by Pathfinder Asset Management

The 'what' and 'why' of alternatives

A recent international study by Willis Towers Watson focused on US$33 trillion of pension fund assets in 7 countries (Australia, Canada, Japan, Netherlands, Switzerland, US and UK). They found that across portfolios an average of 24% was invested in assets classified as “other/alternative” - a staggering jump from 7% in 1996. By contrast equity allocations have gone down from 52% to 44% over the same 19-year period. The rationale for alternatives is well understood, it is about risk and return:

Below we look at PIE fund options for NZ investors in alternative assets by reviewing hedge funds, private equity, commodities and other 'alternative strategies (we will save real estate for a future commentary)'.

Multi-asset hedge funds

Multi-asset hedge funds invest across a range of asset classes – equities, fixed income, commodities and credit. They can also cover a broad geography (i.e. both developed and emerging markets).

Their returns are not benchmarked to equity markets. The intention is to generate positive returns in all conditions, whether markets are going up or down. These funds are likely to include unconventional strategies like long / short exposures and leverage. Unfortunately the proprietary nature of hedge fund investing often means limited transparency to the underlying assets (although this is improving).

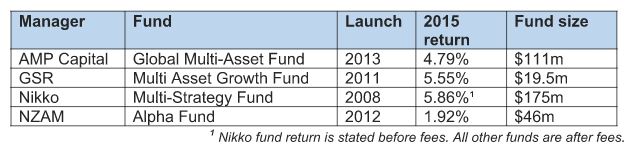

The NZ fund manager will typically “repackage” one or more offshore hedge funds through a PIE fund with currency hedging. For example the GSR fund mentioned below invests in the Blackrock Multi-Opportunity Fund, the Nikko fund in JP Morgan’s Multi Strategy II fund, the AMP fund invests with both AMP and Schroders and the NZAM fund invests in a “diverse group of managers”.

There are advantages of using a PIE fund rather than trying to access the offshore hedge fund managers directly. These advantages include:

Here are hedge fund PIE options available in NZ:

Hedge funds have been a tough space for NZ fund managers. Several specialist funds in this area have subsequently disappeared – largely because it has been difficult raising investor money (Elevation, Richmond and Savings & Investments have generally had good underlying hedge fund managers but limited traction with NZ investors).

These hedge fund PIE products seem to succeed in their mission of producing returns uncorrelated to equity markets. For example, the correlation of NZAM’s fund to global equity markets is close to zero (-0.06). In recent years this class of funds has helped diversify portfolio risk, with positive (but largely unspectacular) returns.

Private equity

Private equity has proven itself by generating solid absolute returns in NZ – fund returns exceeding 20% p.a. are common. While it is a lucrative asset class, the problem for most investors is finding access to these investments.

For sophisticated investors who can write large cheques there are occasionally private equity managers raising new funds. Names include Maui, Knox, Pencarrow, Waterman and Direct Capital (the NZ Super Fund has invested with these last 3 managers). However these investments are only available to wholesale investors with minimum applications of $100,000, $250,000 or more.

There have been a few attempts to make private equity funds accessible to retail investors, namely:

The challenge with private equity is liquidity. The underlying assets cannot be sold easily so typically investors must hold for 7-10 years until the fund is wound up. The funds do not offer redemptions and there is no developed secondary market. In summary private equity offers good returns for investors, but limited access and very restricted exit options. The higher returns reflect a premium for very limited liquidity.

Commodities

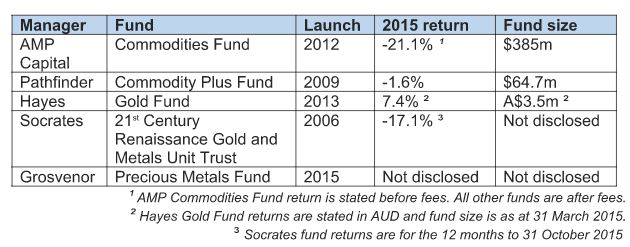

Commodities are the basic building blocks of economies – things that are grown in the ground (like corn and wheat) or extracted from the ground (like oil, copper or gold). Commodity markets have been through tough times in recent years. Oil for example was close to US$100 a barrel less than 2 years ago (now 70% lower). Gold hit an all-time high of US$1,921 an ounce in August 2011 (now 35% lower). Whether prices have stabilised or will continue to be volatile is widely debated.

There are several PIE fund options for commodities in NZ. However, the difficult environment for commodities is reflected in fund returns:

Alternative strategies

The managers in this category may employ strategies similar to “hedge funds” (discussed above) but they are not multi-asset funds. For this reason we regard “alternative strategies” as a separate grouping. There are some interesting and quite varied NZ PIE funds in this category:

It is worth noting that we could have included concentrated equity funds like Castle Point’s Ranger Fund and Devon’s Alpha Fund (closed to new investors) in the table. They do not track equity benchmarks but as concentrated active funds that cannot go “net short”, they are not quite “alternative” enough to include. By contrast the net market exposure of Salt’s Long Short Fund can be anywhere between 30% short and 60% long.

Closing thoughts

There are a range of PIE fund options that give access to alternative asset classes and strategies. These include hedge funds, commodities and alternative strategies (but unfortunately limited options in private equity).

Are these useful for NZ investors? “Alternatives” may enhance returns or diversify portfolio risk (in a perfect world they would do both!). In particular, they often help portfolios with their low correlation to equity and bond markets.

Be sure to do very thorough research before including alternatives in a portfolio. Here are some points to ponder:

In summary, there are a range of alternative asset funds available in NZ. They cover hedge funds, commodities, alternative strategies and private equity. Depending on investor risk profiles, one or more could be a useful addition to portfolios.

John Berry, Director

Pathfinder Asset Management Limited

Seek advice: Pathfinder is a fund manager and does not give financial advice. Seek professional investment and tax advice before making investment decisions.

Disclosure of interest: John is a founder of Pathfinder and invests in its Commodity Plus Fund. He is also an independent director of (and invests in) Punakaiki Fund Limited.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « Super fund invests in a new strategy | NZ & Australia Company Results Review » |

Special Offers

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved

Secondly in his promotion of PIE funds Mr Berry neglects to mention that PIE funds have a disadvantage in that they cannot use comparative value to reduce their tax liability in falling markets.

Thirdly Mr Berry forgets to add that most investors recent experience of alternative assets is that they frequently become correlated with equity markets whenever equity markets fall thus lose their much vaunted diversification benefits at just the time they are needed.