Christian Hawkesby

by Harbour Asset Management

Christian Hawkesby

In our view, the market is currently underestimating the chances of a third scenario, which is a combination of both stronger inflation pressures and softer economic growth.

One of the few certainties when putting together economic or market forecasts is that your central projection is unlikely to be exactly right. This is what motivates a focus on alternative scenarios, to gain a better appreciation of the range of possible outcomes and the balance of risks.

At any time, there are a host of different things that could push the economy off its path. In the current environment, the list might include the threat of global trade wars disrupting economies and markets, the risk of a disorderly slowdown in the Chinese economy, the possibility of fiscal stimulus overheating the US economy and the chance of inflation finally re-emerging in Europe after a period of hibernation.

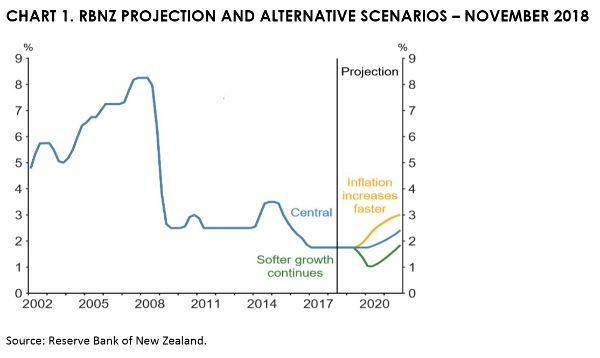

In the Monetary Policy Statements in both August and November, the RBNZ has used the same two alternative scenarios.

The first scenario is that, after a period of very subdued inflation pressure, firms finally revert back to a faster pass-through of costs into prices.

The second is that the recent deterioration in business sentiment results in a more long-lasting decline in domestic demand.

Since August, the market has focused primarily on chances of the downside scenario and, particularly, the prospect that the OCR is cut in response if GDP growth falls below 3%.

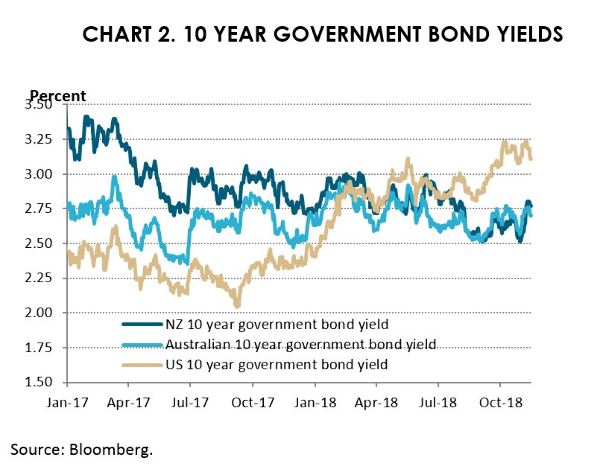

As a result, in recent months, the market has priced up to a 50% chance the OCR being cut by at least 25 basis points in the next 12 months. This has seen yields on NZ 10 year government bonds fall to near all-time lows versus international markets.

We believe the market should also be considering a third scenario for the New Zealand economy. That is, where the recent decline in business confidence persists due to supply constraints at the end of a long economic expansion, rather than an absence of demand.

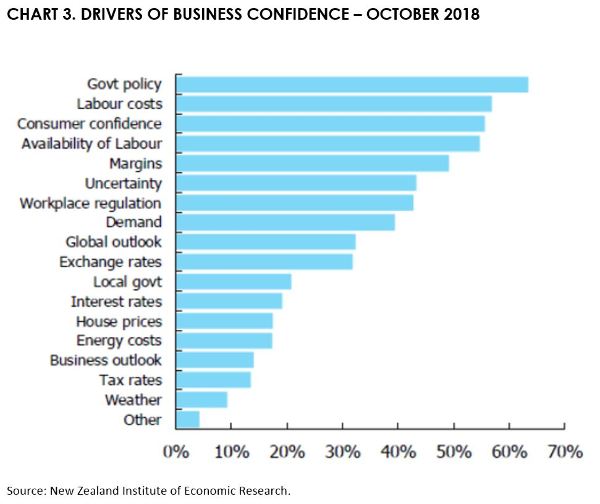

In their most recent survey, NZIER attempted to get to the bottom of the issue of what is driving business sentiment by asking respondents what is motivating their answers on business confidence.

Amongst the laundry list of responses, demand is a factor, but it sits lower than a host of supply-side factors such as labour costs, availability of labour and pressure on profit margins.

This message is consistent with other economic indicators suggesting capacity constraints, such as the difficulty finding both skilled and unskilled labour, and the NZ unemployment rate recently falling to 3.9%.

In other words, it could be that businesses are feeling gloomy not because of a worry about lack of demand, but because of rising labour and other costs creating a squeeze on profit margins.

This is certainly a theme that our equity analysts uncover during their company visits.

Under this third scenario, even if business confidence remains low and GDP growth was to moderate to 2-2.5%, firms may still eventually be forced to bite the bullet and pass rising costs on leading to higher price inflation.

This looms on the horizon as a key question and judgement for 2019.

To be clear, this scenario does not entail a recession, or stagflation; just an end to the global post-GFC Goldilocks period of strong growth and very low inflation.

So what would be the implications for markets?

In some ways it would look similar to the RBNZ’s existing higher inflation scenario, with some variation.

Since August, the RBNZ has displayed a very strong preference to keep the OCR on hold for prolonged period, to give core CPI inflation the best possible chance to get back to the 2% mid-point target or higher.

As a result, it would seem most likely that the initial reaction to stronger inflation pressures would be reflected in higher long-term bond yields, as the market prices in higher long-term inflation expectations. At the moment, the NZ government inflation-indexed linked bond market only implies CPI inflation averaging 1.35% over the next 10 years.

A more rapid reaction from the RBNZ would see mortgages rates and the NZ dollar push higher, which could take markets by surprise.

In summary, our central case continues to be that the RBNZ will keep the OCR on hold well into 2019.

As always, there are a range of scenarios that could play out to change the course of the economy and markets.

In addition to the RBNZ’s two existing scenarios, we see potential over the next 3 to 6 months for the market to shift focus and increasingly watch for evidence of both higher inflation pressures and moderating growth – an end to the global post-GFC Goldilocks period.

By Christian Hawkesby, Head of Fixed Income & Economics

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Equal weight vs. Market cap weight | Brexit boilover; It's all coming to a head » |

Special Offers

No comments yet

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved