Markets this month and beyond

The Harbour team examine market movements in the past month, and what they are watching going forward.

Thursday, April 16th 2020, 6:31AM

by Harbour Asset Management

Key points

- Covid-19 continues to spread globally with cases recently reaching over one million.

- Governments and central banks’ stimulus measures are helping mitigate the impacts of a sudden stop in economic activity.

- Equities posted losses as investors digested the impact of reduced economic activity on company profits, while bond yields in many countries rose as investors baulked at the large increase in bond supply which is required to fund expanding government deficits globally.

- Russia’s refusal in early March to back an OPEC production cut resulted in Saudi Arabia dramatically increasing supply to “punish” the country. Combined with reduced global demand, oil prices have fallen more than 50% year to date.

Key developments

The expanding impact of Covid-19 contributed to a broad-based sell-off in equity markets in March, with many indices retreating to bear markets.

Significant monetary and fiscal policy announcements later in the month helped pare some of the losses sustained by equity investors earlier in the month.

The New Zealand share market closed the month down -12.8% after being down as much as -26.5% during the month in intra-day trading. The MSCI World Index (in local currency) closed the month down -13.7%, after falling as much as -26.2% intra-month.

Despite a 0.75% rate cut by the Reserve Bank of New Zealand (RBNZ), corporate bond yields and long-dated New Zealand Government bond yields rose in March with high intra-month volatility.

While yields initially fell sharply in early March as investors favoured “safe haven” assets, yields soon spiked as investors digested the large increase in supply which is required to fund the Government’s support package.

The risk premium on corporate bonds moved sharply higher as investors sought liquidity and started to price in more distressed scenarios for corporates.

Over the month, market attention was purely focused on Covid-19 developments. The global spread of Covid-19 remains contained, and unprecedented shutdown measures mean a global recession is all but assured.

Control measures are hitting the labour-intensive service sector hardest. Borders are closed, travel is banned and social distancing is either being imposed or voluntarily adopted.

The impact on economic activity is likely to be significant. However, the recent chorus of central bank stimulus has shown that policy makers are aware of the significant risks to economic activity and financial market functioning.

The global fiscal policy response to Covid-19 has also been strong. Japan has announced the largest package at 20% of GDP followed by the US, Germany and Australia (all around 10% of GDP).

Those announced in other countries have been between 2% and 6% of GDP, including New Zealand at around 6% of GDP.

The common thread to most of these is the provision of help to businesses and households impacted by Covid-19, via loans and wage subsidies.

What to watch

Covid-19: Despite having over one million cases worldwide, the scientific community is still coming to grips with Covid-19.

There is a vast array of information that we still do not know, including the case fatality rate and infection rate.

These unknowns will not remain unknowns, and we see the rollout of antibody testing (also known as serology testing) as a key area to watch.

While current testing is focused on finding the live virus, antibody testing will become equally important. These tests will check whether someone has had Covid-19 and since recovered.

Antibody testing is currently being rolled out in the UK, US and China. The results from these tests will not only help derive better statistics but will also give people the confidence to re-enter the workforce with some comfort they have developed immunity to the virus.

There is also an exceptional amount of science being applied to new standards of care (the first step to reduce the impact of Covid-19) and then also to seek a vaccine.

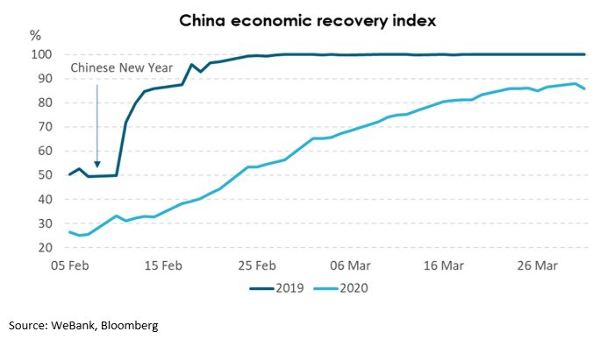

China: Being the initial epicentre of the Covid-19 outbreak, China is also likely to be the epicentre of the global recovery.

So far, balancing a range of different indicators, it looks to us that China is 85%-90% back to work.

Many commentators have pointed to the evidence in China, opening factories and allowing freedom of movement, as a potential signpost to the timing of restarting other economies.

In addition, it seems likely that China will undertake further stimulus in order to boost economic activity.

Market outlook and positioning

The market outlook is tied to several elements.

First, the local and global experience with the control of Covid-19 will be critical – then progress with testing, success with treatments and eventually results of the many vaccine trials.

In addition, government support, from both fiscal and monetary authorities, needs to be monitored alongside rising unemployment. Finally, the extent to which isolation policies are removed will be critical.

Within Harbour’s equity growth portfolios, while we see ongoing risk to earnings from an extended period of Covid-19 containment measures, in price-to-earnings (PE) multiple and yield terms, equity prices have moved to significantly lower levels – reflecting this risk.

Many stocks we invest in will not require additional capital to sustain and grow. A few might, and we will assess those opportunities as they arise.

Current positioning considers the impact of an extended economic slowdown from Covid-19 on earnings and financial risk, favouring those stocks that would do relatively well through the Covid-19 period and those that would do well afterwards.

As always, our focus is on those businesses that could benefit from longer-term structural change, but with the near-term opportunity of investing in such stocks at better pricing levels in a dysfunctional market.

Within fixed interest portfolios, we have aimed to reposition the portfolio where liquidity is the best.

We had started 2020 with a positive view about the New Zealand economy. Our strategy was to be positioned for higher yields, overweight credit and overweight inflation-indexed bonds.

Covid-19 has required a turnaround in our overall position. We have primarily done this with a lengthening in portfolio duration.

We have taken duration from 0.3 years below index to 0.85 years above as at March 31.

While yields are lower for shorter maturities now, longer maturity bonds sit well above cash rates.

While this reflects a much larger issuance programme by the New Zealand Treasury, the RBNZ’s QE programme is expected to limit yield increases and our expectation is that yields should fall in the long-dated part of the yield curve.

We have reduced inflation-indexed exposure a little, but it remains a substantial position.

In the near term, we see Covid-19 as a deflationary shock.

However, over the medium term, due to supply issues and possible preferences by countries to shift away from reliance on imports, we may see some supply-side inflation emerge.

In multi-asset portfolios, we benefited from being cautiously positioned going into March. We extended this cautious positioning prior to the worst part of the sell-off in March.

We have since brought portfolios closer to their long-term strategic asset allocation weights by purchasing more equities at discounted valuations, though we are still modestly underweight risk assets.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Fund update and future outlook | Market timing - what a wicked idea » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |