Coronavirus contagion uncertainty

The Harbour team examine market movements in the past month, and what they are watching going forward.

Wednesday, February 12th 2020, 2:05PM

by Harbour Asset Management

Key points

- Risks of an escalation in trade conflict and a disorderly Brexit subsided in December, boosting equity markets further. The improved sentiment was somewhat dampened by rising geopolitical uncertainty in the Middle East.

- Activity indicators were stronger in December, with a further recovery in New Zealand confidence. The US manufacturing sector remains the fly in the ointment.

- Generally improving economic indicators and the reduction of tail risks saw bond yields rise over the quarter, meaning negative returns for fixed interest investments.

- Domestically, the Government confirmed additional capital expenditure ($12 billion over the five-year forecast period) that should provide further support to economic activity. The Government forecasts that the package will add 1.4% to GDP.

Key developments

Markets began 2020 on a bullish note as fears of an escalation in trade tensions between the US and China, and of a disorderly Brexit, were assuaged late in 2019. However, investor worry switched from trade wars to real wars with the US assassination of Iranian General, Qassem Soleimani, causing a military response from Iran. Fortunately, this conflict, which caused some short-term volatility, met a swift impasse.

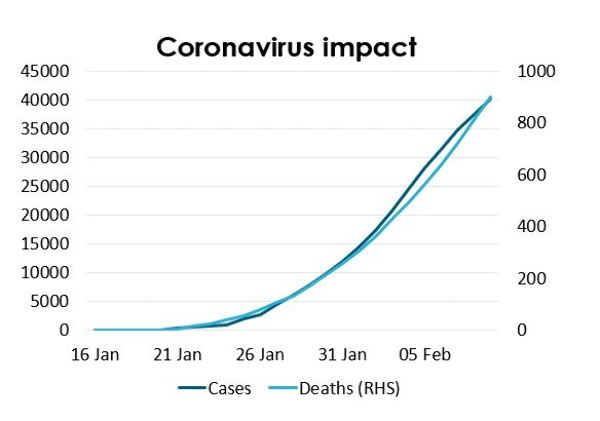

Further volatility ensued later in January following the outbreak of Novel Coronavirus (2019-nCov). This triggered substantial shifts in asset classes. Those sharpest hit were Chinese A-shares, which resumed trading after an extended Chinese New Year break, which fell -7.9% on the first day of trading post the outbreak. China-related, commodity and tourism exposed stocks were also hit hard.

Some healthcare stocks benefited from expected higher healthcare spending. Stocks have recovered strongly in early February.

Outside these two events, January gave investors plenty to be optimistic about.

The US earnings season was especially strong once again allaying fears of an earnings recession. Technology companies fared especially well, with a staggering 36 out of the 38 companies who have reported so far beating consensus earnings estimates. Consumer goods companies also fared well with 82.5% of companies beating consensus estimates, further reinforcing the strength of the US consumer.

Global data surprises have been mostly positive recently, and geographically broad based.

January survey data suggests the US manufacturing sector, which had been disappointing, responded positively to the “phase one” US–China trade deal that was agreed in December. Chinese data had been on the improve following stimulus measures introduced in Q4. Further Chinese stimulus has been announced to combat some of the anticipated economic impact from the coronavirus outbreak.

In New Zealand, the outlook continued to improve in January, aside from the coronavirus risk.

The Government has substantially increased its spending plans over the past two months, turning out to be a better friend to the Reserve Bank of New Zealand (RBNZ) in supporting economic activity than most had anticipated. Not only has there been $12 billion of infrastructure spending announced, Kāinga Ora announced on January 19 an additional $4 billion of borrowing to help its ongoing state housing upgrades.

This adds to a positive picture for the housing market where prices and activity have already been rising in response to lower mortgage rates.

What to watch

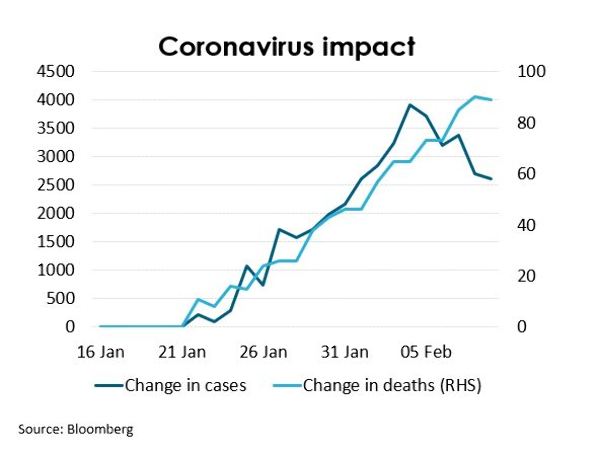

Coronavirus: At the time of writing, the number of new daily coronavirus cases are rising at a slower rate. In previous virus outbreaks when new cases peak, it has been somewhat of a turning point in market confidence.

NZ Earnings Season: February will be the litmus test for local markets with the reporting season starting in earnest. We have already seen some “confessions” ahead of reporting season which largely seem to be idiosyncratic, stock-specific issues. We would expect some companies to call out the bushfires in Australia, plus the coronavirus as potentially impacting future earnings.

Market outlook and positioning

Within Harbour’s equity growth portfolios, the portfolios are overweight versus their benchmarks in selected quality growth companies in the information technology, consumer staples, healthcare and financials sectors, where the potential rate and sustainability of growth may not be fully reflected in share prices.

Conversely, the portfolio is underweight in the New Zealand consumer discretionary and energy sectors where disruption risk remains high; and the utilities, infrastructure, real estate and telecommunications sectors, where valuations are high relative to their potential growth.

Within fixed interest portfolios, we started the month positioned for a shift in monetary policy towards neutral, but coronavirus forced us to consider downside risks. We had initially estimated that the market was not fully appreciating the extent to which data had improved over Q4. We expected that the RBNZ would acknowledge the better data but make it clear that no rate hike was on the horizon due to the persistent gap between current inflation and the top of the target band.

This should remain a feature of the Monetary Policy Statement, when released on February 12.

However, with the coronavirus risks still highly uncertain, and with the possibility of the virus spreading outside China, we need to consider the likelihood of a flight to quality in financial markets and the possibility that growth would slow enough to trigger rate cuts by the RBNZ. Accordingly, we have added duration in our core funds, concentrating this in the 0–3 year sector, where rate cuts would be most influential.

Long-term bond yields remain expensive and could reverse sharply if we are fortunate enough to see a fairly rapid decline in new cases of the virus, as this would enable economic damage to be short-lived.

In multi-asset portfolios, we are cautiously positioned. This reflects two key factors. Firstly, the risks posed by the coronavirus outbreak gives rise to some near-term uncertainty. Secondly, the equity market has had several tailwinds in recent months, which has expanded valuation multiples.

Taking a more medium-term view, we remain optimistic that equity markets should edge higher. Economic data have been improving (notwithstanding the risk posed by coronavirus), equity issuance is low, buybacks are high and earnings look increasingly resilient.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Climate change and investment | Kiwi market ranked fourth over 120 years » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |