Evening the odds

Wednesday, November 25th 2015, 10:10AM

by Harbour Asset Management

When the RBNZ last released its economic projections in the September Monetary Policy Statement there were two key judgements that drove their thinking:

1. That dairy prices would stay low for an extended period following their sharp fall in the first half of the year.

2. That NZ CPI inflation would get quickly back towards target in the first half of next year; due to the sharp fall in petrol prices dropping out of the annual CPI measure and the weaker NZ dollar in 2015 generating higher tradeables inflation.

Since the September MPS, both of these assumptions have unwound sharply.

Dairy prices have bounced around 40 - 50%, relieving some of that pressure on the NZ economic activity and income, and lifting medium-term inflation pressures in 12-18 months.

However, the complicating factor for the RBNZ is that the NZ dollar has also strengthened around 7% relative to their forecasts. This is important, because it means that near-term tradeables inflation will be softer than otherwise, removing some of the bounce in the annual CPI inflation measure that the RBNZ had been counting on.

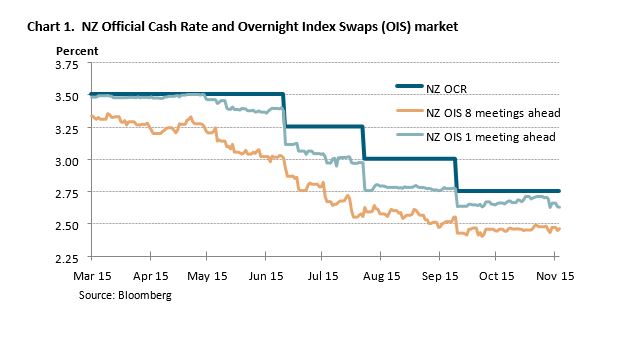

With the directional impact of dairy prices and the NZ dollar offsetting each other, the RBNZ left the Official Cash Rate unchanged at its October Review. The RBNZ also retained the signal that further reduction in the OCR seems likely.

The market is now pricing around a 50% chance of a cut at the December Monetary Policy Statement. Expectations for the terminal OCR rate (proxied by the OIS rate for 8 meetings ahead) have settled around 2.50%.

However, the RBNZ also sent an explicit message in its OCR Review that if the strength in the NZ dollar is sustained, it may require the OCR to be cut further than would otherwise be the case. This, in part, reflects that overall monetary conditions are influenced by both interest rates and the exchange rates.

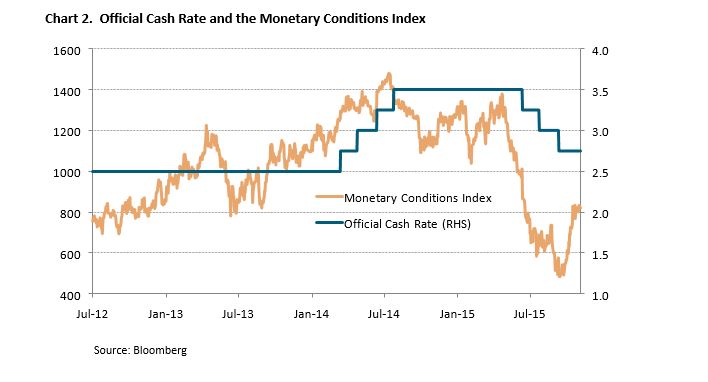

Taking a weighted average of these factors, the RBNZ’s old Monetary Conditions Index (MCI) has risen sharply since the middle of September. In other words, in the absence of action from the RBNZ, there has been a tightening in overall monetary conditions.

By adding this explicit link to the NZ dollar in their statement, the RBNZ has provided themselves a pathway to cut the OCR more aggressively, if the NZ dollar remains elevated and hampers that plans to bring annual CPI inflation back to target.

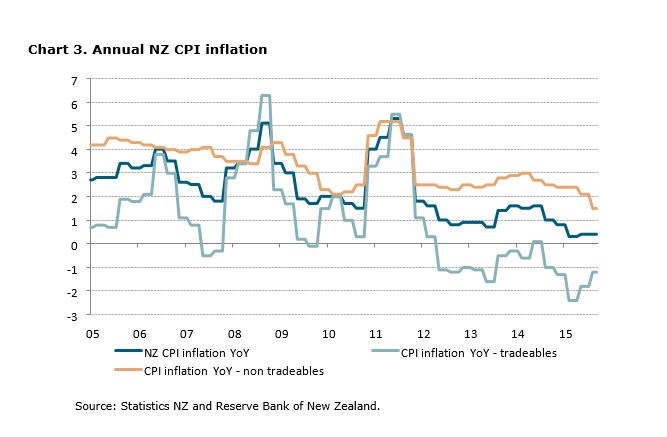

That said, we would still describe the RBNZ at this stage as ‘reluctant doves’, as there is little evidence that they have changed the way they are analysing inflation pressures in a post GFC-world, even with underlying non-tradeables inflation very soft at around 1.5%.

In our view, the balance of risk is that the OCR falls further than currently anticipated by the markets, as the RBNZ eventually comes around to the idea that inflation pressures globally are subdued, and that an OCR at 2.50% or lower is required to keep CPI inflation near the mid-point of the target range.

This column does not constitute advice to any person.

Important disclaimer information

| « What you need to know about income funds | The birth of the Retirement Income Group » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |