Adrian Riminton

The new structure is designed to be simple and transparent, chief distribution officer Adrian Riminton says. But it is also about creating s sustainable model for the company.

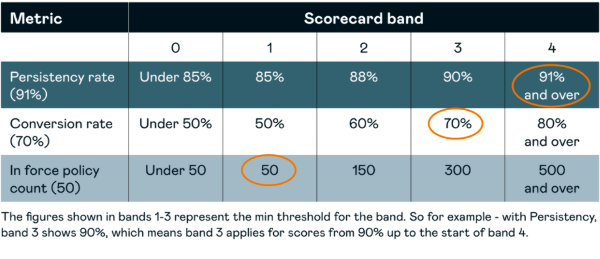

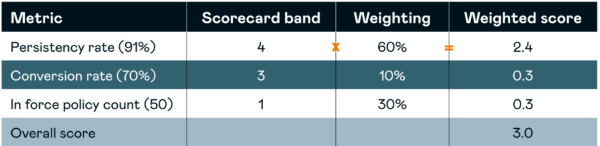

Like Partners Life, Fidelity is using a score sheet to set commission levels. The three factors in its matrix are persistency (60%), in-force policy count (30%) and conversion rate (10%).

Advisers are scored in five bands across these three metrics.

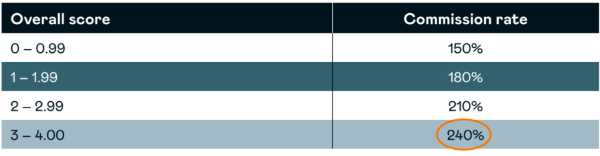

A weighted score is then calculated and these correspond to four commission bands. The lowest commission is 150% and the highest 240%, with intermediate bands of 180% and 210% (see table below).

The new model was put together before new chief executive Melissa Cantell joined the firm. She was happy with it and has not changed anything.

“It’s got my full backing,” she says.

The company is clearly aiming to improve persistency. Currently overall persistency rates across its products sits in the order of 90%, Riminton says.

Another change will see the simplification of ongoing commission for new business, with renewal and service commissions to be combined into one rate of 10% and referred to as "servicing commission".

Last year Partners Life shook up the industry when it decided to pay any override commissions to FAPs as opposed to dealer groups. This decision had wide ranging impacts on the market including leading to the sale of Newpark to SHARE.

Riminton says Fidelity Life will not be paying override commissions. Instead the total amount of commission available is included in its new package (with the highest being 240%).

This will be calculated at a FAP level.

How it is paid out is a decision for advisers. For instance if an adviser wanted to split the commission and include paying a portion to a dealer group that would be possible.

He says some dealer groups are still trying to work out their models in the new licensing environment.

Fidelity is supportive of dealer groups, he adds.

“We still believe a number of groups provide valuable support to advisers.”

Fidelity is also planning to introduce a new “commission on submission” payment to its remuneration package.

While eligibility details will be confirmed in the coming months ahead of July, the company estimate 50% of all advisers will be eligible to receive commission on submission. If they’re eligible and opt to take commission on submission, they’ll receive a fixed 30% of their total initial commission as per their scorecard calculation

Below is an example of an adviser whose metrics are:

91% persistency

50 in force policies

70% conversion rate

A weighted average score is then calculated

The Overall Score then determines commission levels

| « Disclosure warning as new regulations come into effect | Mixed reviews from advisers on FMA regulation » |

Special Offers

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved