Lessons from unconventional monetary policy for New Zealand

Central bankers from around the world met at Jackson Hole in Wyoming, recently, to discuss unconventional monetary policy and lessons for the future.

Monday, September 12th 2016, 11:08AM

by Harbour Asset Management

Closer to home, the RBNZ has itself moved closer to unchartered territory, cutting the OCR to an all-time low of 2.00% in August, projecting further reductions, and publishing two scenarios that would push the OCR to around 1.00%.

It is not our central view that the RBNZ will be forced to follow the same path taken overseas. Indeed, the Governor set out in his speech last week that the RBNZ would prefer not to have to cut interest rates aggressively. However, with the OCR already at all-time lows, as part of considering a range of plausible outcomes, it seems timely to consider what unconventional monetary policy might look like in New Zealand.

The main unconventional tools employed overseas have been:

- Negative interest rates

- Quantitative easing

This paper addresses these tools and other new horizons.

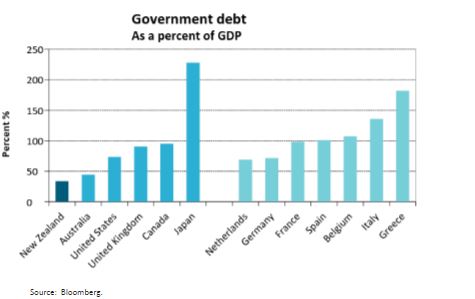

A key conclusion is that, relative to other countries, New Zealand has the benefit of greater room to manoeuvre. In particular, by starting with an elevated exchange rate, there is more scope for an easing in policy to come through a depreciation in the NZ dollar. Similarly, by starting with a low level of Government debt to GDP, there is more ability for supportive fiscal policy to be deployed hand-in-hand with supportive monetary policy.

Interest rates

The RBNZ has not yet officially ruled out cutting the OCR below 0%, to negative levels.

Back in 2009 when the GFC was at its height, the US Federal Reserve and Bank of England initially cut and paused policy rates at 0.25% and 0.50% respectively. At the time, it was thought that cutting interest rates any further would potentially cause more harm than good. In particular, it could have the unintended consequence of hurting the profitability of banks and building societies, unable to pass on negative interest rates to depositors.

That conventional wisdom was challenged in 2014, when official interest rates in Europe and then Japan were cut to negative levels. This initially came as a surprise to markets. However, it reflects that these regions have faced acute deflationary pressures and the lowest potential growth rates. That said, there is a physical limit to how low interest rates can be cut. At some point depositors become incentivised to remove their cash from the banking system when the cost of storage, security and insurance is less than the negative interest rates charged by banks on deposits.

More recently, there has been increasing focus on the adverse consequences of negative interest rates, including on the harm to savers, as well as the perverse incentives and distortions it can create within the financial system.

In response to the surprise Brexit referendum result, the Bank of England cut overnight interest rates from 0.50% to 0.25%, but has signalled that it is likely to finish cutting interest rates just short of 0%, which the market has taken to be around 0.10%.

Quantitative easing

Much like the question of where to stop cutting interest rates, the assets purchased in Quantitative Easing (QE) schemes have also differed for each central bank.

While they shared the same objective of increasing the monetary base and bringing down longer-term interest rates, the application of QE has often depended on many local considerations.

- US Fed: The US Federal Reserve initially began QE in November 2008, buying mortgage-backed- securities (MBS). This reflected that these assets were a large, liquid part of the US financial system. It also provided official support to a market that had been under pressure from the US housing market crash. In later phases of QE – QE1, QE2, and

- QE3 – the US Fed added US Treasuries to be a major component alongside MBS purchases.

- BoE: The Bank of England (BoE) initially began QE in March 2009. Despite being provided scope to buy corporate assets (corporate bonds, loans, asset-backed securities), the vast majority of assets purchased by the BoE were UK government bonds. This reflected a preference for the central bank not to take credit risk, and instead focus squarely on lowering long-term interest rates and “crowding in” other investors into the corporate bond and the equity market.

- ECB: The European Central Bank (ECB) initially began QE in May 2009 by purchasing covered bonds, a form of debt issued by banks and securitised (or “covered”) by pools of mortgage assets. Much like the motivation in the United States, the covered bond market in Europe represented a large, liquid part of the European market for the ECB to easily access. In addition, the ECB was initially keen to avoid purchasing government bonds as part of a QE programme, to avoid even the impression that the ECB was financing national governments. In January 2015, in response to growing deflationary pressures, the ECB changed tack and announced a new expanded asset purchase program, including the debt of national governments, agencies and European institutions.

New horizons: Helicopter money

As the ECB, BoE, and BoJ (Bank of Japan) have scaled up their QE programmes through 2015 and 2016, commentators have increasingly asked what more can be done by policymakers, moving beyond the unconventional tools used so far.

While QE involves expanding the money supply through the banking system, the next step would be expanding the money supply direct to households.

The phrase “Helicopter Money” was coined by Nobel Prize-winning economist Milton Friedman in 1969, and was popularised more recently by Ben Bernanke (“Helicopter Ben”) in his 2002 speech on preventing the threat of deflation.

In these days of electronic banking, what this amounts to is getting money directly into the bank accounts of households, and encouraging them to spend their windfall. In practice, the easiest and most practical way for governments to do this is through a tax cut that is financed by the central bank – so-called “Monetary Financing”.

While Quantitative Easing involves the central bank buying government bonds off another investor in the secondary market, Monetary Financing involves the central bank buying directly from the government in the primary market. As a result, both the money supply and the government deficit increases hand in hand.

Importantly, this form of Helicopter Money requires a new co-ordination between monetary and fiscal policy. This requires a real change of thinking from policymakers. In the immediate aftermath of the GFC from 2009 to 2012, ‘fiscal austerity’ was a key catchphrase in the US and Europe, encouraging tighter, not looser, fiscal policy.

In more recent years, the conversation has moved on, with many commentators calling for more active, stimulatory fiscal policies to take the load off overburdened central bankers. That said, many countries, especially in Europe, are already constrained by high government debt, limiting the room for manoeuvre. Over the weekend in Jackson Hole, Janet Yellen once again reiterated that “as always, it would be important to ensure that any fiscal policy changes did not compromise long-run fiscal sustainability."

What does this all mean for New Zealand?

It is not our central view that the RBNZ will need to apply unconventional monetary policy. However, with the OCR already at all-time lows, it seems timely to consider this tail risk as part of considering a range of plausible outcomes.

In this scenario, we suspect that the RBNZ would stop cutting the OCR somewhere between 0.25% and 0.10%, judging that negative interest rates are potentially more troublesome than they are worth.

If the RBNZ were to undertake a QE program, New Zealand Government bonds would be the obvious assets to purchase. With $75bn bonds outstanding, there is no other NZ dollar market with the same scale, liquidity, or credit quality. This is the simplest approach.

If the RBNZ were having to loosen monetary policy aggressively in response to sharp deterioration in the housing market, it is also likely that mortgage-backed-securities (MBS) would play a role in an asset purchase program. While the MBS market is not currently a large, liquid part of the local financial market, banks would be in a position to quickly structure these securities specifically to sell to the RBNZ. In effect, the banks would be liquidising their balance sheets, exchanging mortgage assets for reserve balances at the RBNZ.

There may also be a practical reason for the RBNZ buying MBS as part of a QE program. The RBNZ would need to be careful that their NZ Government bond purchases weren’t so large that they removed so many bonds that it harmed secondary market liquidity. In that case, the sheer scale of banks’ mortgage assets could become an alternative source of assets to purchase as part of a QE program. (By way of comparison, household debt to GDP is around 160% of GDP, compared to Government debt to GDP of around 30%).

As a small open economy, the RBNZ has an additional tool in its armoury: the NZ dollar exchange rate. If the RBNZ were to ease policy more aggressively than its trading partners (through a lower OCR and/or QE programme), there is plenty of scope for the NZ dollar to fall from its current elevated level. In practice, this could be where the economy receives the most stimulus and immediate impulse to lift inflationary pressures.

An asset purchase program from the RBNZ could be even more potent if accompanied by an expansion in government spending, with monetary and fiscal policy working in tandem.

With one of the lowest levels of Government debt to GDP in the developed world, New Zealand has the luxury of having real room to manoeuvre with fiscal policy. Implementing this approach would require a significant change in mind-set or circumstances. At the moment, the NZ Government is still focused on reducing (not increasing) Government debt to GDP. However, the government has shown flexibility in the past in times of crisis, like the Canterbury earthquakes, to let the fiscal stabilisers (higher benefit payments and lower tax income) kick in to support the economy.

In other words, while the New Zealand Government appears hesitant to pre-emptively loosen the fiscal purse strings, if a recession causes the RBNZ to embark on unconventional monetary policy, it is likely that those same circumstances would also result in more supportive fiscal policy.

Christian Hawkesby, Director at Harbour Asset Management

This column does not constitute advice to any person.

www.harbourasset.co.nz/disclaimer/

Important disclaimer information

| « The West looks East | Invitation to IML’s new Listed Investment Company (QV Income) pre IPO briefing » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |