Equity market pullback

The Harbour Outlook summarises recent market developments, what we are monitoring closely, and our key views on the outlook for fixed interest, credit and equity markets.

Tuesday, November 6th 2018, 1:57PM

by Harbour Asset Management

Christian Hawkesby, Harbour Asset Management

Key developments

For much of the year, the main theme has been global bond yields inching higher as US Federal Reserve continues normalising interest rates; while at the same time equity markets also moved steadily higher, supported by solid global growth.

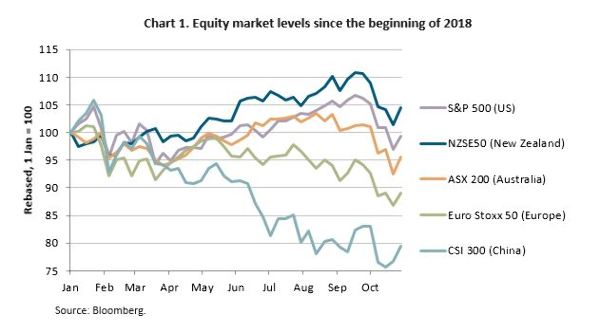

However, finally in October equity markets experienced a noticeable and widespread pullback.

The New Zealand equity market (S&P/NZX 50 Portfolio Index) fell -6.3% over the month reflecting weakness in equity markets globally. The Australian equity market fell -6.1% over October (-6.5% in NZD terms).

Global equity markets sold off over October, with the MSCI Developed Market index down – 6.8%, the worst monthly return since May 2010. Several factors explain the weakness in equity markets, including the cumulative impact of higher global interest rates, tighter funding and liquidity conditions, the stronger US dollar hurting emerging markets, worries about US mid-term elections, concerns about US-China trade wars and US firms not quite meeting elevated earnings expectations in the recent US company reporting season.

Many of these factors have been in play for some time, but in October they combined to rattle investors.

Typically, in this type of risk-off environment, bond yields tend to fall in a flight to safety and liquidity. However, in this case US and NZ government bond yields ended the month little changed, given this late stage of the economic cycle is showing growing inflation pressures which may keep the US Federal Reserve on its established tightening bias.

What to watch

Looking forward, we see three main areas to watch.

First, the current Annual General Meeting (AGM) season will provide an update of the outlook for many businesses. The November profit result season for the September period will also provide an update as to how companies are dealing with changing economic conditions, increasing input costs and structural change including technology disruption. While outlook statements may be cautious, market valuation levels now allow for some slowing in the rate of earnings growth.

Second, as we head into the end of the year, we will learn more about the political risks and tensions that have been hanging over the market. In particular, Donald Trump and Chinese President Xi Jinping are scheduled to have a face-to-face meeting at the G-20 summit in Argentina later this month as the deadline looms for US tariffs to rise from 10% to 25% in the absence of an agreement between the two countries. Another near-term political event is the US mid-term elections, which could influence the ability of the US administration to implement its domestic agenda.

Finally, we will be watching the key upcoming monetary policy decisions, both locally and globally.

At home, the RBNZ’s decision looks reasonably straightforward. Although NZ Q2 GDP and NZ Q3 CPI were both stronger than expected, business confidence has remained depressed and global markets have been volatile. In that case, we anticipate that the RBNZ will hold its line that the OCR is expected to remain on hold through 2019 and 2020, with a chance that the next move could be up or down.

The outlook for US monetary policy looks more finely balanced. Up until now under Jay Powell, the US Fed has taken a steady course by removing stimulus at a rate of 25 basis points at each quarterly meeting. They have also signalled very clearly, so the meeting ahead has typically been priced at 80-90% certain. It has been the solid US economic data that has kept the US Fed on its path up until now.

However, the US Fed also takes financial conditions into consideration when forecasting the economy, and these have clearly tightened with the rise in bond yields, strength of the US dollar and volatility in equity markets.

By the end of October, the market was only pricing a 50% chance of another 25-basis point hike by the US Fed’s December meeting. In our view, the binary decision whether or not to hike could influence the market’s expectation of whether the Fed remains on track to continue normalising or is on a prolonged pause.

Market outlook and positioning

In fixed interest portfolios, we do not have a strong view about the direction of interest rates from here. By contrast, our strongest conviction is that inflation expectations are likely to rise going forward, either because business confidence eventually recovers or the RBNZ is required to cut the OCR aggressively to lift inflation and employment growth.

As such, we see New Zealand government inflation-indexed linked bonds at very attractive valuations, with these bonds providing very cheap protection against inflation rising back to the mid-point of the RBNZ’s inflation target.

In equity portfolios, while we expect equity markets to deliver positive returns driven by solid earnings growth, we can also see that the return of equity volatility is here to stay. So far, the sell down in the equity market has been reasonably indiscriminate, which should provide opportunities for investing in companies with strong cashflow at a more attractive level. In this environment, being active and selective should add value over a passive or buy and hold the market investment approach. We have used the pullback in equity prices to increase exposures to companies with strong franchises that grow through weaker economic conditions and benefit from structural change.

In our multi-asset portfolios, we have closed our underweight positions to equity markets, buying back into these positions at more attractive valuation levels.

This column does not constitute advice to any person.

Important disclaimer information

| « Investing: The future of sustainable property | Time to invest in gold? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |