Evaluating active managers and Active Share

No two active fund managers are the same.

Friday, February 5th 2016, 10:20AM

by Harbour Asset Management

They differ in style, strategy and how much risk they take. These differences also lead to differential investment performance. To understand how, and whether, active managers are genuinely adding value, investors need to break fund returns into underlying market performance, and returns generated as a result of investment manager skill.

Active Share is a risk measure that may help investors evaluate fund managers.

Active managers attempt to add value by deviating from benchmark indices. Active Share looks at the degree to which the investment holdings in an actively managed portfolio differ from those of a market index or performance benchmark. Active Share helps investors to understand and compare how much idiosyncratic risk is in a fund.

A low Active Share indicates that a fund manager is closely following an index, while a high Active Share indicates the fund manager is choosing investments that differ from the exposures in the fund’s benchmark. For example, a New Zealand equities fund that owns the same holdings, in the same proportions, as its S&P/NZX50 index benchmark would have an Active Share of 0%. A New Zealand equities fund that holds stocks that are completely different from those in the index would have an active share of 100%.

Tracking error volatility, often simply called tracking error, is the traditional measure used to assess active management. Active Share and tracking error emphasise different aspects of active management. Tracking error measures the volatility of the fund that is not explained by movements in the fund’s benchmark index. Active Share quantifies active management at the holdings level and mostly measures manager risk in terms of stock selection. Tracking error is a returns based measure, and is a proxy for systematic factor risks such as tilts to sectors, industries, macro trends and market timing. By measuring active management using Active Share, investors can get a clearer understanding of what exactly a manager is doing to drive performance, rather than drawing conclusions from observed returns.

Some investors are looking to invest in funds that have a high Active Share content as markets become more volatile and to avoid high cost ‘closet indexing’ funds (managers who claim to be active, and charge active fees, but whose portfolios are very similar to the benchmark portfolio). Research by Martijn Cremers and Antti Petajisto of the Yale School of Management indicates that US fund managers with high Active Share outperform their benchmark indexes, both before and after expenses, and that Active Share significantly predicts fund performance. Their research also notes that US Funds with medium or low active share show indifferent performance to underperformance versus benchmark indexes over time, particularly after allowing for expenses.

Investing very differently from a benchmark can contribute to a fund performing better than its benchmark – or worse. Active Share does not show that holding deviations from benchmark index exposures will necessarily deliver better outcomes for investors. Funds with a high Active Share may have a greater dispersion of upside and downside risk. Active Share is not a complete measure of risk. Active Share does not account for portfolio construction, concentration of positions or diversification. For example, including small illiquid stocks or developing businesses in an equity fund will have a higher risk than a large defensive liquid stock with the same size “active” position.

Fund’s with a high tracking error don’t always have a high Active Share – they could be using factor tilts rather than stock selection to generate outcomes. Funds with high Active Share don’t always have high tracking errors – they may be holding idiosyncratic investments that have low non-systematic risk.

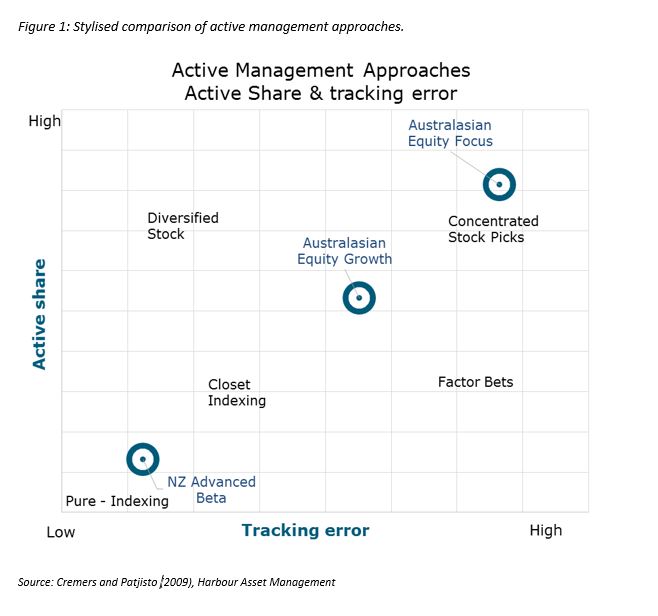

Figure 1 is a stylised comparison of different management approaches, and how they compare in terms of Active Share and tracking error. To provide a local example we have included the positioning of three different equity strategies managed by Harbour Asset Management.

Active Share is measured at a single point in time and needs to be calculated at the portfolio level regularly to be useful. It is difficult to calculate without a detailed data set and it can be cumbersome to create a series going back in time. Active Share may not provide a consistent comparison across different benchmarks and investment mandates.

But perhaps the key benefit in calculating Active Share for investors is that it exposes fund risk changes over time. Risk change over time, as measured by Active Share, could be part of a manager’s strategy. But risk change could indicate style drift (for example becoming more index aware), behavioural biases (for example risk aversion) or excessive risk taking incentives. Any of these changes may deliver investment performance that is very different from what the fund has generated in the past.

Investors can’t make decisions about manager skill or return potential using the Active Share measure alone. Investors considering investing in funds that purport to have a high Active Share component need to have a good understanding of the fund managers investment process and team. Importantly investors need to know whether the fund’s investment approach has been used consistently over a reasonable period of time and whether there has been any changes made to the fund’s investment process.

Investors also need to understand the funds risk profile relative to their own risk tolerance and relative to a reference benchmark (if they are using one). High Active Share funds should exhibit a degree of diversification and investment liquidity (ability to realise investments) that is consistent with investor objectives.

The development of the New Zealand capital market over the last few years gives fund managers a wider range of investment options from which to deliver Active Share. The introduction of new companies to the New Zealand market that may have return profiles that are very different from the broader market, and a broader range of fixed interest investment options, give fund managers a greater range of investments from which to create funds than was the case five years ago.

Active Share combined with tracking error and other measures can give investors a lot of information regarding risk and the style of a fund’s investment strategy. Active share is a useful metric to add to investors fund analysis tool kit especially as a comparison measure between funds over time. But to truly prove that managers with a high Active Share can persistently deliver better outcomes investors need to understand underlying investment processes and teams.

Important disclaimer information

| « China: Accepting the landing | Should fund managers invest in their own funds? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |