The scheme set up by Rupert Carlyon and backed by Warren Couillault and Hobson Wealth, is pitching itself as a roboadvice platform using passive funds.

“Digital advice is a very popular proposition overseas and we are excited to be able to launch a truly consumer focused digital adviser in New Zealand,” Carlyon says.

The firm says the majority of KiwiSaver members are in the wrong funds and that the biggest issue is a lack of advice.

Instead of using advisers to solve this issue, kōura plans to solve it using technology.

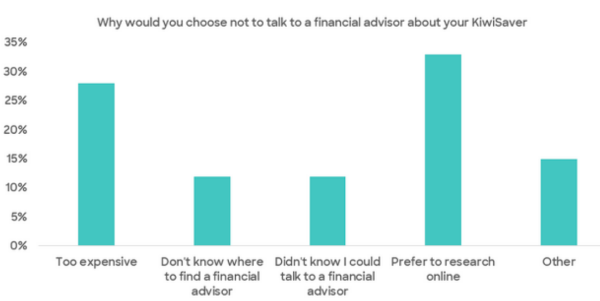

“In the 12 years since KiwiSaver has been operating, the focus has been on encouraging customers to sign up to KiwiSaver, rather than focusing on ensuring the right outcomes for customers. Advice and help is really hard to come by. Financial advisors are seen as out of reach for most people and our research shows most would prefer online research to an adviser in any event."

“We strongly believe that free digital advice will play a key role in improving the financial literacy of KiwiSaver members and help them make meaningful informed choices that are in their own interest.”

"kōura offers investors six separate passive investment funds providing investors an exposure to more than 45 global markets and more than 3,000 companies. Rather than offering the traditional Growth, Balanced and Conservative funds, kōura creates a personalised portfolio that’s tailored directly to the customer’s life stage and financial goals."

This is the third KiwiSaver Scheme that Warren Couillault has established, the previous two schemes being the Fisher Funds and Generate KiwiSaver Schemes.

“All of the KiwiSaver schemes I’ve been part of have been an evolution to what’s already in the marketplace, providing something more advanced,” says Couillault. “kōura is the same. We’re bringing technology into the KiwiSaver space – helping make sure that all kiwis maximise their KiwiSavers’ potential. Hobson Wealth Partners (which has a shareholding in koura and provides various support services) is excited to be a part of this journey as we believe in the value of advice."

"Helping people achieve better financial outcomes is what we stand for at Hobson Wealth so kōura is a perfect fit for us.”

update their goals and objectives

| « Code Committee: We've thought about what could have been better | Mann on a mission to diversify financial advice » |

Special Offers

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved