Downside risks reduced

The Harbour Investment Outlook summarises recent market developments; what we are monitoring closely; and our key views on the outlook for fixed interest, credit and equity markets.

Thursday, January 23rd 2020, 6:03AM

by Harbour Asset Management

The fourth quarter saw global equity markets strengthen as investor risk appetite improved after a phase one trade deal between China and the US was announced, UK elections provided clarity on the path to Brexit and Chinese authorities provided further economic stimulus. Bond yields spiked higher as the risk of a global recession declined.

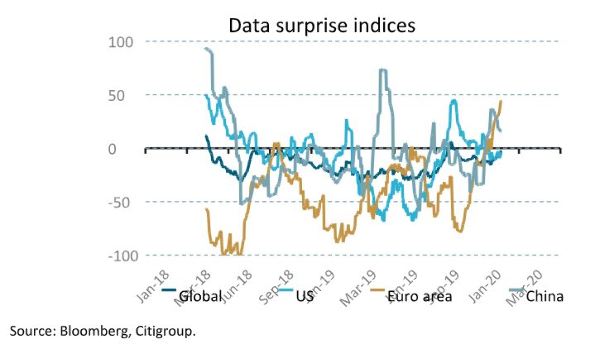

Over the month, global activity indicators have generally stabilised and data surprises have become less negative.

Consumers continue to support the US economy, encouraged by ongoing jobs growth, low interest rates and historically high equity prices.

The People’s Bank of China cut banks’ reserve requirements in early January and the latest Chinese activity data beat expectations.

Manufacturing sectors in Europe and the US remain particularly weak; the weakness in US manufacturing data was confirmed in early January with the ISM Manufacturing PMI again falling short of expectations.

The New Zealand equity market provided continued strong returns in the final quarter rising by 5.3% (S&P/NZX 50 Gross with imputation), lifting the year-to-date return for 2019 to +31.6%.

The Australian equity market managed only a small gain, underperforming as the banking sector continued to fall. For the quarter, the Australian market only rose by +0.7% in Australian dollars but was down -2.5% in New Zealand dollars as the kiwi dollar outperformed the Australian dollar over the period.

Cyclical equity market sectors outperformed defensive sectors both globally and domestically over the quarter as economic risk declined.

Locally, a stronger housing market and merger and acquisition activity in the retirement village sector boosted NZ market returns, while Rio Tinto’s announcement of a review of its Tiwai Point aluminium smelter activities contributed to weakness in the electricity sector.

The NZ economic outlook has continued to improve with a recovery in confidence now well entrenched. Consumer sentiment is above its long-term average with households showing greater confidence in buying major household items, house price gains and the economic outlook.

Firms’ expectations of their own activity (which tends to have a strong relationship with GDP) is the highest since early 2018. On a net basis, firms now report an intention to hire and invest versus a net negative outlook in October.

The level of business confidence, however, remains low and is constrained by structural factors. An announced fiscal boost at the December Half Year Economic and Fiscal Update (HYEFU) also buoyed sentiment.

These factors, paired with a reduction in global tail risks, saw domestic interest rate yields edge higher over the month and quarter.

What to watch

The US consumer: When manufacturing and earnings came under pressure in 2019, it was the US consumer who was the bulwark of not only the US, but also the global economy. US consumption makes up 70% of US GDP and 17% of global GDP, making the strength of the US consumer a factor well worth paying attention to.

As it stands currently, the US consumer is in good shape, with an improving housing market, low unemployment and low inflation all supportive.

Data surprises: Data prints have largely come in better than expected, especially in the Eurozone and China. The US improved, excluding manufacturing. Continued improvement in surprise indices will likely increase sentiment and support equity markets.

Market outlook and positioning

Within Harbour’s equity growth portfolios, we remain selective with active investment positions focused on companies that benefit from structural changes such as:

- urbanisation (particularly in Asia)

- the impact of rapid technology disruption

- accelerating medical innovation and growing demand

- demographic change (both boomers retiring and millennials consuming)

- the rise of sustainability as an economic force.

A key risk for a large part of the New Zealand market remains any resurgence in inflation, or stronger growth that would further lift bond yields. Defensive yield stocks generally have high valuations that could be exposed to a lift in interest rates.

Within fixed interest portfolios, in December we moved from a long to a short duration position relative to the benchmark. We think the positive momentum in the domestic economy is likely to continue and that we are also likely to see inflation rising above 2%.

With market pricing still reflecting an expectation that rate cuts are more likely in 2020, we think the market may shift expectations towards eventual rises in the OCR.

The shift in tone in the domestic market has already taken bond yields higher, with 10-year NZ government stock reaching 1.65% from a low of 1% in October. However, we think there is scope for ongoing increases in yield, most probably centred around the 2 to 5-year maturities.

In multi-asset portfolios, we hold a small overweight to equities. This reflects a reduction in macroeconomic risks and improved activity data creating a favourable backdrop for equity returns.

Within equities, we are relatively overweight to Australasian equities. While we are wary of valuations in this sector, we believe these equities look relatively attractive against the backdrop of low interest rates.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

Important disclaimer information

| « What have eggs, baskets, advice and the 'missing middle' got in common? | NZ equity returns for the next decade? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |