Tariffs, Tehran and Turbulence

Wednesday, March 11th 2026, 11:40AM

by Harbour Asset Management

Key market movements

- Global equities navigated a multi-faceted landscape, delivering solid returns over the month. The MSCI ACWI rose 2.1% in NZD terms and 1.4% for NZD‑hedged investors, with markets continuing to rotate away from mega-cap US technology names.

- New Zealand and Australian equities also performed well. The S&P/NZX 50 gained 2.3%, supported by an encouraging domestic earnings season, while Australian shares advanced 4.1% in AUD and 6.9% in NZD terms.

- Bond returns were positive over the month, as investors sought high quality assets amid growing geopolitical uncertainty. Global bonds (NZD-hedged) rose 1.3% as government bond yields trended lower, while the Bloomberg NZ Bond Composite gained 1.5%, helped by dovish commentary from the RBNZ's February meeting.

Key developments

Global equities navigated a turbulent February, with AI-related anxiety weighing on sentiment across software stocks and asset managers with exposure to the sector.

While major indices held up reasonably well, individual stocks experienced sharp moves as investors paused to assess the disruptive potential of rapidly advancing AI across industries including real estate, trucking, and wealth management.

These dynamics gave rise to the so-called "HALO" trade (Heavy Assets, Low Obsolescence), as investors rotated toward companies with tangible, physical operations and away from asset-light digital businesses.

Defensive sectors including utilities, materials, and energy were among the strongest performers as a result. The US earnings season delivered another round of strong results, however there was a mixed response to the hyperscalers announcing further capital expenditure increases, reflecting growing investor scepticism around the return on AI investment.

Broadening global growth and falling bond yields provided a tailwind for small caps and real estate, both of which outperformed large-cap equities. Japanese equities were the standout regional performer, with the Topix returning 10.5% over the month following the snap election victory of Prime Minister Sanae Takaichi, whose two-thirds supermajority raised expectations of further fiscal stimulus.

While occurring after month end, the US and Israel attack on Iran represents the latest challenge to the global economy via elevated energy prices and heightened uncertainty.

It joins a host of other recent geopolitical events that have been led by the US military including last year's targeting of Iranian nuclear facilities in operation "Midnight Hammer" and this year's US military strike on Venezuela that included the capturing of President Maduro.

While neither of these events had a significant impact on the global economy or markets, this one may be different as the US targets are broader and the Iranian response is more aggressive. JP Morgan, for example, estimate that a scenario where Brent crude oil stays above US$80/barrel, which could reduce global GDP by 0.3% in the first half of this year and increase inflation over the same period by more than 0.5%.

Aside from geopolitics, AI disruption and private credit concerns continue to have an impact on some parts of the global economy.

A key source of funding for “SaaS” (Software as a Service) companies has come from private credit funds and has served to increase rates of investor withdrawals from these funds. So much so that one of the largest, Blue Owl, was forced to gate one of its funds in February.

This dynamic is likely to tighten credit conditions in the non-bank lending space and may well spread wider into the financial sector, as major US banks provide extensive stand-by lending facilities to private credit funds.

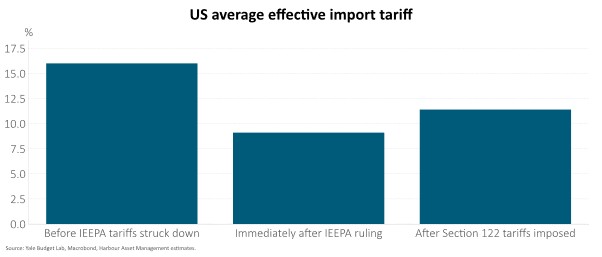

In yet another twist in the tariff saga, the US Supreme Court ruled President Trump's tariffs illegal in a 6-3 decision, finding that the International Emergency Powers Act did not provide sufficient authority. President Trump responded swiftly, imposing a broad 10% tariff on all imports for up to 150 days under separate trade legislation. Significant uncertainty remains over the fate of the US$142 billion in tariff revenue already collected, with FedEx among the first major companies to sue for a refund.

President Trump is expected to travel to Beijing in coming weeks, with the court ruling strengthening China's negotiating hand ahead of those talks.

Closer to home, the Reserve Bank of New Zealand left the Official Cash Rate unchanged at 2.25%, reminding markets that the economic recovery remains at an early stage and that stimulatory policy is likely to be required for some time. It noted that the recent increase in inflation to 3.1% y/y was being heavily influenced by increases in administrative prices that monetary policy has little impact on with components of the non-tradables basket that are sensitive to monetary policy dropping to around historic average levels.

Yields and the New Zealand dollar fell in the immediate aftermath of the announcement, with markets now pricing in just 30bps of hikes this year.

What to watch

The US Administration opted to impose a 10% blanket tariff rather than the previously signalled 15% - representing a large drop in the effective tariff to 11.4% from 16% prior to the Supreme Court’s ruling.

At this lower level, our global research partner, Strategas notes that the policy delivers meaningful tariff relief — equivalent to an estimated US$145bn reduction — and adds to the fiscal impulse already embedded in the Administration’s ambitious 2026 economic agenda.

Market outlook and positioning

The global macroeconomic environment remains positive with inflation largely normalised, healthy rates of GDP growth and loose financial conditions. Inflation in most countries is now at central bank targets or within target bands.

Improving US and Chinese growth prospects over the past 6-9 months mean that most forecasters expect another year of c.3% global growth, which is around trend. Most recently, the effective US import tariff has dropped from 16% to 11%, after the US Supreme Court ruled Trump's tariffs illegal.

This represents a helpful impulse for both lower inflation and higher growth, and along with solid corporate earnings provides a supportive environment for share market returns.

The NZ economic recovery is continuing after the strong GDP bounce in Q3. Data over the past 6 months have shown improvement, on net. These include business and consumer confidence, PMIs and job ads. Low interest rates and export sector strength are likely to sustain ongoing growth.

In its February Monetary Policy Statement, the RBNZ reminded the market of the need for stimulatory policy for a prolonged period to remove the large amount of spare capacity, not implying a full OCR hike in its forecasts until early next year.

Strong export sector revenues will also play a role in our recovery, particularly with the additional benefit for Fonterra shareholders of the capital return associated with the sale of the consumer business – estimated to be as much as $400,000 per shareholder.

The earnings momentum backdrop for both the New Zealand and Australian markets remains positive. The results season for the December period highlighted a positive inflection point for NZ share market earnings.

Company management teams highlighted a more confident tone in post result meetings reflecting self-help strategies and the NZ economy showing signs of a more consistent but still gradual recovery. We expect NZ share market earnings to continue to track higher over the next 12 months driven by company specific initiatives.

While the Australian share market’s positive earnings upgrade cycle may be nearing a peak, it remains underpinned by a robust economy, solid earnings, and a supportive commodity cycle.

Important disclaimer information

| « Market, meet your new Fed Chair | What did reporting season teach us about software and AI? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |