, of course, involved the issuance of massive quantities of new government debt and so far this year it has been the global banking system - and primarily the central banks and the investment banks - that have funded by far the greatest part of the OECD countries' budget deficits. Quite simply, rather than ‘real world savers' it has been the operation of the various iterations and versions of Quantitative Easing Policies that have allowed the fiscal largesse which governments have been able to indulge in over the last 18 months.

In short, governments have either been printing money themselves in order to fund their budget deficits or providing the wherewithal to investment and commercial banks to achieve this aim on their behalf. As the Bank of Japan noted in a recent conversation with us, there is little material difference between the central bank buying government bonds directly, or the central bank lending the necessary funds at extremely low interest rates to a troubled commercial bank that then buys the bonds for its own balance sheet (in fact, the only difference is that under the second option the commercial bank will gain the profits accruing as a result of the difference between the higher yields that it receives on its investments relative to the bank's subsidized cost of funds).

Whether this apparently easy funding situation for the governments can persist in the face of rumours of a global economic recovery and, more particularly, against the background of signs of a re-acceleration in inflation rates remains to be seen and, in many ways, this question may mark one of the most important moments for the global economy in recent times. If the governments were to begin to face funding difficulties, then we could envisage their counter revolution either stalling or perhaps reversing altogether, although we suspect that the private sector would also face some considerable fallout from such an event, given its still high dependency on cheap credit.

In fact, we suspect that few people currently realise just how dependent many parts of the world remain on cheap credit and we are somewhat dismayed to find that there remains a strongly-held belief amongst many investors with whom we talk that the world is somehow deleveraging. Although some US commercial banks may be slowly reducing the size of their balance sheets and US households have reduced a small portion of their outstanding debt burden over the last year, in general we find that private sectors around the world as well as the public sectors are still borrowing aggressively, with the result that debt ratios are still rising around the world.

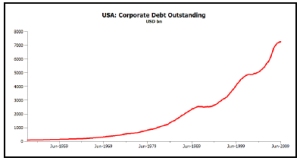

For example, central banks have become large scale financial institutions in their own right providing not just a high powered liquidity system but actual credit to end-users in the private sector such as mortgagees in the US and corporate borrowers in Europe. Meanwhile, although small companies remain credit rationed, many large corporations in the US and Europe are borrowing heavily and by some measures, corporate bond issuance has reached new all time highs over recent months (queue the recent boom in M&A activity). As we have noted in a previous review, the investment banks have revived their mid-2000s business model and are once again expanding rapidly while the household sectors of Brazil, Australia and some parts of Asia are clearly gearing up. Meanwhile, China's credit boom has become one of the most dramatic of modern times.

Consequently, while the world's press may be talking of ‘deleveraging' with something approaching religious fervour, the reality of the situation is that we are currently locked in a renewed credit boom in both the public sector and parts of the private sectors.

Clearly, despite many people's expectations for 2009, we are not repeating the path which Japan took in the 1990s since here private sector de-leveraging has been taking place for well over a decade. This, however, is not the situation in the West - in the US in particular private sector debt is now rising once again and public sector debt is soaring. In practice, we would suggest that far from following the Japanese model, the West is not de-leveraging but in fact re-gearing so that financial markets, property markets, retail sales, employment and government popularity can be supported, if only partially and temporarily.

Returning to our main theme, in our opening remarks we stressed that at the centre of this continuing credit boom process in the West is nothing more than a simple arbitrage carried out by banks and other leveraged institutions between the current very low level of short term interest rates and the higher rates available on longer duration AAA securities, such as government bonds. Moreover, we have noted that governments would not have been able to fund their deficits at such attractive rates (for the issuers that is...), without the banking system's purchases of Treasuries, Gilts, JGBs and Euro government debt. Since corporate bonds are in effect priced off Treasuries and Treasury yields form the basis (and indeed collateral) for much of the ultimate funding and pricing of the investment banks' activities, the health or otherwise of the government bond markets is clearly instrumental in deciding whether the Western leveraging process can continue.

In practice, we suspect that at the centre of the current global liquidity boom lies the US Treasury bond market.

Unfortunately, on a purely fundamental level, we feel that we should be overwhelmingly negative towards the government bond markets at present. Although we are not believers in the global recovery story (the current bounce seems to be a mixture of the end of de-stocking and the effects of particular government stimuli), we believe that bond markets should by rights face a torrid first half to 2010 as inflation rates rise, QEP exit strategies are mulled over by central banks, excessive government bond supply issues surface and long term government solvency issues are brought into sharper focus by Japan's worsening public sector debt predicament.

If bond markets were to crack however, then they would not only threaten the private sector's financial situation (by imposing higher interest rates on borrowers) but most likely also force some degree of fiscal tightening by governments. Quite simply, if bond markets were to crack, the asset price boom and perceived global economic ‘stabilisation' of recent months could evaporate or worse in a relatively short space of time.

For governments, there is clearly now a need (including an electoral one in the US and UK) to keep bond yields low and now that they implicitly own large tracts of the global banking system, they potentially command the means to keep yields low - since they could in theory force the banks to keep supporting the bond markets. In this context, we note that Spain, the US and the UK have already moved some way down this track with regulatory initiatives.

However, many of the commercial bankers concerned can remember the bond market debacles of 1994 and 2006, when QEPs were removed. Central bankers meanwhile are concerned by the extent of the global credit and capital flows boom, its potential inflationary consequences, the undesirability of their growing direct roles in the credit system and most of all the potential systemic risks that may be growing in the resurgent credit systems.

Consequently, many technocrats and policymakers in the central banks are wary about the current situation (and its long term impact on the ‘supply side' of the global economy) and hence many would like to exit the current regime as soon as possible. Furthermore, we sense from our contacts in the industry that even many in the investment banking world saw 2009 as a ‘last chance' to continue the old model and even they may now be expecting some form of deceleration in 2010. Therefore, it seems that with ‘fundamentals' apparently turning against bonds, many of the participants in the bond markets and by implication in the maintenance of the current credit resurgence are looking for their own exit strategies. Clearly, we are moving to a situation in which the ‘free will' of the financial system could cease to be aligned quite so closely with that of the governments.

For us, the question that will likely shape the global economic landscape - potentially until the next theoretical ‘counter revolution' in a decade's time - is will the governments exercise their rights as shareholders in the financial system to force the banks to keep the bond markets acquiescent? Specifically, will governments oblige the banks (including the central banks) to keep buying bonds and so keep the current credit boom alive by maintaining the low level of interest rates, regardless of the impact that this will have on savers (who already face negative real interest rates) and the long term efficiency of capital allocation within the global economy (including the emerging markets which are already being destabilised by the recent credit boom-related surge in global capital flows)?

Many rightly fear that governments, by dint of the political calendars involved will stop being passive shareholders and begin to exert managerial control over the banking systems that they now own but, while in the short term this may allow the global credit boom to continue, its long term impact would likely be as damaging as every other rise in government control of the capital markets has proved to be in the past.

If the governments do now force the banks to support the bond markets even as fundamentals decline, asset markets may be a ‘buy' in the short term but the 1970s will surely follow the increase in state interventionism in the credit system. For our money, we would expect the central banks to defy their political masters (something which might even appeal to one or two of them...) and to resist artificial attempts to support the bond markets but clearly their paymasters have the ability to override the central bankers if they so wish.

On a practical level, we shall simply be watching the regular credit numbers to see what the banks actually do in the face of these two large opposing forces but it does feel that the next few months will see the outlook for the next 10 years in the global economic system defined.