A Capital Offence

Fletcher Building made the news again last week in a Radio New Zealand Checkpoint piece focusing on the One Central development in Christchurch, formerly known as the East Frame.

Tuesday, June 18th 2019, 8:00AM  3 Comments

3 Comments

by Castle Point Funds Management

In 2015 the then National government awarded an exclusive contract to Fletcher Building to develop roughly 1,000 townhouses and apartments on government acquired land in central Christchurch. Three other tenders were submitted as part of a competitive process for the contract; one from the Todd Group, one from a joint venture including Mike Greer Homes and Ngai Tahu property, and one from the Chinese backed New Urban group. The unsuccessful bidders felt particularly aggrieved to have lost out on what was an expensive bidding process, with Mike Greer pointing out the disparity between his experience of building more than 1,000 homes per year versus Fletcher Buildings’ near 250, and only a handful of those in Canterbury.

Construction of the first homes was scheduled to start mid-2016 and continue through to 2024. However, it wasn’t until May 2017 that Fletcher Building started construction. The first 20 homes were to be completed in May 2018 with 200 to be completed by mid-2019. The first 20 One Central homes in Latimer Terraces were finally completed and put on the market in November 2018 with asking prices from $1.1m to $1.6m. A substantial sum for a 200sqm 3-bedroom apartment in the middle of what was essentially still a building site. Last week Radio New Zealand followed up on the status of these homes, interviewing the head of Fletcher Residential, Steve Evans. Despite reports that only 3 of the 20 homes had sold, Evans refused to allow Radio New Zealand to view the site or to confirm the sales quantity.

The aspect of the interview that particularly concerned us was Evans’ strong rebuttal of the reporter’s questions on pre-sales, maintaining that Fletcher Building did not need to secure presales in order to start developing. “And we're almost unique in that position because we don't need to worry about getting pre-sales to start development. We're backed by Fletcher Building, we're owned by Fletcher Building and therefore have the balance sheet to be able to deliver." Evans reportedly said it was a case of “build it and they will come”.

The balance sheet that Evans referred to has had a chequered recent history. It was only just in April 2018 that the company was forced to cancel its dividend and raise $750m in a 1 to 4.46 rights issue at a 20% discount to the recent share price in order to avoid breaching debt covenants. This balance sheet is only there thanks to shareholders’ belief that the company will earn a sufficient return on the capital in it. In the June 2018 Strategy refresh, Ross Taylor confirmed that the company’s minimum return requirement was 13% EBIT on funds employed. Despite slow sales to date, Evans’ is apparently confident that the “vision” of attracting more people to live in the Christchurch CBD will prove successful, and he may be right. The trouble is that some brief analysis of the economics of property development shows that delays in hitting “visionary” sales targets can quickly erode shareholder returns.

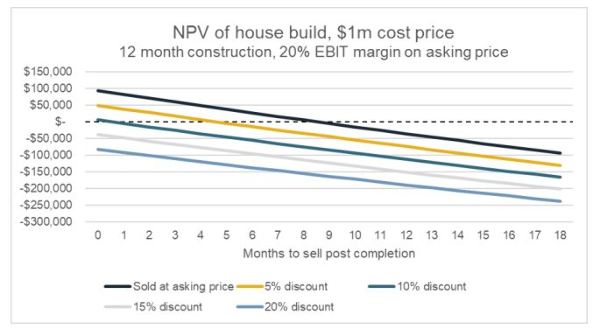

We have made a simple model of the return from the build of a single house below. When things go well a return well above the minimum requirement can be made. We have used an example of a development costing $1m, where 30% of the cost is paid upfront in acquiring the land, and the remaining 70% spread evenly over the following 10 months. If the house is sold for $1.2m, the company reports a 20% EBIT margin. If the house is sold within a month of completion the company also manages an annualised return of 25% on the project and all is well. These metrics are along the lines of those reported by the Residential & Development division over recent years.

However, if the development does not go as expected, things can deteriorate rapidly. A 6-month delay in selling the house results in the annualised return moving perilously close to the target 13%. Add in the extra 6 months in construction time that has occurred at One Central (May 2017 Start date) and despite still reporting a 20% EBIT margin the development has returned less than the required return and actually destroyed shareholder value. Equally, if the house is ultimately sold at only 10% EBIT margin the project destroys shareholders value even if built on schedule and sold within a month.

The terms of the contract between Fletcher Building and the government for the complete development of the East Frame haven’t been disclosed. We know that Fletcher Building is in the process of building 150 houses, 200 were meant to be completed by mid-2019, and the original plan was to build around 900. Did they commit to building all 900? We doubt that Mike Greer offered to, and because he most likely only had access to funding with pre-sales constraints he would not have been able to.

Evans’ assertions about not needing to manage development risks through pre-sales because of access to the group’s balance sheet makes us feel rather uncomfortable. We wonder whether Fletcher Building might have been more generous in the 2015 tender than they should have been. In our opinion, the consequences of this for a single housing development are unlikely to result in provisions of the scale seen for Commercial Bay. However, the Residential & Development Division’s return on funds employed has fallen from greater than 30% in FY14 and FY15, to 18% in FY18. Where to next?

| « Trade tensions impact global growth | Oh Lord's... what if a win comes down to economy rates? » |

Special Offers

Comments from our readers

This philosophy of theirs build them and they will come (buyers)has long been a myth.

I predicted over 2 years ago the outcome which now has proved to be correct.

Not rocket science just plain commonsense and realism.

Question: does the “build it & they will come” mindset exist in the NZ financial services industry, and if so, what are the implications for your client?

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |