Bounce back

The Harbour Investment Outlook summarises recent market developments, what we are monitoring closely and our key views on the outlook for fixed interest, credit and equity markets.

Thursday, May 14th 2020, 12:54PM

by Harbour Asset Management

Key points

- Covid-19 infection rates have slowed in most countries with some positive news on potential treatments and the fatality of the virus.

- Equities bounced back strongly digesting positive Covid-19 news flow alongside large scale monetary and fiscal stimulus.

- US earnings season has kicked off with the results to date above expectations, albeit earnings expectations have fallen in recent weeks. Technology and healthcare companies have led the way.

- The action of central banks saw interest rates fall over the month. They are likely to remain low for some time.

Key developments

Share markets recovered in April, reflecting extensive central bank easing, government fiscal stimulus, expectations of a further relaxation of stay-at-home containment policies, the emergence of potential treatments for Covid-19 and some economies getting back to work faster than expected.

Equity market volatility dropped significantly as bond market functioning improved with central banks providing liquidity, allowing asset allocators to operate more normally. Central bank actions also helped interest rates fall over the month.

Global equities (MSCI All Country World Index) gained 10.6% over April in local currency, to be down -13.5% YTD.

The Australian equity market (S&P ASX200) recovered over April, increasing 8.8% over the month (+12.3% in NZD), to be down -16.3% (-14.7% NZD) year to date.

The New Zealand equity market (S&P/NZX50 gross with imputation) was also strong, ending the month up 7.5%, to be down -8.4% year to date. The recovery in the New Zealand equity market was broad with 43 out of 50 stocks in the market delivering positive returns.

While equity market earnings forecasts continued to be reduced, they have been trimmed less than expected, with sectors such as technology and healthcare reporting positive earnings results and profit guidance, offsetting weakness in sectors directly impacted by Covid-19, including consumer discretionary stocks.

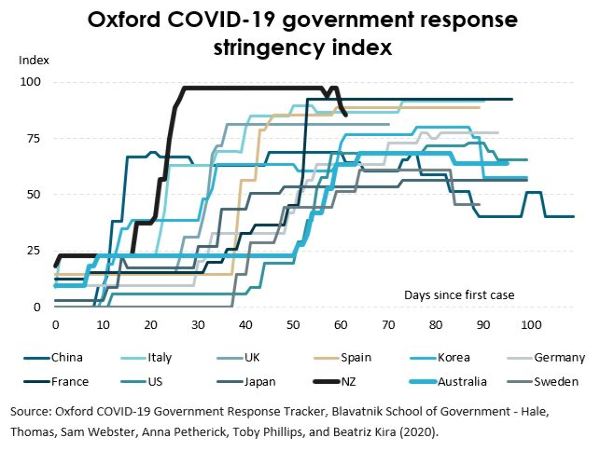

While Covid-19 infection rates have now slowed in most countries, containment measures have led to sharp drops in economic activity and large increases in unemployment, particularly in the labour-intensive service sector.

Since January, the global services PMI (Purchasing Managers’ Index) has fallen 29 points to 24 in April, versus a 10.5-point fall in manufacturing to 39.8.

The International Monetary Fund (IMF) cut its world 2020 GDP growth outlook from +3.3% to -3.0%.

In the US, 26 million people have filed for unemployment benefits (16% of the labour force), suggesting unemployment may peak at more than 20%. The New York Federal Reserve weekly US economic index suggests activity has dropped 12% y/y, versus 4% y/y in the global financial crisis (GFC).

Global policy makers continue to provide stimulus with a focus on providing household and business support to bridge the economic gap created by the crisis. Globally, the amount of fiscal stimulus announced so far is equivalent to 3.8% of global GDP, more than double that seen during the GFC.

New Zealand’s stimulus measures are equally unprecedented at 7% of GDP, with more likely to come in the May 14 Budget. Despite these measures, New Zealand’s success in controlling Covid-19 has likely come at significant economic cost.

While the alert level was reduced from level four on April 27, where economic activity was likely 35-40% below normal, to level three until at least 13 May, where it is likely to be 20-25% below normal.

Assuming we soon move to level two, the Treasury estimates that economic output will still decline 13.5% over the next year and the unemployment rate will reach 9.5%. New Zealanders already claiming unemployment benefits are at 180,000, around 6.5% of the labour force.

What to watch

Covid-19 advancements: Over the last month, the world has learnt a lot about Covid-19. It was only in March when the World Health Organisation (WHO) stated the likely infection fatality rate (IFR) of Covid-19 was 3.4% and many models were released showing the potential devastation the virus could have on the world’s population.

With the passage of time, the real impact of the virus has fallen well below the numbers modelled and antibody testing is revealing an IFR which could be up to 5-10 times lower than what was stated by the WHO in March.

The facts around the magnitude of the health impact of Covid-19 will become more important than ever over the coming weeks as governments juggle the health and economic impacts of the virus.

Treatments are also advancing quickly. As one epidemiologist told us “things that would normally take months to happen, take days when it comes to Covid”.

This statement is perhaps exemplified best by the sheer number of treatments currently in the research pipeline with the Milken Institute counting 199 treatments and 123 vaccines in development.

In April we saw an existing drug, Remdesivir, show effectiveness in reducing hospitalisation time by 31% and mortality by 29% in a placebo-controlled trial. This drug is already being adopted as part of the standard of care in the US.

Vaccines will take longer, however there are milestones we can track as they go through the stages of their trials. The global co-ordination and money behind it are without precedence.

Second waves: We are starting to see containment measures relaxed in many countries including our own. So far, second waves have largely not eventuated to any large degree though Japan and Singapore have seen some increase to cases as containment measures have been relaxed.

China, who were the first to relax measures, have not seen evidence of a second wave and have managed to get economic activity back to 80-90% of pre-Covid levels.

Market outlook and positioning

There is a significant degree of uncertainty regarding the short and even medium-term outlook. That does not mean, however, that investors should stay on the side-lines.

While we expect Covid-19 may continue to impact on economies and markets for the next two years, containment protocols are showing signs of slowing and even stopping Covid-19’s spread.

Additionally, there has been significant progress in understanding many factors, such as the severity of the disease, who it impacts, and what containment measures work best.

Treatment research has accelerated rapidly with many in multiple trials. Vaccine developments may be longer-dated but many trials are also underway.

Within Harbour’s equity growth portfolios, we are observing key structural trends accelerating with Covid-19.

The digital economy and use of technology are changing how we live and work and influencing the long-term profitability of businesses. As a result, we continue to bias investment to those stocks that benefit from the move online, including logistics service providers which are important in the fulfilment of online transactions.

The portfolio continues to have three anchor sector exposures in consumer staples, healthcare and materials which we believe are likely to have more resilient earnings profiles and balance sheet strength.

There will also be opportunities like last month to support business in recapitalising balance sheets, albeit we will be selective.

Being active and selective, in our opinion, ought to provide superior returns for client portfolios.

Within fixed interest portfolios, we held a long duration position throughout April, with this position peaking at 0.9 years early in the month.

As yields fell, we started to reduce the size of the position and with 10-year bond yields down by 0.36% to 0.72% at month end, duration had been reduced to 0.25 years long. Bond yields are now at record lows.

We believe that the Reserve Bank of New Zealand will aim to keep bond yields low through the rest of 2020.

In credit, our strategy has been to emphasise high grade credit, notably Kāinga Ora (Housing NZ) and Local Government Funding Agency (LGFA).

The longer-dated maturities had widened to attractive levels and we added exposure, particularly when Kāinga Ora issued new bonds maturing in 2030.

However, in lower grade credit, we have become more cautious. Early in the month, when the market was under some stress, we made some changes, essentially adding to credits that we thought could survive and reducing those that are now less resilient in tougher times.

Currently we envisage retaining a strong bias towards high grade credit and other issuers where we see strong fundamentals. We are steering away from issuers with high leverage or where access to equity raising is challenging.

We continue to hold inflation-indexed bonds. These have under-performed and we expect soft valuations to persist, given the disinflationary forces introduced by Covid-19. We are likely to reduce exposure cautiously as pricing and liquidity conditions permit.

In multi-asset portfolios, we have a small underweight to equities. This reflects that valuations are starting to look full based on multiples which reflect earnings which are likely to be lower than they were in a pre-Covid world.

Our positioning reflects that many of the downside scenarios one could have envisaged with regards to Covid-19 in the middle of March are somewhat mitigated as we have learnt more about Covid-19, the economic impact and the reactionary functions of monetary and fiscal policymakers worldwide.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « What does the future hold for oil? | Optimistic view of New Zealand equities likely to continue [+VIDEO] » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |