Market review: How hard will the landing be?

With offshore markets and economies tracking in line with expectations this month Anthony Quirk focuses on New Zealand's economic and market outlook. He also takes a quick look at the KiwiSaver legislation that has just been tabled in Parliament.

Wednesday, March 1st 2006, 4:41PM

by Anthony Quirk

|

This market summary is provided by Tyndall Investment Management New Zealand Limited (Tyndall). To see how the numbers stacked up for various markets around the world in the past month and over the year, visit our Monthly Market Review here |

There is no debate amongst commentators that we are going to experience an economic slow down and this is currently under way. The issue is how far and how hard will the economy decline? We have had some company ceo's berating "gloom and doom" merchants on the basis that things are tracking along fine at present. However, most economists are looking at leading rather than lagging indicators to base their more pessimistic view.

It has been somewhat amusing and frustrating (at the same time!) to see the wringing of hands across the Tasman from the RBA Governor, Ian McFarlane about whether Australia can continue to have its 15th straight year of economic growth. It really is the "lucky country" with the global resources boom now underpinning its economic outlook.

For various reasons the New Zealand economy has had more of a roller coaster ride over that time. This looks likely to continue given its dependence on "soft" and not "hard" commodities, making it more vulnerable at present than Australia to a softening in some commodity prices.

So will we get a hard or a soft landing for our economy? The New Zealand economy has a "curate's egg" look about it; that is, partly bad and partly good.

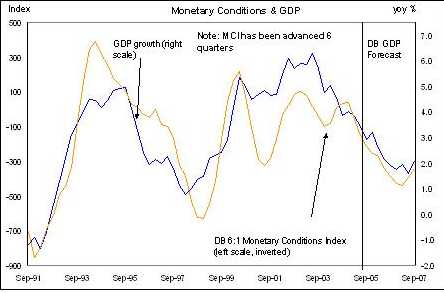

Whatever the weighting applied to these good and bad factors, the New Zealand economy is vulnerable at present and monetary policy settings accentuate this. The combination of high interest rates and relatively high Kiwi dollar meant that, late last year, the MCI measure was at its highest in a decade. (The MCI is a combined measure of interest and currency rates.)

As the following chart from Deutsche Bank shows this is a leading indicator of where the economy is heading.

Source: Deutsche Bank

If the MCI had stayed at its late 2005 levels then the risk for the New Zealand economy was on the down side with a significant chance that we would have a "hard landing".

That is the bad news! The good news is that the recent fall in the Kiwi dollar has loosened monetary conditions. The Kiwi has been called down by market commentators for quite a while and has finally started what should be a material correction. This is partly based around New Zealand's interest rate differential looking less attractive as global rates have risen, as well as recognition we have a weak economy and large trade imbalances.

Currency markets are often based around momentum and the momentum is certainly turning against the Kiwi currently. The Kiwi's fall may provide just the right mix for the RBNZ of a tight domestic economic policy setting (thereby slowing down an overly buoyant housing sector) and some relief for exporters. While not quite the "goldilocks" (neither too hot nor too cold) economy of the US, this combination could see the potential "hard" landing turn into a shallower, but more prolonged, soft landing.

Thus we are at the cross roads of the soft and hard landing scenarios with the Kiwi dollar probably holding the key to which road we will go down.

Introduction of KiwiSaver Legislation

The introduction of KiwiSaver legislation this week into the House is a real milestone for the potential savings behaviours of many New Zealanders. This is potentially the most positive and proactive Governmental policy initiative to lift our savings rate through employer based schemes that I have seen in my over 20 years in the investment industry in this country. However, it has obvious fish hooks. On scanning through the over 200(!) pages that was released (including the draft legislation) my brief comments are:

- the $64,000 question is: will the $1,000 carrot be sufficient to entice employees into a scheme where your funds are locked up to age 65 (or even older if the Government raises the age of eligibility for Government Super payments). The Government is assuming a 25% take up rate and no-one really knows if this is going to be too optimistic, pessimistic or about right.

- the housing deposit assistance for first home owners is a free lunch (similar to student loans) that may attract some younger people but they are not going to be long-term savers in the scheme, as they will probably exit when they move to buy their first homes.

- how many people will only contribute for the first year to get the $1,000 and then stop? This is the nightmare scenario for KiwiSaver providers who would then have to service very low value account balances for many years.

- how does KiwiSaver interact with the massive taxation changes mooted for 1 April next year? For example, what impacts will a marginal tax flow through regime have for potential investors into a KiwiSaver scheme?

- what impact will KiwiSaver have on retail managed funds and financial planners? One only has to look to Australia to see that superannuation savings make up the bulk of investment products with most other investment products relatively less popular.

- which will be the most popular option chosen by existing employer schemes? Will some have duplicate schemes and how many existing employer based schemes will allow employees to "cash out" of their existing scheme, thus actually decreasing savings levels in the short term at least.

- how many employers will contribute as well as the employee? Not many I think, and one way to overcome this would be to decrease the corporate tax rate to 30% and enforce an employer contribution.

- will KiwiSaver be the first step of a process that eventually leads to a compulsory scheme, like Australia? Perhaps Winston Peters will eventually get his way (although well after his referendum)!

In summary, I feel that KiwiSaver is a positive step in the right direction and gives sufficient flexibility so that those who do and do not want to save through it are catered for. However, it is only the start of a long journey – not the final destination.

To see how the numbers stacked up for various markets around the world in the past month and over the year, visit our

Monthly Market Review hereAnthony Quirk is the managing director of Tyndall Investment Management New Zealand Limited (Tyndall).

Anthony Quirk is the managing director of Guardian Trust Funds Management.

| « Weekly Wrap: Where are the markets heading | Weekly Wrap: Kiwisaver legislation » |

Special Offers

Commenting is closed

|

|

Printable version |

|

Email to a friend |