Outlook for the Year of the Monkey

Capital markets have had a volatile start to 2016, the Year of the Monkey.

Monday, January 18th 2016, 10:56AM

by Harbour Asset Management

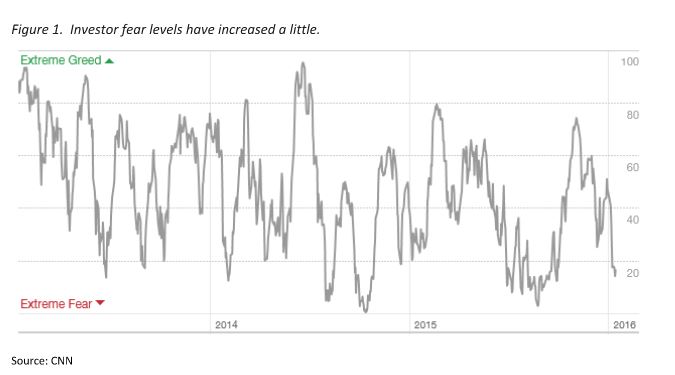

A mix of weak Chinese economic data, further Chinese currency devaluation, new stress in the Middle East, softening commodity prices, North Korea's nuclear blast and broader concerns about global growth have contributed to in an increase in investor fear, as shown in Figure 1. below.

There is a lack of consensus on the outlook for global economic growth which waxes and wanes.

On the one hand, economic growth may remain moderate and inflation may remain low in the short term. This backdrop will provide limited evidence for the US Fed to aggressively increase rates, or for other central banks to tighten.

The World Bank sees global growth sputtering along amid a China slump. The World Bank has cut its global growth outlook for this year by 0.4% and warned of a disorderly slowdown in one of the big emerging market countries, China, which was driving growth. The global economy is now expected to grow by 2.9% according to the World Bank this calendar year and 3.1% next year, compared with a slower than previously expected 2.4% last year.

China is forecast to grow 6.7% this year by the World Bank and slower in 2017, while India grows 7.8% this year and faster the next year. The key message from the global lender is that while the rich world is recovering and adding to global growth momentum, this is being overwhelmed by the weakness in major emerging market economies, apart from India. The BRICS (Brazil, Russia, India, China and South Africa) will only grow 4.6% this year, compared with an expectation of 5.4% in last June's World Bank outlook.

On the other hand, while lead economic growth indicators have fallen recently they remain in positive territory, supporting net global economic expansion.

Risks for capital markets come from the impact of the continued rebalancing of the Chinese economy, and the impact of the unwinding of commodity markets, emerging economies and credit markets.

Rebalancing of Chinese economy

China remains in the midst of a deliberate effort to restructure its economy. The continuing transition from investment-led to consumption-driven growth is destabilising ‘old’ economy Chinese industries more quickly than some had expected.

The recent, and likely ongoing, Chinese currency depreciation is part of China's macro adjustment and comes at a time when China is becoming a capital exporter. The Chinese policy authorities are now shifting policy to tie movements in the Yuan to a basket of 13 currencies. Currency management in China may move towards a managed float regime (like Singapore) with the following key features: the basket of currencies, the exchange rate band and the crawl regime - an intermediate exchange rate regime.

For New Zealand and Australian markets the devaluation reduces Chinese business and consumer’s ability to keep paying the same prices they have been for local goods and services, and may contribute to further weakening in the NZD and AUD exchange rates. The latest move by China in devaluing the Yuan and various stimulus packages may stabilise commodities, but it is unlikely to drive a near term rebound.

We continue to expect iron ore and oil prices to remain weak as oversupply and declining demand takes effect. The slowing rate of Chinese oil demand growth is occurring at the same time OPEC is seeking to squash non-traditional producers, further exaggerating the impact on oil prices.

Changes to China’s capital markets are also challenging.

The Chinese equity market now has a shock absorber circuit breaker whereby the market shuts down if it falls 7% within a day. A number of securities that were restricted from sale have also been released for sale by Chinese regulators at the same time. The down tick limit circuit breaker is a new regulatory protection that went into action for the first time in early January, Chinese investors may have panicked when the market fell 4-5% and sold out faster to get money out before the market locked them out. The protection itself may have made the situation worse - investors now face even shorter time frames to get out of stock if they want to sell, meaning Chinese investors may be more aggressive if they want to get orders executed before limit rules kick in and the market is closed. We expect Chinese policy makers will continue to fine tune Chinese market trading structures.

While the Chinese restructure is likely to unsettle markets in the short term, the fact that there are multiple components to the Chinese economy means, there will continue to be opportunities to invest in companies that benefit from growth in the ‘new’ China.

Credit markets

Credit markets performed strongly over the middle of 2015 as cash moved up the risk curve from bonds to enhance portfolio income streams. In the last eight weeks the Bloomberg US High Yield Corporate Bond index, which measures the performance of a group of publicly issued non-investment grade USD fixed rate corporate bonds, has fallen 4.5%. The US equity markets performance has tracked the High Yield Corporate Bond Index’s performance over the last year.

A large part of recent weakness in the High Yield Corporate Bond index was driven by debt issued by the US oil sector, and other commodity and emerging markets exposed debt issuers. Stabilisation of the Chinese economy may result in an improvement in the performance of the High Yield Corporate Bond index. While US centric, the index provides a useful reference point for other high yield debt markets and may have contributed to a recent increase in New Zealand and Australian corporate credit spreads.

Reduced liquidity and increased volatility in credit markets has contributed to credit fund redemptions, and in some cases the fund closures. Equity markets are partly reflecting the credit market moves, with the ‘yield carry/enhancement trade’ that has supported yield stocks waning over the last two months. Equity investors are also being much more discerning about balance sheet settings and debt facilities for such yield equities. Further reductions in near term credit market liquidity may continue to spook equity markets.

While earnings downgrades continue to outnumber upgrades globally, and in the near term investor fear may continue to increase given changing policy setting in the US and in China, we continue to see the mix of low economic growth/low inflation and easy monetary conditions remaining conducive for local equity market returns. In particularly real interest rates (the nominal fixed interest rate less underlying inflation) remains low and supportive for equities. But investors will need to be active to manage risk and generate returns over the next twelve months.

Investment Implications

Quality & Stock selection to continue to drive returns

Research completed by Harbour Asset Management indicates companies that rank well on quality measures tend to outperform in markets that move sideways or that are weak. Quality tends to also do relatively well when volatility increases.

We expect overall market volatility to continue to increase from recent abnormally low levels. As an active equity manager, greater market volatility may create opportunities for Harbour’s stock investing process to continue to add value by investing in companies with unique growth propositions.

The New Zealand equity market is fully priced. The New Zealand equity market is nearing historical peak pricing based on a simple Price to Earnings measure. Earnings growth expectations for both the New Zealand and Australian (non-resources) markets are reasonable relative to economic and industry change settings. While the New Zealand equity market remains fully valued, we expect global-facing companies to continue to benefit from the historic year-on-year sharp decline in the New Zealand dollar.

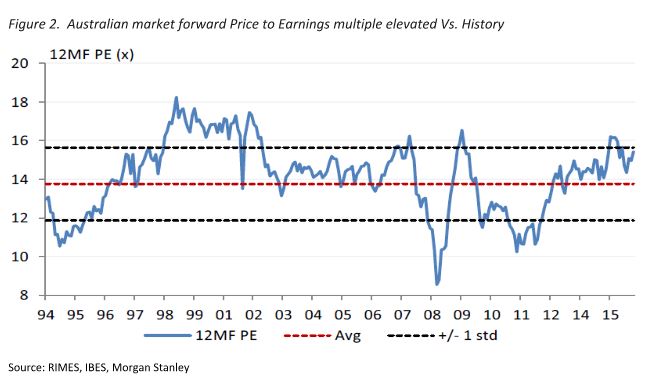

The overall Australian equity market is now priced slightly above long-run average levels, skewed by the resource and energy sectors looking expensive on depressed earnings, as illustrated in Figure 2.

But the Australian equity market considered on a sector neutral basis is cheap, trading below long run average multiples versus other developed markets, as illustrated in Figure 3.

Much of the Australian market’s earnings growth expectation over the next three years (consensus expectations are for -5.3% in 2016, +7.1% in 2017 and +9.1% in 2018) is predicated by a recovery in the energy and materials sectors.

Our investment thesis is not based upon expectations of a recovery in resource and energy sector earnings. We believe the underlying Australian economy is more resilient, and more conducive to company profitability, than many investors have feared.

Both the New Zealand and Australian equity markets offer a 5% plus net dividend yield that remains attractive relative to fixed interest investments.

While credit market movements may slow near term enthusiasm for defensive growth stocks, high quality defensive growth stocks with a pipeline of genuine growth options should keep outperforming over the medium term. Bond yields are not likely to rise enough to unwind investor thirst for high quality yield. But given the massive valuation multiple expansion pure interest rate sensitive stocks have had from the global fall in interest rates there is risk of a de-rating for some ‘pure’ yield stocks if earnings growth is not sufficient. Select quality yield stocks with potential to grow earnings remain attractive in this context.

We think the key investment opportunity lies in high quality stocks that have genuine longer term growth prospects. Sustainable dividend payers and dividend growers are also likely to do well. Self-help productivity programmes and merger and acquisition (M&A) activity will provide a return boost for some stocks.

Given the full pricing of some parts of the equity market, stock selection and avoiding structurally challenged businesses and earnings disappointments remains crucial in influencing portfolio outcomes.

For this reason, in the foreseeable future Harbour’s investment approach will continue to be skewed to those companies that we believe can grow earnings and dividends faster than market consensus assumes.

Shane Solly

January 18, 2016

This column does not constitute advice to any person.

Important disclaimer information

| « A few worrying things | China: Accepting the landing » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |