High valuations and rising interest rates = Volatility

In this article we take a look at what higher interest rates mean for equity valuations.

Thursday, March 24th 2022, 9:12AM

by Castle Point Funds Management

This year has started with quite the kick to investors’ solar plexus. Bond yields have jumped, and equity markets have dropped. Not a good beginning to 2022 for either asset class.

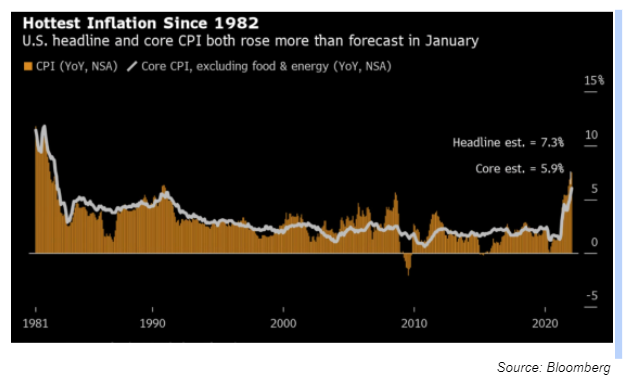

As the chart below shows, for the first time in a generation there is some inflation out and about in the global economy.

Not since 1982 have annualised US consumer price inflation rates been as high as 7.3%.

Inflation has arrived, after a 40-year absence

Central banks around the globe had assumed that, as it had in 1991 and 2008, inflation would top out at around 5% before dropping back.

January and February readings proved that to be way wrong.

As shown above the US Consumer Price Index increased from 5% over the past 2 months to reach highs not seen in 40 years.

This is a potential regime change where a steady diet of low and then zero interest rates is replaced with rising and higher interest rates.

Such a regime shift will require a reset of how equities, and other asset classes, are valued.

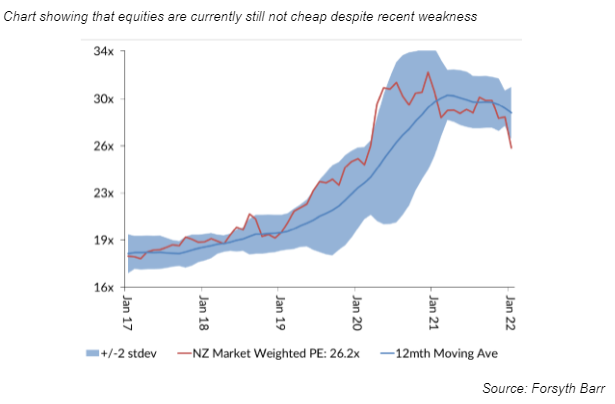

The chart above shows that the price of New Zealand shares had been rising in recent years. The price to earnings of the market weighted by market cap back in 2017 was around 17.5 times earnings, shown by the red line.

That level is at the higher end of where New Zealand equities trade but it’s a realistic price to pay for a company with growing earnings and a healthy dividend.

The chart shows how that ratio, the red line, rose significantly over ensuing years rising to nearly 33 times earnings.

This is a very elevated level indeed, but it could be explained by zero interest rates. In a zero-interest rate environment future profits of a company are barely discounted which means that a discounted cashflow model spits out a higher company valuation than it did previously. Hence the rise to nearly 33 times earnings for the market weight average, which was a huge factor in the share market rising so strongly over this period.

Averages clearly have their uses, but they can also hide some important details. And a major detail is the difference between what investors have been paying for “growth” companies versus “value” companies, and the impact that has been having on market indices (which use a market weight approach). It’s a detail that has already made share markets volatile in 2022 and looks set to continue if the interest rate regime has indeed changed after nearly 40 years.

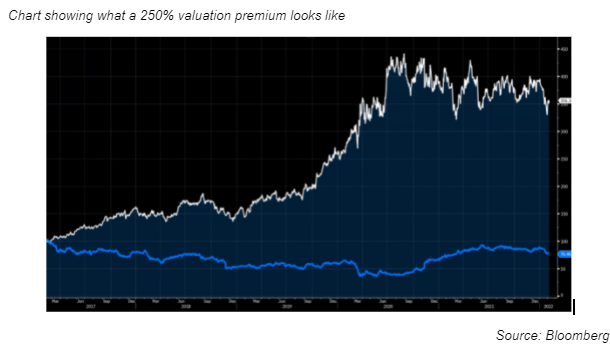

The crucial details lost in the average can be illustrated by taking a close look at two well-known New Zealand companies, Fletcher Building (FBU) and Fisher & Paykel Healthcare (FPH). These companies are similar in several ways. Both long established, FBU, as part of the Fletcher Challenge group, founded in 1910 while FPH was founded in 1934.

They are both listed on the NZX and members of the S&P/NZX 50 index. In 2022 both are, according to Bloomberg consensus forecasts, expected to generate a profit of around $400m. And again in 2025 both are expected to earn a profit of around $500m. But there the similarities end, FPH’s earnings are viewed as far more valuable than FBU’s, with a current price to earnings multiple of 42 times versus the 12x that FBU merits according to the market.

There is a perfectly rational reason to pay more for FPH. It is a quality business with pricing power while FBU is a cyclical business that can be seen as a price taker not maker.

The quantum of that premium is however debatable. Should it be a 250% premium. Personally, I think it’s hard to convincingly argue for that degree of premium, even with zero-interest rates. And in any case, the era of zero-interest rates appears to be over.

There is every reason to expect this very large valuation premium to reduce, as interest rates rise through 2022.

If that valuation gap does indeed close, its going to make market cap weighted indices, such as the S&P/NZX50, S&P/ASX200 and the S&P500, perform worse than the performance of the median member.

This is best explained by returning to FPH and FBU. Due to its far higher price to earnings multiple FPH has a much larger market cap and as a consequence a much larger weighting in the S&P/NZX50, 13.6%. FBU with its lower valuation multiple and market cap only makes up 4.4% of the index.

As a result, the share price moves of FPH have a much larger impact on the index than FBU.

Let’s illustrate this with a totally hypothetical, but far from improbable, scenario.

FPH’s valuation premium drops to 30 times earnings which sees the share price drop over 25%. That move in itself would cause the S&P/NZX50 Index to drop 4%. Another hypothetical but not completely improbable scenario would be the market viewing FBU earnings more favourably, in light of recent earnings upgrades. That could easily see FBU share price rise 25% but that would only cause the S&P/NZX50 Index to rise by 1%. The net result of these two hypotheticals would be a 3% drop in the index, due to the index skew to an expensive large growth company.

This situation is seen across the globe.

This article could have easily referenced Tesla and Walmart where a very similar valuation and index representation distortion is also evident.

Overall, the current combination of highly elevated multiples for large growth companies and market weighted indices creates a situation where the headline index can be far more volatile than the median index member, particularly if we see rising interest rates reduce the premium paid for those mega growth companies. While this would likely be a challenging time for the headline index, the more value focused investors should fare considerably better than the market cap weighted average.

Disclaimer

The following commentaries represent only the opinions of the authors. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement or inducement to invest. All material presented is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. Castle Point may or may not have investments in any of the securities mentioned.

About Castle Point Funds Management Limited

Castle Point is a New Zealand boutique fund manager, established in 2013 by Richard Stubbs, Stephen Bennie, Jamie Young and Gordon Sims. Castle Point’s investment philosophy is focused on long-term opportunities and investor alignment. Castle Point is Morningstar Fund Manager of the Year 2021 – Domestic Equities.

About Stephen Bennie

Stephen is a co-founder of Castle Point. He has over 25 years of investments experience and 18 years of portfolio management experience in New Zealand and abroad. Stephen holds a Bachelor of Commerce (Hons) in Business Studies and Accounting from the University of Edinburgh in 1991 and is a CFA charterholder.

Stock photos can be found here:

https://castlepoint.sharepoint.com/:f:/s/Consultant/EsyXv-TcMlpDn8nDLVXk8tsBWBOMAeERgXPKwmjt8aVzeA?e=BJbuYg

More information can be found at:

www.castlepointfunds.com

| « Tricky transition favours stock picking | Join the Club – Financial wellbeing for Women » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |