Asset allocation: Modern Portfolio Theory v Behavioural Finance

In the financial world, a great many asset allocation decisions are made using the Modern Portfolio Theory (MPT), but what about Behavioural Finance? Karl Geal-Otter investigates.

Wednesday, May 29th 2019, 9:56AM

by Pathfinder Asset Management

Karl Geal-Otter

As a theory, it attempts to explain how capital markets operate; with a long list of assumptions that don’t always hold true in the real world. Its little-known sister, Behavioural Finance (BF) is another theory that tries to explain how investors actually operate, rather than how they should operate, which is often at odds with MPT assumptions. In this article we will look at the two theories, and why asset allocators and advisors should take a few more pages out of the behavioural finance book when making allocation decisions.

Harry Markowitz was awarded the Nobel Prize in Economics in 1990, 40-years after he had developed his mean-variance optimisation – what is known today as Modern Portfolio Theory. Since his winning of the Nobel Prize, the theory has become widely used, with investors becoming more acquainted with efficient frontiers and diversified portfolios. Markowitz’ work changed what the investment industry thought of diversification.

Previously it was thought that you should hold 5 or 10 stocks and the job was done. However, Markowitz’ pointed out that the correlation between those stocks, not the number we held, had the biggest impact on diversification. For example, there would be very little diversification benefit from holding a portfolio consisting of Contact Energy, Meridian Energy and Mercury Energy with risk characteristics of each company being largely the same. Instead, Markowitz’ work would suggest holding Contact Energy, A2 Milk and Vista Group – businesses that share some risk (NZ economy) but have very different drivers; energy prices, infant formula demand and technology demand in the cinema industry. This is an overly simplified example, but a good illustration.

Modern Portfolio Theory assumes that we design our portfolios as if we are all mean-variance optimisers; rational, perfect economic beings that always make the correct decision. But, as those of you that have attended a Pathfinder presentation on behavioural finance will know, you are, in fact, irrational humans.

For those of you who haven’t, behavioural finance blows Markowitz’s assumptions of rationality out of the water - we are human, and we often make “poor” decisions that do not reflect real-world facts as a result of behavioural biases.

Daniel Kahneman was awarded a Nobel Prize in 2002 for his work on behavioural finance, 30 years after his key work on Prospect Theory with colleague Amos Tversky. Prospect Theory would lay the foundation for what would become behavioural finance, which suggests that we frame our decisions differently when considering the risk of gains compared to the risk of losses. Unfortunately for traditional finance, this phenomenon was even more prevalent when making financial decisions. Kahneman’s work must be considered at the same times as traditional financial theory, like Markowitz’, suggesting that investment practitioners should pay more attention to how investors actually behave, rather than assuming they are perfect economic beings.

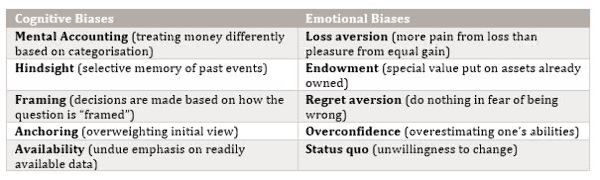

From its Prospect Theory foundation, a myriad of behavioural biases can affect the investment decision process, which can typically be broken into two broad categories, “cognitive biases” and “emotional biases”. Cognitive biases reflect our inability to mentalise or solve a problem and can often be corrected through education, or guidance from a financial professional. Emotional biases are more difficult to correct; they play on our emotional responses to situations (often to our detriment). The table below highlights a few examples:

The two theories offer the opposite opinion of how a portfolio should be constructed. MPT would optimise asset allocation to achieve a well-diversified risk-adjusted portfolio. Behavioural finance would optimise for human emotion, often resulting in an inefficient allocation, but one that the investor is much more likely to stick with.

However, if we apply the learnings from both theories, we could find an asset allocation that is efficient over time and is less likely to be changed by the investor during stressful market environments.

Two examples of this combined construction are:

Pyramid portfolios: is a goal-based decision process, drawing on learnings from behavioural finance, to modify traditional mean-variance analysis. The portfolio uses risk buckets, or tiers of a pyramid, to meet progressive levels of client goals. The goals are in order of priority, with the highest priority goal being at the low-risk base of the pyramid. Once a tier is fully funded the surplus capital (funds) will be invested in the next tier up. There are three broad tiers:

- Personal risk bucket: funds are invested to protect the client from a dramatic change in lifestyle. Investments will include money market funds, bank TDs as well as the family residence. The goal is safety, and returns will likely be below-market.

- Market risk bucket: is used to maintain lifestyle. Investments will include equities and bonds, with an expectation of achieving market returns.

- Aspirational risk bucket: any remaining funds are invested here, and if successful, these high-risk investments could significantly improve the client’s lifestyle. Holdings could include private business, concentrated stock holding and other higher-risk investments (private equity, real estate & hedge funds etc.)

The benefit of this approach is the different levels of risk assigned to each tier. Investors will become more comfortable knowing that their protection assets are invested in a low-risk portfolio. During times of distress this will reduce their desire to sell out of their market portfolio at the bottom. Finally, having an allocation which can improve their lifestyle, without risking their lifestyle protecting assets, will improve their chances of staying the course.

Behavioural modified asset allocation (BMAA): is a deviation-based approach that considers the effects of behavioural biases on investment decisions. Consider a worst-case scenario for a client, after setting the optimal portfolio they go on to abandon it during a stressful market period. The result can be detrimental, as investor’s behavioural biases cause them to sell, typically at the bottom, right before a recovery period.

BMAA begins with that optimal portfolio construction but then allows deviation from that allocation to reduce the chance of behavioural biases impacting decisions (making them sell at the worst possible time). BMAA assess investors and determines whether to adapt to or moderate their behavioural biases. It then considers how much to deviate from the optimal portfolio to reduce biased decisions, building a portfolio the client can stick with. It includes three criteria:

- Relative level of wealth: investors with high levels of wealth compared to their lifestyle can afford to deviate away from the optimal portfolio

- Standard of living risk: is the client’s standard of living at risk if their portfolio was sub-optimally allocated. High standard of living risk reduces ability to deviate from the optimal portfolio

- Biases: the primary type of biases will also impact the decision. Cognitive biases are easier to moderate, proper education can reduce the need to deviate. Emotional biases are more difficult to deal with and will typically need to be adapted to allowing a larger deviation from the optimal portfolio would help the client stay the course.

BMAA comes down to: Can the investor afford to indulge their behavioural biases or does the advisor need to work more closely with the client to moderate the biases? The idea is that allowing an investor to deviate from the optimal portfolio will reduce the chance of complete abandonment during difficult market conditions.

While many asset allocators and advisors will continue to use MPT as the core of their process, it is important to remember that investors are subject to behavioural biases, and we now have a theory that helps to fill in the gaps that MPT can leave. Behavioural finance shows us how investors might react in real-world stressful situations. By designing portfolios that consider some of these learnings, investors will likely have better financial outcomes.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « PE of 1 | Trade tensions impact global growth » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |