by Harbour Asset Management

• Global COVID-19 infections have continued to worsen sharply reducing investment sentiment and creating pockets of financial stress.

• While sentiment is clearly downbeat, there is still a wide range of outcomes that might occur.

• In the event COVID-19 does result in recession, note all recessions have been different and, if this one eventuates, it might be short and sharp.

• While this heightened volatility is unsettling, it is important to put this equity market sell-off in historical context.

Global COVID-19 infections have continued to worsen sharply reducing investment sentiment and creating pockets of financial stress.

At the time of writing, the US share market is down 29% since its peak, and the New Zealand market has fallen by about 23%, fearing the worst from COVID-19 with little optimism shown following monetary and fiscal policy responses thus far.

It is impossible to plot the exact path that markets will take from here. COVID-19 has become more widespread than markets initially anticipated, affecting supply chains and economic activity. This poses a challenging environment for economic policies and forecasting growth.

While sentiment is clearly downbeat, we need to recognise that, from here, there is still a wide range of outcomes that can occur.

We note from high frequency data that much of China and Japan are progressively getting back to work.

The best-case scenario is that COVID-19 might prove to be, as some recent epidemiologists have suggested, less contagious as the northern summer emerges and that a co-ordinated global monetary and fiscal policy response restores market confidence.

The worst-case scenario is that the virus takes longer to burn-out or be contained and indeed leads to a global recession.

Currently, markets seem to be favouring, and pricing in, a recession and more financial stress.

It is important to remember that, in the event COVID-19 does result in recession, all recessions are different. We know this because there have been 11 recessions in post-war America. Some had relatively small impacts on employment and investment markets, while others, like the Global Financial Crisis (GFC) in 2008, had longer and deeper impacts.

The crisis of 2008 was a “balance sheet” recession. House prices in the US had risen sharply in the years prior due to excessive leverage and over-confidence. When the bubble burst, it left a massive hole in household balance sheets and meant households focussed more on reducing debt than consumption (which means the consumer is in a much better position today than they were in 2008).

This, in turn, exposed the highly leveraged banking system and led to a collapse in global demand.

The economic shock posed by COVID-19 affects both the supply and the demand side of the economy. Factory and business shutdowns, travel bans and school closures impact the ability of the economy to produce goods and services.

The reaction to COVID-19 also means fewer trips to shops, restaurants and cinemas, which represents a demand shock – consumer spending falls. Large falls in the stock market also have a negative wealth effect, leading potentially to people cutting back on spending due to falling wealth. These effects can sometimes be self-reinforcing, which is something we are watching as it has the potential for a supply/demand recession to morph into a balance sheet one.

While the GFC was a financial shock that affected the demand side of the economy, COVID-19 is an economic shock that affects both the demand and the supply side of the economy. The two situations are fundamentally different; therefore, the length and impact of the downturn should be different as well.

The GFC in 2008 led to a deep recession followed by an extremely slow recovery as households and financial institutions repaired their balance sheets. COVID-19 may trigger large falls in output of affected economies over just the next 1-2 quarters, provided that the virus fades.

This is what has been suggested to us by all epidemiologists we have spoken to; activity should rebound as supply constraints are lifted. It is worth noting that in China, where the outbreak started, economic activity (measured using high frequency indicators like traffic congestion and coal consumption) has started to resume as new cases slowed to a trickle and containment measures are relaxed.

The economic shock of 2008 was exacerbated by high levels of corporate debt and an over-leveraged banking sector. Today, banks are much better capitalised and corporate debt ratios, especially in NZ, are not alarming.

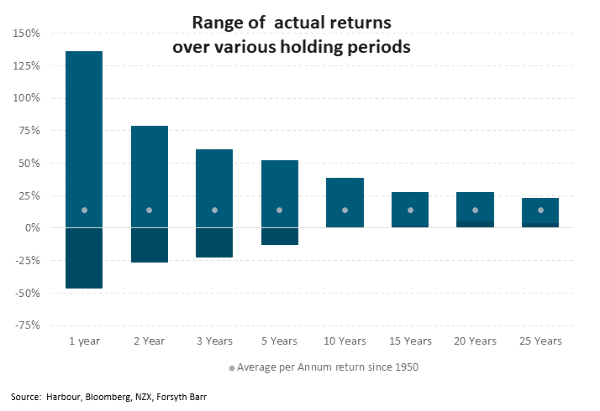

Lastly, while this volatility is unsettling, it is important to put this sell-off into historical context, which the below data, encompassing the 1987 share market crash, the dotcom bubble and the Global Financial Crisis, does.

The bars show the highest and lowest per annum return over each of those periods whilst the dots provide an average per annum return over each of those measured periods since 1950.

If you have any questions about this article or what Harbour is doing in portfolios at the moment, please contact Shannon Murphy (Investment Specialist) at shannon.murphy@harbourasset.co.nz

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Negative news abounds; but things will get better | Recovery from coronavirus – a buying opportunity? » |

Special Offers

No comments yet

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved