by Mint Asset Management

The rise of passive investing and exchange-traded funds (ETFs) has been one of the biggest financial trends of the past two decades – low costs, instant diversification, and strong performance for US and global indices in a 15-year bull market.

But with passive flows dominating markets, a question worth asking is whether the very popularity of indexing has quietly created other risks. In a concentrating market, asset allocators need to actively look for efficient diversifiers to improve model portfolios.

The growth of ETFs over the past two decades has been staggering. ETF assets under management grew over 30% in 2025, and surpassed US$19 trillion globally by year-end. In the US, roughly half of all managed fund and ETF assets are now in passive vehicles, and since 2010 c.80% of every dollar invested in US markets has flowed to just three providers: BlackRock, Vanguard, and State Street.

The appeal of ETFs, most of which are ‘index tracking funds’ is easy to understand. Low fees, broad exposure, and market returns. Yet the sheer scale of passive flows has begun to reshape markets in ways that deserve careful attention. As passive flows pour into market cap weighted indices like the S&P 500, the largest stocks receive the most capital – not because they are the most attractively valued, but simply because they are the biggest.

Diversification is a critical plank in portfolio construction. It makes sense to have a portfolio that is broadly spread across different sectors and geographies; is exposed to different trends; has a blend of cyclical and defensive businesses; small caps vs large caps etcetera.

The risk is that that while indexing may promise broad diversification, it may not always deliver this to investors. The US S&P 500 Index is a case in point. The top 10 stocks in the S&P 500 now account for over 40% of the entire index – double the 19% share they held in 1990.

Cut another way, technology companies combined also account for over 40% of the index. Additionally, companies viewed as impacted by AI (either ‘AI-winners’ or ‘AI-losers’), now account for close to 50% of that index by some estimates.

Weight of top 10 companies in S&P 500 Index

Source: JP Morgan

According to modern portfolio theory, the ‘market portfolio’ is supposed to sit on the efficient frontier – but that is highly questionable in a world of such high concentration.

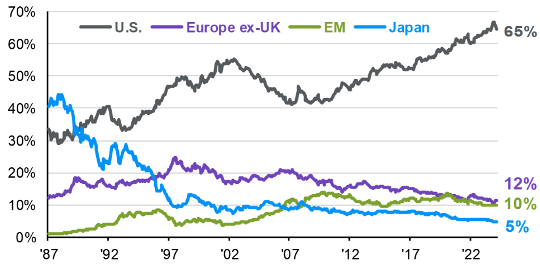

It isn’t just the US market that has become concentrated. Broad global indices like the MSCI World Index have followed the same path. 70% of the MSCI World is invested in US-based companies, with the ‘Magnificent Seven’ stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) now representing over 25% of the index.

History offers a powerful warning. At the peak of Japan’s asset bubble in 1989, Japanese equities represented close to 45% of the MSCI World. A global index investor was, without realising it, almost half-invested in an extremely overvalued share market that traded on over 60 times earnings.

When the bubble burst, the Nikkei lost more than 80% of its value over the following decade, subtracting c.30% off the value of the MSCI World Index on its own.

The lesson: blind indexing can mean blindly inheriting extreme concentration risk.

Share of global market capitalisation

(% of MSCI World Index)

The dominance of passive strategies also has implications for how markets behave during periods of stress. When markets sell off, index fund redemptions force mechanical, indiscriminate selling of every stock in the index – good and bad alike. This happens simultaneously across trillions of dollars of assets, amplifying downward moves in ways that pure fundamentals alone would not justify.

This effect is compounded by a range of strategies that have grown alongside the passive boom: risk-parity funds, which automatically reduce equity exposure as volatility rises; ‘trend-following’ funds, which sell into falling markets; and volatility-targeting strategies, which mechanically unwind leverage when markets become choppy.

By John Middleton

The European Central Bank documented how, during the March 2020 Covid crash, risk-parity strategies alone were required to sell assets equivalent to 225% of their portfolio capital to meet volatility targets. Academic research also confirms that stocks with higher ETF ownership experience meaningfully greater volatility.

None of this is to suggest that indexing has no place in a portfolio - it certainly does. Rather, it is to highlight that an unexamined reliance on cap-weighted indexing carries risks that are easy to overlook.

While the last decade has not generally rewarded broad diversification, that may not be the case over the next decade. In 2026, we are already seeing significant change in market leadership. Europe, Japan and Emerging Markets are outperforming the US, small caps are outperforming large caps, value is outperforming growth, and the Mag 7 are lagging the benchmark.

It feels like an opportune time for advisers to review portfolio construction.

In the current environment we believe asset allocators should favour more geographical diversification against less; consider a range of both public and private market assets; ensuring an allocation to more inflation-protected asset classes like property and infrastructure; and also hold a blend of both passive and active strategies (after three years in a row where the majority of active managers have underperformed).

The goal for client portfolios should be to deliver strong absolute returns over the long run – not to replicate a concentration risk that most investors would not choose if they were designing a portfolio from scratch.

Mint Asset Management is an independent investment management business based in Auckland, New Zealand. Mint Asset Management is the issuer of the Mint Asset Management Funds. Download a copy of the product disclosure statement at mintasset.co.nz

| « Tariffs, Tehran and Turbulence |

Special Offers

No comments yet

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved