The Ides of March

“Beware the Ides of March” is a well-known Shakespearian phrase, but ultimately the month came to pass rather peacefully for markets, despite significant drama within the banking sector.

Monday, April 24th 2023, 10:07AM

by Devon Funds

By Greg Smith, Head of Retail at Devon Funds

Concerns over contagion following the implosion of Silicon Valley Bank (and a couple of others at the “pointier” end of the spectrum) were quickly neutralised by US officials. Across the Atlantic, officials acted equally swiftly to reassure over the state of the European banking sector, with a hastily arranged rescue takeover of Credit Suisse by fellow Swiss peer UBS.

Central banks were also in the spotlight on a number of counts, with questions raised over whether problems in the banking sector were by-products of overly fast and furious rate-hiking initiatives. Any introspection by the central banks came as several signalled they were nearing the end of their interest rate tightening journeys. Indeed, the central banks in Canada and Australia were notable for both hitting the pause button.

In what was a volatile month, a semblance of calm prevailed, particularly in the US where the S&P500 gained 3.7%, while the Nasdaq jumped 6.7%. The kiwi and Australian markets were relatively weaker, with the NZX50 dipping 0.1%, and the ASX200 edging 0.2% lower during the course of the month. While central banks in the Northern Hemisphere had already shown their hands, there was an air of anticipation over recent rate decisions by the RBA and RBNZ - the reactions proved somewhat different.

Ultimately central bank meetings were held in much calmer settings than would have been the case a few weeks earlier. Authorities on both sides of the Atlantic acted swiftly to reduce the risk of contagion or a lack of confidence in the banking sector.

US regulators put in place a long-term funding program for the sector and guaranteed all deposits above the previous US$250,000 cap at the two failed banks. There was also the stated willingness to do more if needed.

The difficulty that Credit Suisse found itself in was unrelated to the collapse of SVB and Signature Bank, but it also found central bank support. The takeover of Credit Suisse by UBS was engineered by Swiss authorities in a bid to shore up confidence in the country’s banks but was also as concerns were running rife over the banking sector globally. The transaction also removed any moral hazard questions as it was not a bailout per se.

This is all while significant measures had already been taken to strengthen the sector since 2008. Confidence is a fickle thing, but authorities have taken substantial measures when previous crisis have occurred to restore faith, and to lessen the extent and impact of future events. This also ultimately allows depositors, and most equity and bondholders, to move on.

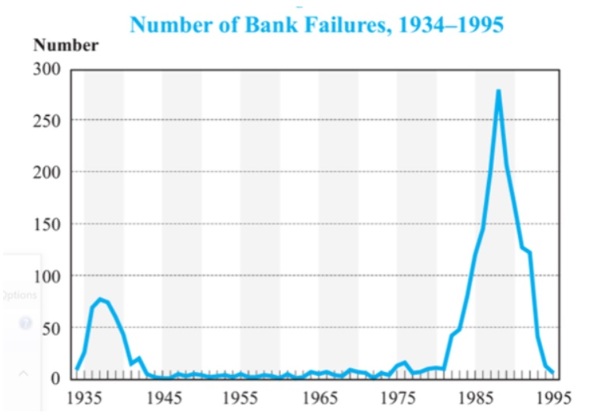

There has been much discussion around the measures taken since the GFC to ensure the resilience of the US banking system. These were significant, but a strong response was needed. Lehman’s was a high-profile failure, and there was concern over the bigger banks, but some others did not make it – there were 25 bank failures in the US in 2008. There was no suggestion this time around that it will be much more than the handful that have already been in the spotlight.

Still, this is far and away from what occurred during the 1980s due to a confluence of economic and regulatory factors. From 1980-1994 some 1,300 savings institutions failed, around a third of the total in existence at the time. In some states, it was worse (9/10 failed in Texas). The response of authorities was wide-ranging and substantial. The Federal Deposit Insurance Corporation Improvement Act of 1991 brought in a series of " corrective actions" to be taken as capital ratios of banks had declined significantly. Nothing close has been seen since, with the GFC mild in comparison.

Source: FDIC

In any event, authorities knew the drill; they acted quickly and will likely implement further measures to mitigate any possible repeat of recent events. Jerome Powell has stated that the case of SVB was likely a very isolated event, but that officials will look at how it happened to ensure nothing like it happens again. In any case, a few isolated events at SVB and Signature Bank need to be taken into context when compared to previous periods of stress in the banking sector.

