It's better to be first

Stephen Wilson, chief executive officer, Equitable Group of Companies looks at the security of fixed interest investments.

Friday, May 16th 2003, 11:42AM

Open the business section of any newspaper and you will see a raft of interest-bearing investments on offer.

The proliferation of finance companies in recent years, seeking hard-earned investor savings to fund lending and leasing activities, has changed the New Zealand fixed interest market.

Investors tend to see the fixed interest market as simple, easy to understand and inherently low risk – a safe haven that generally outperforms bank deposit returns.

Most fixed interest investments are promoted as “secured”, but is the investors’ sense of security misplaced? Are investors, in reality, exposing themselves to the very equity risk they are seeking to avoid?

Lending is a risk based business and financial services companies can and do collapse – remember Securitibank, RSL, Equiticorp, and DFC to name but a few. More recently we’ve seen a number of high profile defaults in the New Zealand bond market.

So, how secure is a fixed interest investment likely to be in the case of a financial collapse?

The security of an investor’s funds will largely be determined by the recovery that the finance company achieves on its loans. This will essentially be a function of underlying borrower quality and/or the strength of the security held.

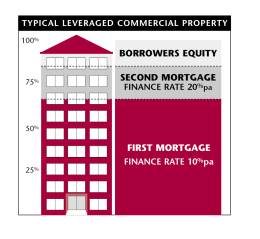

In the property market, the finance rate charged by lenders (ie: the true cost of borrowing including all interest costs, fees etc) will vary depending on the type, size and risk profile attached to a specific loan.

In most cases, as the level of risk increases so does the finance rate charged.

For example, the cost of borrowing second-mortgage secured finance is usually considerably higher than on a first-mortgage basis, reflecting an increased risk premium.

This is because, when a First Mortgagee seeks to recover their debt through the sale of a security property, several things are likely to prejudice the Second Mortgagee’s position as illustrated in the following table:

FIRST MORTGAGEE RISK

- The First Mortgage holder is first in line for

re-payment in a recovery situation

- The level of debt recovery is dependant on the

strength of the security held

- In most cases 100% of the loan is recovered

|

SECOND MORTGAGEE RISK

- Only after the First Mortgagee has been paid

in full will the Second Mortgagee have access to any remaining funds.

- Assessed asset values are usually

significantly discounted in a mortgagee situation (often by 15-20% or

more) prejudicing the Second Mortgagee’s position.

- A First Mortgagee’s priority over sale will

include payment of accrued interest (at penalty rates) together with

recovery of costs incurred, further eroding the funds available for

repayment of the Second Mortgagee.

|

This is not to say second-mortgage or higher risk lending is bad – far from it. As long as the lender in question is not overly exposed to high risk transactions and has a spread of relatively modest loans compared to its capital base, a small number of defaulting loans are in themselves unlikely to put the company (and therefore the investor) at risk.

History has shown us however that financial failures do occur. Investors should therefore understand that in the event of a financial collapse (as unlikely it may seem at the time of making the investment), the level of capital that will be returned is likely to be directly related to the underlying lending risks assumed by the institution in question.

When making higher risk investments, it is important that the return to the investor should adequately compensate for the increased risk being assumed. If a finance company is charging a significant interest rate for the risk that it is exposed to, an appropriate risk premium should be paid to the investor.

The majority of investors in fixed interest securities are not risk-takers. Many are at or near retirement, cannot afford the risk of capital loss, and invest in the expectation that capital return is assured.

Equitable is therefore an excellent place for conservative investors to consider placing funds. It provides attractive rates of return and the peace of mind of knowing that investments are backed by first-mortgage security.

At Equitable all mortgages and investments are held by an independent statutory trustee, Tower Trust Limited, to further protect the interests of the investor.

For a range of investment products that are tax-effective, flexible, offering excellent security and returns it is hard to go past Equitable.

An Equitable Group of Companies advertorial. Stephen Wilson is the chief executive officer, Equitable Group of Companies.

Commenting is closed