Should fund managers invest in their own funds?

Would you buy clothes from a shop whose staff wouldn’t be seen wearing their own brand? Or dine at a restaurant where the chef wouldn’t want to eat? Would you think twice about investing in a company’s shares where the CEO doesn’t want to invest? So how do you feel about investing in a fund where the portfolio manager chooses not to invest?

Tuesday, February 9th 2016, 8:33AM

by Pathfinder Asset Management

Reasons to invest

Why should a portfolio manager invest in the fund he or she manages? The key argument is to align interests – you would reasonably expect a manager to care deeply about how a fund is run if a material amount of their own money is committed to it. It is greater than the alignment from a performance fee or staff bonus – the portfolio manager has exactly the same experience as investors.

When a portfolio manager’s personal funds are at stake it is a sign that they believe in the investment strategy. But not everyone agrees.

Reasons not to invest

There are several reasons given why it may be a bad idea for fund managers to invest in their own funds. These include:

- Managers are already aligned: It is likely the manager’s personal interests are already aligned with investors. There may be a bonus for beating the market, and the threat of job loss for under-performing…. Isn’t that enough alignment?

- Managers may skew to their own risk profile: If a manager has too much invested in a fund, then they may start managing it to suit their own personal preferences and risk profile. It may make them fearful of taking on risk. This argument is valid if a manger were to commit too much of their personal wealth to a fund or if they own a very large portion of the fund (in which case they may feel it is their own personal fund).

- Using personal investment brings in emotion and is a bad way to align: You may want the portfolio manager to stay dispassionate and not get emotionally connected with the fund. Could that lead to better decision making?

What the evidence tells us

A 2008 paper published by Russel Kinnel (Director of Fund Research at Morningstar) looked at investment in US mutual funds by the individual portfolio manager responsible for the fund. The research was particularly interesting given that US managers had only recently been required to disclose their personal holding. The research was later repeated in 2011.

Conclusions from the 2008 paper were quite clear –

- Whether the individual manager invests (or does not invest) in the fund they manage is a “great tool” for choosing funds.

- There were “staggering” levels of managers not investing. Many categories had between 50% and 70% of portfolio managers not investing in their funds (for example 47% of domestic US equity funds, 61% of global equity funds and 71% of balanced funds had no portfolio manager ownership).

- Funds that Morningstar rated highly had a much higher average investment ($354,000 per fund) compared to funds that Morningstar did not favour (average investment of $52,000).

The report’s overall view was don’t invest where the portfolio manager doesn’t.

What does the NZ disclosure tell us?

In NZ we are not required to disclose how much a portfolio manager invests in a fund they manage. What we are required to disclose is how much the board of a fund manager company invest in their funds. It shows a commitment by the board – but is not the same as the portfolio manager investing. This information is included in the related party note to each fund’s financial statements registered on the companies.govt.nz website – unfortunately it is very hard to navigate the website and find the information.

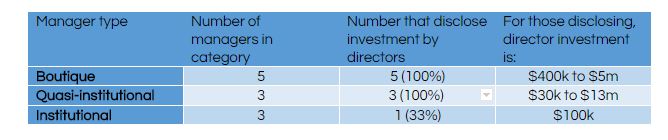

The results from a sample of 11 funds from different NZ fund managers are set out in the table below. The managers are broken into three groups. Boutique managers and large financial institutions need no explanation. The “quasi-institutional” category falls in between these – it is either a very large boutique, a manager with significant institutional shareholders or a manager that has no direct ownership by principals working day to day in the business. The results are:

Does this tell us anything useful? Given the table only covers one fund from each of 11 managers, it is a small sample. We can draw some loose conclusions – the question is then whether these conclusions are true across the entire universe of NZ funds:

- The directors of boutique managers (including large boutiques) typically invest in their funds, and in material amounts

- While boutique fund managers disclose their director investment in funds, only 1 in 3 institutional managers make this disclosure (this probably means directors of 2 out of these 3 institutional managers have no holdings in their funds.

- When disclosed, the amounts invested by the board of larger managers in their own funds can range from very insignificant ($30k) to very significant ($13m).

It would be helpful to know what the portfolio manager (as well as the board of a fund manager) invest in their funds. NZ disclosure could be improved on this front – unfortunately it was not adopted under the new Financial Markets Conduct Act regime.

Final thoughts

Investment by a portfolio manager in a fund they manage does show a degree of personal commitment to the fund and alignment with their investors. Past Morningstar research showed this may be a good indicator of fund quality. In NZ managers are not required to disclose holdings of their portfolio managers – but this should not stop financial advisers and investors from asking.

One research house (which has since exited the NZ market) shared an interesting anecdote with us about investment by NZ portfolio managers. They were surprised how few NZ fund managers were prepared to disclose how much their portfolio managers invested in their funds, citing privacy reasons. When told that without disclosing that information there would be no fund rating, the fund managers would relent and disclose holdings. No surprise to hear that when the manager was reluctant to disclose the portfolio manager’s holding was invariably zero. As a general rule, information about aligning interests that fund managers are reluctant to disclose is likely to be exactly the information investors should be demanding.

Here’s a great quote on the issue to finish up:

“I can’t think of why anyone should invest in a fund that its own manager doesn’t invest in. True, higher investment levels aren’t a guarantee of success or an ethical manager, but at least they show managers believe in the funds…”

Russel Kinnel, Director of Fund Research at Morningstar, 2008

John Berry, Director

Pathfinder Asset Management Limited

Seek advice: Pathfinder is a fund manager and does not give financial advice. Seek professional investment and tax advice before making investment decisions.

Disclosure of interest: John invests in all four of Pathfinder’s PIE funds.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « Evaluating active managers and Active Share | Super fund invests in a new strategy » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |