Generate Investment Specialist puts all current market volatility into perspective for investors.

Wednesday, March 18th 2026, 1:07AM

by Generate KiwiSaver

Unsurprisingly, the war with Iran has unsettled global markets. Oil and gas prices have jumped, and investors are trying to second-guess how long the conflict will last and when the Strait of Hormuz will reopen.

As a result, price action has been heavily driven by sound bites - particularly comments emanating from the White House and from those involved in global oil supply.

Mainstream media headlines increasingly portray the Iran war as a protracted and potentially destabilising conflict. This is perhaps no surprise - fear and anxiety sell, particularly when they involve the prospect of another cost-of-living shock.

Several prominent economists have also been quick to highlight potential downside scenarios, adding to the broader sense of anxiety.

Markets, however, are so far behaving as though the shock may remain contained.

The pullback in global equities from recent highs has been relatively modest and has yet to reach correction territory. Even after several volatile sessions, many major indices such as the S& 500 have slipped only a few percent from recent peaks.

Several factors may explain that resilience. There is the so-called “TACO” factor, as well as suggestions that the degradation of military capabilities and financial pressures may eventually force Iran to the negotiating table in earnest, reducing the perceived likelihood of a prolonged escalation.

None of this suggests investors are complacent. Rather, markets are doing what they typically do during geopolitical shocks: pricing probabilities rather than headlines.

The contrast between relatively stable equity markets and sharply moving oil prices - Brent crude recently pushed above US$100 a barrel for the first time since Russia’s invasion of Ukraine in 2022 - highlights where investors believe the real economic risk lies.

Energy supply is the real transmission channel

Disruption in the Strait of Hormuz has driven sharp moves in oil markets. Prices surged toward US$120 at one point recently as shipping routes were threatened, before easing back as markets began pricing in potential emergency responses and diplomatic developments.

These moves matter because oil remains one of the most important inputs in the global economy. Higher crude prices ripple through transport costs, food prices and business expenses, and ultimately into inflation.

In New Zealand the effects are already becoming visible. Petrol prices in some parts of the country have pushed above $3 per litre as the rise in global crude prices flows through to the pump. With the New Zealand dollar also under pressure against the US dollar - the currency oil is priced in - the impact is amplified for local consumers.

The surge has prompted renewed discussion about potential government responses if elevated prices persist. Some commentators have even raised the prospect of fuel-saving measures reminiscent of the 1970s oil crisis, when New Zealand introduced “carless days” - a policy that ultimately proved largely ineffective - to reduce consumption.

While such comparisons make for striking headlines, the global energy system today is very different from that era.

Why this is unlikely to be a 1970s-style oil crisis

Some commentators have taken a more pessimistic view, but there are several reasons why the current situation will not become a replay of the oil crises of the 1970s.

First, the global energy system is far more diversified. Around 80% of global oil supply does not pass through the Strait of Hormuz.

Second, the United States is now a major oil producer and net exporter thanks to the shale revolution, providing supply flexibility that did not exist during earlier Middle East crises (including the export embargo in the 1970s).

Third, the global economy is significantly less oil-intensive than it once was. Oil consumption relative to global GDP is roughly 60% lower today than it was in the 1970s and around 35% lower than in 2000. Modern economies generate far more output per barrel than they once did.

Strategic petroleum reserves also provide a buffer. International Energy Agency members have already discussed coordinated releases of emergency reserves that could inject hundreds of millions of barrels into global supply if necessary.

That is however, not to say that taking out 20% of supply for a prolonged period will not have a material impact, particularly for our Asian trading partners. However, much of the recent move in oil arguably reflects risk premium rather than confirmed long-term supply destruction.

“Higher for longer” oil prices will clearly see a demand response. While the term “stagflation” has begun appearing more frequently, it is also worth noting that the global economy was much weaker and inflation was much higher heading into the 1970s oil crisis. Inflation in the US and many other countries was already running at around 6–7% before the oil shock. That is another important point of differentiation.

Markets tend to price worst-case scenarios first

History suggests financial markets often assume worst-case outcomes during geopolitical shocks before recalibrating as events unfold.

The Ukraine invasion in 2022 provides a recent example with many similarities. Global markets initially sold off sharply as energy prices surged and recession fears intensified. Yet equities eventually recovered strongly later that year once it became clear the worst economic scenarios were unlikely to materialise. Large parts of the world learnt to live without Russian oil and Europe found routes for its gas.

Other political shocks have followed a similar pattern. Markets reacted sharply to sweeping tariff announcements in 2025 before rebounding once the most extreme outcomes failed to eventuate.

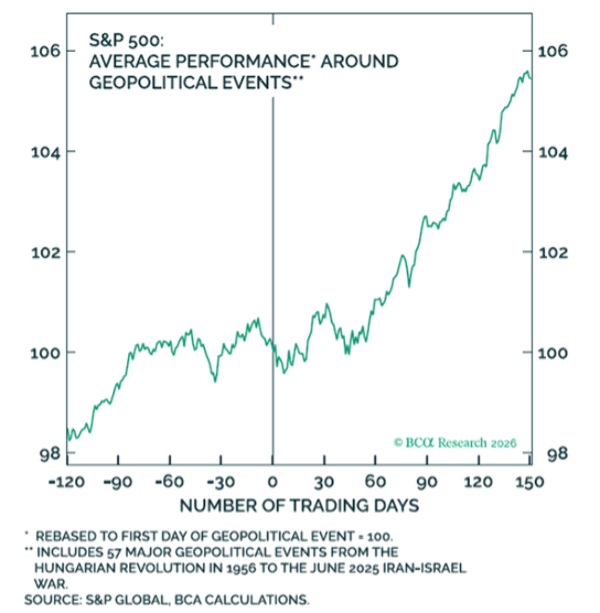

Looking across history, geopolitical shocks have often proved surprisingly short-lived in market terms. Research from BCA suggests the S&P 500 has historically been nearly 6% higher on average five months after major geopolitical events.

Volatility creates opportunity for active investors

Periods like this also highlight an important difference in investment approaches.

Passive investors move with the market. When volatility rises, they experience the full market swing - both up and down - because their mandate is to track the index rather than respond to changing conditions.

Active investors, by contrast, have the flexibility to respond.

Geopolitical shocks often create temporary dislocations across sectors and asset classes. Energy companies may surge while transport or discretionary sectors fall. Defensive assets may become expensive while high-quality businesses are sold indiscriminately.

For active managers, that volatility can create opportunities.

Periods of heightened uncertainty often see investors sell broadly rather than selectively. That can push strong companies to valuations that do not reflect their long-term earnings power. Skilled investors can use those moments to rebalance portfolios, add to quality businesses at more attractive prices, or reduce exposure to areas where risk has genuinely increased.

In effect, volatility can become a source of opportunity rather than simply a source of risk.

Discipline matters more than headlines

Short-term volatility can be uncomfortable, particularly when news flow is dominated by dramatic geopolitical developments.

Taking a broader perspective, markets rarely wait for the news to improve before recovering. In many cases, the rebound begins when expectations have simply become too pessimistic.

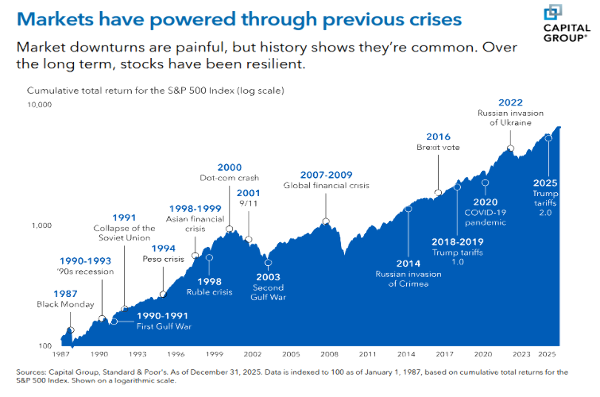

Over the past 150 years markets have navigated wars, oil shocks, financial crises and recessions. Each episode felt unprecedented at the time. Each was followed by recovery.

Ultimately, markets have a long-standing tendency to climb a “wall of worry”. Financial history is filled with episodes that felt existential at the time but proved temporary. Crises are not anomalies in markets – they are recurring features.

Warren Buffett has often referred to geopolitical drama and macroeconomic forecasts as “expensive distractions”. His point is not that such events are unimportant - they clearly matter. Rather, reacting emotionally to them often proves costly for long-term investors.

The current episode illustrates that dynamic clearly. Headlines increasingly frame the Iran conflict as a prolonged geopolitical crisis. Markets, so far, are behaving as though the shock will remain contained.

Equities have slipped but not corrected. Oil prices have surged but remain highly sensitive to news about shipping routes and diplomacy.

None of this downplays the seriousness of the moment. The longer shipping routes remain disrupted, the greater the economic strain. But markets have faced – and recovered from – similar crises before. The pandemic briefly sent oil prices negative.

The Ukraine war triggered fears of a lasting European energy crisis. In both cases, markets eventually stabilised and moved on.

And as markets have repeatedly shown, the moments that feel most uncertain are often when discipline matters most.

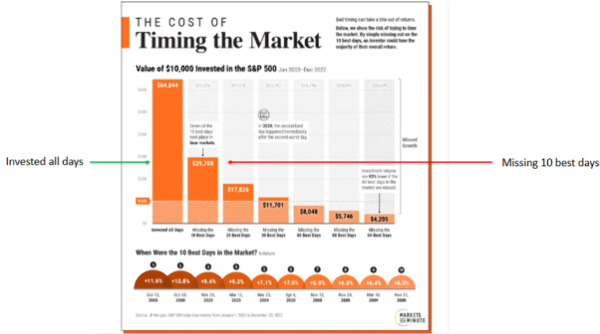

Avoiding short-term reactions to headlines has more often that proven the best course for long term investors. The cost of trying to “time the market” can be costly as the below graphic highlights.

Generate is a New Zealand-owned KiwiSaver and Managed Fund provider managing over $8 billion on behalf of more than 180,000 New Zealanders. With a team of specialist advisers and a track record of strong long-term performance, Generate aims to help Kiwis make informed decisions and build a stronger financial future.

This article is intended for general information only and should not be considered financial advice. All investments carry risk, and past performance is not indicative of future results. To view Generate’s Financial Advice Provider Disclosure Statement or Product Disclosure Statement, visit www.generatewealth.co.nz/advertising-disclosures. The issuer is Generate Investment Management Ltd.