Developments in the banking sector last month thrust attention on March’s Federal Reserve meeting. The Fed came through with the widely expected 25bps increase in interest rates to a target range of between 4.75%-5%. Fed Chair Jerome Powell acknowledged that financial conditions had tightened following recent events in the banking sector.

The US central bank is however nearing the end of its rate hiking journey, after nine increases since March 2022. Expectations are that there will be just one more rate increase in this year. Markets have clearly had much to contend with already in the first quarter of this year, but ultimately the Fed’s projections are in line with where they were in December. The central bank remains focused on price stability although Powell also noted that the banking crisis would effectively do some of the Fed’s tightening work for it, with a consequent tightening of credit conditions working the same way as a rate hike.

There was a notable change in language from the need for “ongoing policy increases” in the policy rate, to the indication that “some additional firming” may be appropriate. Decisions will though still be made on a meeting-by-meeting basis, based on the totality of economic data. A greater than expected fall in the Personal Consumption Expenditures Index (the Fed’s key inflation measure) for February has added to the view that the end of the tightening line is at hand.

The European Central Bank meanwhile stayed the course with a 50-point rate hike flagged at its previous meeting, taking rates to 3%. One potential reason why the ECB voted to press ahead with a move against inflation is that it was also a tacit vote of confidence in the strength of the banking system in Europe. ECB President Lagarde was at pains to point out that the recent turmoil was very different to what occurred during the GFC. In any case, a recent rise in core inflation has effectively vindicated the ECB’s course of action at this meeting.

Most central bank officials (including the RBNZ) remain vigilant about inflation. The Bank of England put through a rate increase of 0.25%, the 11th consecutive rise, taking the base rate to 4.25%, the highest level in 14 years. The Bank has potentially been looking at a pause, but this view likely changed as inflation jumped to 10.4% last month, five times the Bank’s target.

Some central bankers are pressing pause. The Bank of Canada did so during the month, and the RBA this week pressed pause on rate hikes after increasing them for 10 consecutive meetings since May last year. The decision was well received and put the bid into the Aussie stock market for the seventh consecutive session.

The RBA left the cash rate at 3.6% but did not rule out further tightening of monetary policy in the months ahead. Effectively officials are adopting a “wait-and-see” approach, conscious of the lagged impact of the tightening work that has been done to date. Helping matters is that monthly CPI prints show inflation is coming down, and likely peaked at 8.4% in December last year – February’s CPI was lower than market expectations at 6.8%.

Officials also acknowledged that the economy is slowing down, and that the combination of higher interest rates, cost-of-living pressures and a decline in housing prices is leading to a substantial slowing in household spending. The accompanying statement noted that “while some households have substantial savings buffers, others are experiencing a painful squeeze on their finances”. RBA Governor Philip Lowe said the decision to hold interest rates steady this month provides the board with “more time to assess the state of the economy and the outlook.”

The Aussie labour market meanwhile remains very tight, although officials note that some firms reported an easing in labour shortages and the number of vacancies has declined a little. The RBA expects unemployment to increase as the economy slows.

As does the RBNZ, which did not stop New Zealand’s central bank from coming through with a higher-than-expected 50bps increase in interest rates at the last meet. This takes the OCR to 5.25%, and marks the 11th consecutive rise since October 2021, and comes as inflation had not fallen significantly. The floods and cyclone have stoked inflation further.

The RBNZ believes that inflation is still “too high and persistent.” A complicating issue however is that inflation prints are not (unlike Australia and other countries) monthly. Monetary policy operates with a lagged impact and this is being acknowledged by other central banks. The NZ economy has already slowed down significantly, with the December quarter GDP showing a contraction, when the RBNZ was forecasting an expansion. The NZ economy is probably already in recession and will not have been helped by the weather events in recent months.

Devon Funds Management is an independent investment management business that specialises in building investment portfolios for its clients. Devon was established in March 2010 following the acquisition of the asset management business of Goldman Sachs JBWere NZ Limited. Devon operates a value-oriented investment style, with a strong focus on responsible investing. Devon manages six retail funds covering across the universe of New Zealand and Australian, equities and has three relatively new international strategies with a heavy ESG tilt. For more information please visit www.devonfunds.co.nz

| « When it comes to equities, there is no hiding from the voting machine | Valuation methods are in the eye of the beholder » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |