NZ & Australia Company Results Review

While some New Zealand companies produced solid earnings results, and overall the results were not as bad as some may have expected, there was a wider divergence of earnings growth outcomes than in previous periods.

Friday, March 11th 2016, 12:00PM

by Harbour Asset Management

Company outlook statements were cautious, with signs of a broad softening in activity levels. Both Diligent (+19.4% over February) and Nuplex (+21.5%) received takeover offers during the month, underpinning the valuation of the New Zealand equity market.

The Australian reporting season was better than expected, with more companies beating market expectations than missing them. Resource companies outperformed as commodity prices stabilised (particularly iron ore and gold) and low earnings expectations were met or exceeded.

Locally it was the best since 2012 with fewer downgrades and more upgrades. Across the Tasman results were better than feared with earnings revisions lacking their normal downward bias.

Share price weakness going into the results season has mostly been attributed to global concerns rather than specific influences from Australia or NZ. Weakness in global banks saw Australian financial stocks selloff significantly in sympathy, rather than reflecting actual results or underlying bank sector influences (see Bank section below).

Most pleasing individual result?

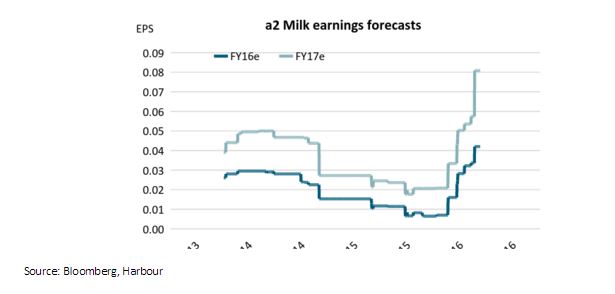

a2 Milk presented its full year result during the month delivering sales and earnings well ahead of consensus expectations. However, it was the upgraded guidance for FY16 that caught the markets attention. This was the third earnings upgrade by the company in as many months, with infant formula sales being the key driver of the upgrade. The result suggests strong demand for infant formula in China, highlighting that the company has been successful at building a brand that consumers trust and want to buy. The a2 stock price, however, did not respond to the improved outlook on an expectation that the regulatory environment in China will make it harder for companies such as a2 Milk, Bellamy’s and Blackmores to distribute product to China via so-called grey channels. The a2 Milk Company has significantly increased sales through official distribution channels and signalled that this trend will continue, reducing the potential for adverse regulatory impacts.

After years of looking expensive, the a2 stock price is no longer a valuation outlier. The a2 stock price is currently trading at 22x forecast FY17 Price-to-Earnings multiple, which places it 11th in the ranking of New Zealand stocks on a price-to-earnings multiple. This suggests that the market is demanding a significant risk-premium for the potential regulatory risks and possible general execution risk into new jurisdictions.

Most disappointing individual result?

Sky TVs result again provided a small downgrade to guidance. Sky TV’s immediate advantage is security of content, but subscriber momentum and cost pressures (sports content and currencies) remain key issues. There is a belief that Spark is well on the way to waving the white flag with Lightbox, so the immediate local competition may begin to wane. The online subscribers (Fanpass, Neon and SkyGo) may be growing, but overall revenues are clearly under pressure and the subscribers nowhere near as valuable as the traditional satellite subscribers. Capital management remains the most likely outcome. However, any returns are expected to be modest (circa $100m), and anything larger would probably raise questions given the capital needs for the company over the next five years.

Skellerup also disappointed, although given tough industry conditions this was less of a surprise for the market. Sky City Entertainment, Wynyard and Fletcher Building results also disappointed, but in Fletcher Building’s case outlook comments were positive.

Which sector/s held up the best?

Tourism continues to be a strong area of growth for the NZ and Australian economy. Visitor arrivals have been very strong, and this supported Auckland Airport (a nominee for best result), Sydney Airport and other stocks in the sector. Auckland Airport’s result was very good with a circa 8-9% upgrade to earnings guidance provided by the company. Strong retail spend at the airport and lower capital expenditure demands were the key drivers. Australasian hotel operator, Mantra Group, also had strong profits and earlier in the month many analysts upgraded Air New Zealand’s profits after increased guidance.

Which sector/s underperformed?

The electricity sector generally had weak metrics. Retail competition and hydrology impacted results across the sector. Competition for broadband (in part from Trustpower) also impacted on Spark’s result. It is also likely that we will see further bundling of services provided by the larger utility companies, with Contact Energy likely to be the next one to offer broadband services.

Harbour attended the annual downstream energy conference which highlighted several key thematics. Retail competition is likely to fragment further as niche offerings attract different customers. Retail brands could hit 50 from 29 currently available, with offerings coming from disruptive and non-traditional players.

Electricity customers are also likely to lead change in the sector, particularly around emerging technologies of solar and battery. New business models will likely develop that lead to increased penetration and uptake with the large companies becoming increasingly marginalised if they fail to adapt and respond.

Biggest surprise?

As opposed to earnings (see a2 Milk and Auckland Airport), takeovers announced in the month for Nuplex and Diligent provided surprises for the market. These two stocks topped the returns in the month. Diligent received a takeover offer of US$4.90 per share from US-based private equity fund Insight. Unfortunately, the offer is likely to succeed in its current form as the company is incorporated in Delaware where a threshold of 50% acceptance is required, and the offer isn’t subject to NZ takeovers code where shareholder acceptance of 90% would be required. Currently 35% of outstanding shares are committed to support the offer. Chorus also positively surprised with a higher dividend.

Were dividends broadly higher/lower/same?

Broadly speaking dividend expectations have been met or exceeded. Compared to earnings, dividend (and special dividend) growth is strong. In NZ, so far dividends are up a healthy 9%. That is interesting, as despite a pause in earnings growth, companies remain confident in cash flows and future growth. Corporate balance sheets remain relatively strong.

At an aggregate market level, dividend per share growth was 17.1%, primarily driven by Chorus, Fletcher Building and NZ Refining. At a median level, growth was more modest at 1.3%. FY16 estimates have seen positive revisions to 13 companies with 8 negative revisions. An area of caution we are watching is the dividend pay-out ratio with the aggregate market pay-out for the forecast period creeping up to 86% of earnings.

Why have bank share prices been volatile?

In recent weeks share prices of listed Australian banking and financial sector companies were weak and then in the first week of March bank share prices rallied sharply. In part, this volatility reflected a correlation with the global widening of credit default swaps, and over-reaching speculation of rising impairments, illiquidity issues and general funding concerns. Fortunately, all the Australian banks have recently either reported earnings, provided trading updates or made quarterly disclosures under their Pillar 3 requirements. By and large, these disclosures and management commentary has dispelled impairment, net interest margin, liquidity and funding concerns.

For example, all the banks disclosed strong regulatory capital. In fact, there were several positive disclosures. Westpac’s impaired assets fell, NAB and CBA showed little movement in impairments or asset quality, while ANZ provided guidance of some deterioration in asset quality, but even then much of that was associated with specific mining exposure in Indonesia.

Net interest margins for the banks were generally better than expected (as higher wholesale funding costs were offset by higher mortgage pricing in the period).

Both Westpac (now 14.3%, was 13.2% in Sep 2015) and CBA (now 14.3%, was 12.7% in Jun 2015) now have internationally comparable capital positions that would place them at the very top of global league tables on a like for like basis.

In terms of liquidity, the banks have significantly lifted excess liquidity in the last five years. For instance, Westpac now has $30bn of excess liquidity over their regulated requirement. Wholesale funding maturities have also been extended across the bank sector. Already in the last few months, and despite recent financial market conditions banks have issued benchmark trades in all major markets.

The key point is that since 2008, Australian banks have significantly improved their funding, liquidity, capital positions and have moved to re-price risk. A spike in global credit spreads does have a negative impact but compared to 2008 this impact is softened by the reduction in wholesale funding requirements, access to new covered bonds, the longer tenor of funding and more flexible mortgage rates.

A key area of investor focus remains the performance of loans to mining, energy and agriculture. These sector exposures are relatively small (<2% each by sector) but remains clearly topical exposures. Stress and impairments in these sectors remain low (highest in agriculture, lowest in mining) however, banks seem to be very watchful and are making more detailed disclosures. For instance, ANZ did guide for higher-than-expected impairments as a result of Indonesian mining exposures.

In our view analysts’ consensus for dividends is broadly right. Granted we are at lows in the impairment cycle, but for now talk of an elevated impairment cycle seems more of a risk than a central scenario. The share prices of banks seem to imply a significant deterioration in impairments, or falling net interest margins, or both. The latest earnings round provides few signals that either factor is currently a significant concern.

Moreover, for the Australian corporate sector more generally, earnings announcements have shown significant resilience, consistent with broader signals of moderate economic growth.

Outlook

Global equities had a weak start to 2016, but global growth has continued to be a little stronger than the worst fears. Employment data in the US remains firm, and it seems that calls for the US economy to experience a recession are not supported by the data. Given reasonable earnings expectations and cyclically adjusted valuations, we believe the pull-back provides another opportunity for investors to buy cash generative and growing New Zealand and Australian companies at a reasonable price.

In a further sign of corporate health, M&A activity continues. In New Zealand, two takeovers have been announced at large premiums. Technology company, Diligent and chemical company, Nuplex announced takeovers on the same day, propelling both stocks toward bid prices.

And more broadly, despite the down-draft from the mining, energy and dairy sectors, economic conditions in Australia and New Zealand show little economic stress. Consumer confidence in both countries is strong, credit growth is moderate, and overall business sentiment on a trend basis is consistent with expansion.

Andrew Bascand, Shane Solly, Craig Stent

9 March 2016

This column does not constitute advice to any person.

www.harbourasset.co.nz/disclaimer/

Important disclaimer information

| « Investing in 'alternatives' | Playing the man not the ball » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |