The Asian miracle – on track, but risks are higher

Despite recent financial market gyrations, we remain positive on the Asia story. That is not to say the risks have not increased. The global liquidity tide is ebbing, as inflation creeps higher, leaving much of the region vulnerable to weaker global growth.

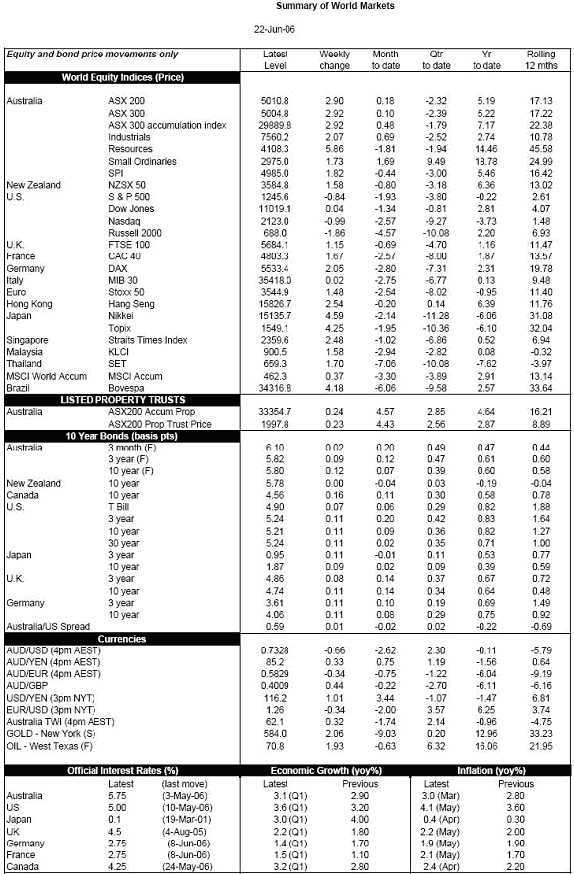

Wednesday, June 28th 2006, 9:28PM

The two regional growth heavyweights, China and India, both put in strong first-quarter performances. China grew by 10.2% yoy as industrial production, business investment, retail sales and trade continued to grow at remarkably stable paces.India came close to matching that with 9.3% yoy growth in Q1. The world’s largest democracy was buoyed by a long-awaited pickup in growth in agriculture, still around 20% of the entire economy. The sector grew by 5.5% yoy, the fastest pace in two years. Manufacturing activity was also a strong performer, up 8.9% yoy. The broad base on which India’s economy is now growing means it is not as reliant on exports as its Asian neighbours.

The expectation is that these two monoliths will slow to around 9% for China in 2007 and 7% for India.

Japan is finally in expansion mode. The economy grew by 3.0% yoy in Q1spurred on by a pickup in business investment and housing activity. Despite steady increases in bank-lending over the past few months, Japan’s central bank is seemingly unable to generate the kind of money-supply growth needed to spark meaningful inflation. The economy is still skirting the deflation abyss as a result.

Despite this, the Bank of Japan are gearing up to put an official end to the yen-carry trade by raising interest rates in the near-future, possibly as early as July 14th. Herein lies the risk for the Japanese economy. All three previous recoveries in Japan have been cut short by an overzealous central bank with an itchy trigger finger. If recent chatter from the BoJ boffins is anything to go by, such a scenario cannot be ruled out this time around.

None the less, favourable job conditions (unemployment is at a seven-year low), gains in income, and solid business investment, supported by healthy profit margins, are all expected to underpin domestic demand next year allowing the recovery to continue to build into 2007.

The medium-sized Asian economies, Thailand, Malaysia, Indonesia and Taiwan, rely more heavily on trade to drive growth and are hence more at the mercy of currency fluctuations. The most spritely of these is Thailand, where strong business investment and exports have helped grow the economy at a 6.1% yoy clip in Q1. Export growth is less strong in Malaysia where growth is currently 5.3% yoy. In Taiwan, weak business investment has been more than offset but strong exports leaving growth at 4.9% yoy. Indonesia is growing at a 4.0% pace helped along by both exports and government spending. Despite higher oil prices weighing on consumer spending, growth in the area is expected to maintain its current pace next year.

South Korea booked 6.2% growth in Q1, boosted by gains in consumer spending and exports. The ever-reluctant consumer is being enticed out of its shell by an improving jobs market and slowly rising wages. Industrial production, however, has slowed for the third consecutive month suggesting overall economic growth will be slightly weaker next year at just under 5%.

Hong Kong is riding on the tail on the Chinese dragon as it continues to act as a mediator between it and the rest of the world. The economy benefits from a substantial mark-up, which some have estimated to be worth 25%, on the goods it receives from China and re-exports to the rest of the world. Strengthening domestic demand conditions are also helping. Strong corporate profits and a boost in business investment are expected to leave the growth profile intact for next year.

Singapore is similarly benefiting from China’s strength. The economy grew by 10.6% yoy, the fastest pace of growth in seven quarters, helped by a strong contribution from financial services and manufacturing activity. Low unemployment and rising wages is shoring up the domestic economy and spurring consumer spending. An expected slowdown in electronics sales, which make up half of all exports, will see growth weaken next year to around 5% from an expected 6.6% this year.

With growth in the US expected to slow this year, and the US dollar likely to decline against most currencies in the region, the risk to growth is to the downside. Rising inflation, and higher interest-rates in the US, suggests tighter monetary policy is also on the cards. Policy has already been tightened this year in China, India, South Korea, Malaysia, Thailand, and Taiwan, and soon to be in Japan.

Moreover, despite the genuine recovery in domestic demand that seems to be underway in Japan, much of the Asia region is still at risk from an external shock. These include higher oil prices, bird flu, or policy error from the US Federal Reserve, the Bank of Japan, or the Chinese authorities.

| « New Zealanders richer than ever | Market review: Classic show-down between earnings and interest rates » |

Special Offers

Commenting is closed

|

|

Printable version |

|

Email to a friend |