Earnings deliver, trade fears fade

The Harbour team examine market movements in the past month, and what they are watching going forward.

Wednesday, December 11th 2019, 1:57PM

by Harbour Asset Management

Investors’ appetite for risk assets further increased in November, as improving activity indicators, a better than expected earnings season, and positive news flow on a US–China trade deal gave investors reason to feel optimistic.

The MSCI World Index returned 3.2% (in local currency) over the month, driven by the high growth IT and health sectors, while defensive utilities and real estate sectors retraced as global bond yields drifted higher.

Global activity indicators have generally stabilised over the past month and data surprises have become less negative, leading to an improvement in many lead indicators that we follow.

Chinese October activity data, however, was unexpectedly poor with the economy continuing to slow due to US tariffs and the absence of meaningful stimulus as policy makers continue to prioritise reducing debt as a proportion of GDP.

The New Zealand share market delivered 4.95% over the month. While improved global sentiment helped the local market, the key driver of the strong performance was the positive reporting and AGM meeting season.

Fisher and Paykel Healthcare (up 15.7%), a2 Milk (up 19.4%) and Ryman (up 17%) were standout performers, delivering a combination of positive results and trading updates.

Despite the market pricing in a 75% chance of a cut, the RBNZ left the OCR unchanged at 1.00% at its November 13 meeting, citing offsetting factors since the August MPS 50bp cut. The RBNZ noted lower interest rates and a weaker currency were providing greater economic support than anticipated at the time of the August MPS.

The decision to leave rates unchanged, however, has removed a large portion of that support. Interest rate swap rates have increased 5-15bp and the market now implies an OCR of 0.90% in one year versus 0.73% prior to the decision.

In currency markets, the NZ dollar trade-weighted index has appreciated more than 3% since the decision.

What to watch

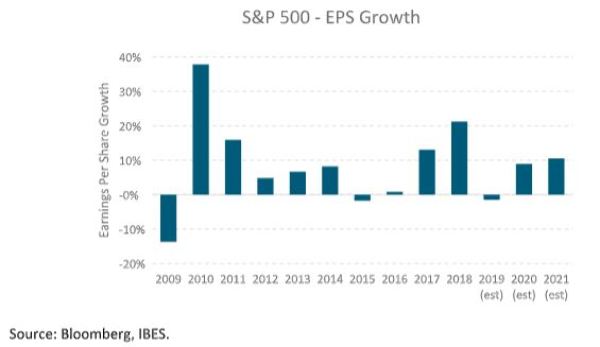

Earnings: There was a high degree of concern going in to 2019 that an earnings recession would hit the market, though this has not eventuated. This concern came after years of strong earnings growth, driven by solid economic growth, monetary stimulus and tax cuts.

In our view, the corporate earnings cycle can remain positive against the backdrop of easy monetary conditions. However, it is an area that warrants scrutiny given the multiple expansion we’ve seen so far in 2019.

NZ Economy: Over recent weeks we have seen stronger retail sales, continued improvement in the housing market, gains in our terms of trade and a bounce in business and consumer confidence.

In the ANZ Business Outlook survey a net 13% of businesses reported an increase in their own activity in November, up 17 percentage points from October and the strongest read this year. Consumer confidence continued to gain as households felt better about the economic outlook, buying major items and the prospect of house price increases.

Expectations of additional fiscal stimulus may be contributing to the increase in confidence. The level of business confidence, however, remains structurally weak and consumer confidence is only slightly above its 15-year average.

Market outlook and positioning

With a picture of bond yields stabilising and economic indicators improving, we have seen a period of better performance for growth as a style, alongside some excellent results and outlook comments from many of our key growth overweight positions highlighting that these type of companies can provide strong returns in many environments.

We continue to be comfortable with large capitalisation growth stocks such as Mainfreight, CSL, Xero and Macquarie Bank which have provided positive updates, alongside a2 Milk which has soothed some of the recent market concerns.

We continue to remain wary of the cyclical companies in both NZ and Australia where ongoing margin pressure may lead to further earnings downgrade risk.

Within fixed interest portfolios, we reduced duration in November, recognising the risk of an unchanged RBNZ decision and better domestic data. Our overall duration position is now neutral, reflecting the competing influences of an improving local economy but persistent downside global risks.

As for much of 2019, our greatest conviction remains in the appeal of NZ inflation-linked government bonds and in the poor value of conventional NZ government bonds (NZGBs) versus US Treasuries (UST).

Market-implied inflation rates increased in October but are still historically low (eg 10-year c.1.2%) and should continue to move higher as the domestic economy improves (even without further capital gain, the yield enhancement make these bonds attractive to hold).

The spread of 10-year UST to 10-year NZGB yields narrowed by 6bp in November to just over 30bp but, considering the respective movement in RBNZ and US Federal Reserve rate cut expectations, NZGBs continue to look expensive.

In multi-asset portfolios, following a strong period of performance for share markets we have trimmed our overweight equities position back to neutral, within which we are relatively overweight to Australasian equities.

While we are wary of valuations in this sector, we believe these equities look relatively attractive against the backdrop of low interest rates. We retain our underweight to global equity markets due to sensitivity around macroeconomic risks.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Has property had its day in the sun? | Five things to look out for in 2020 » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |