Giving inflation a chance

A key theme for markets moving into 2016 has been the persistence of low inflation, and the battle facing central banks to avoid low inflation becoming embedded within the expectations of households and businesses.

Monday, April 18th 2016, 11:41AM

by Harbour Asset Management

Both the RBNZ and US Federal Reserve met in mid-March and delivered decisions that underlined their determination to lift inflation from its recent low levels. By keeping policy interest rates lower for longer, both central banks have given themselves a greater chance of hitting their future inflation targets.

The RBNZ’s decision to cut the OCR came as a surprise to many local economists who had ruled out a move in March based on the Governor’s speech on 3 February. To recap, in February the Governor said that it would be wrong for the RBNZ to take a “mechanistic approach” to current low headline inflation, as that would not draw on the flexibility in the Policy Targets Agreement (PTA).

While some bank economists may quibble with the timing, they were all expecting an OCR cut at some point in the first half of 2016. The evidence in favour of a cut became overwhelming given an elevated NZ dollar, a further fall in dairy prices, a moderating Auckland housing market, higher wholesale overseas funding costs for banks, and fragile global financial markets.

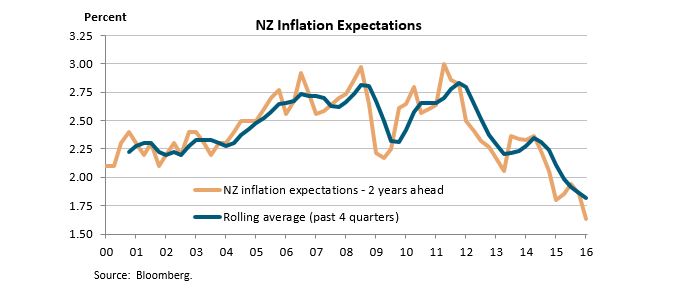

However, the key factor that tipped the RBNZ to act decisively was the sharp fall in inflation expectations. Up until December, the RBNZ were clinging to the idea that NZ inflation expectations remained “well anchored”, despite survey measures trending down from 2.5% to 2.0%. The survey measures fell materially again in February. It is hard to remember a domestic development causing the RBNZ “concern” since the Christchurch earthquakes. However, that is the language the RBNZ used to describe the prospect of low inflation becoming imbedded stubbornly into wage and price setting behaviour.

Source: Bloomberg.

In many respects, the March Monetary Policy Statement reaffirmed what was already clear. That is, the primary objective of the RBNZ is to set interest rates to try and keep future inflation near the 2 percent target midpoint. When setting interest rates, all the other stuff in the Policy Targets Agreement (PTA) about taking into account the efficiency and soundness of the financial system, and seeking to avoid instability in output, interest rates and the exchange rate are secondary considerations. First and foremost is having a plan to meet the inflation target in the future.

What came as more of a surprise in March was the US Fed’s dovish press statement and economic forecasts. As always, there had been a cacophony of voices across the regional US Fed Presidents and FOMC members expressing a range of views leading up to the policy meeting. However, the US Fed’s forecasts and Yellen’s press conference were clearly dovish. Back in December, they had forecast the US Fed Funds rate to be lifted four times in 2016. In their March forecasts this was revised back significantly to just two hikes in 2016, when the market had only expected this to be trimmed to three.

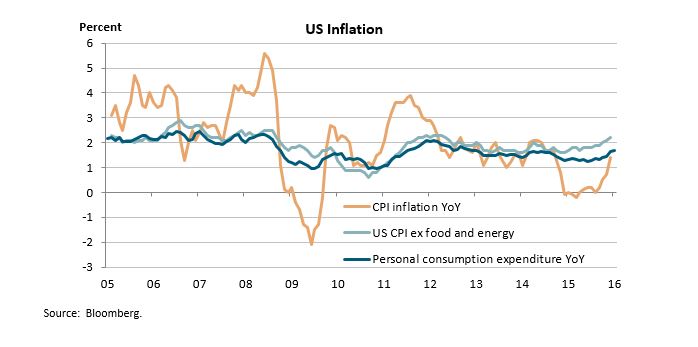

On the surface the US Fed’s dovish forecasts are hard to reconcile with the very solid performance of the US economy. Jobs continue to be generated at over a rate of 200,000 per month, the unemployment rate has halved since the GFC to 5%, and inflation and wages are showing their first signs of lifting (see chart).

Janet Yellen’s speech at the Economic Club of New York on 29 March outlined the US Fed’s position in more detail, and could have been entitled: “Why Yellen thinks only cautious gradual moves in policy will be necessary”. It included a virtual laundry list of worries and risks consuming US monetary policy makers:

- Lower global growth forecasts.

- Global market turbulence.

- Weakness in manufacturing, net exports and energy sector.

- Risks around China, oil market, inflation expectation becoming unanchored.

- Wariness that the recent rise in the core PCE deflator may be short-lived.

- An awareness that the use of the Fed Funds rate is asymmetric – they have plenty of room to hike if needed, but little room to cut before alternative tools would be required.

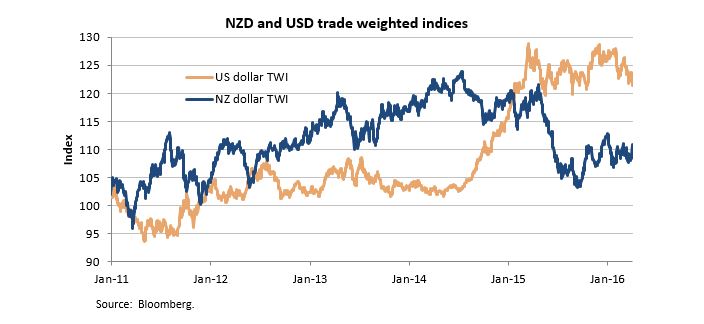

The US Fed’s dovish stance in March could have significant implications Down Under for the RBNZ, particularly given the ensuing US dollar weakness.

The RBNZ’s Monetary Policy Statement retained an easing bias. Their forecasts for the 90 day bank bill rate imply an additional 25 basis point cut, somewhere through the middle of the year. Given the RBNZ’s mild preference to change interest rates when armed with a full set of economic forecasts, the market only placed around a 33% chance of a cut at the next interim OCR Review on April 28.

However, since the March Monetary Policy Statement, dairy prices and NZ inflation expectations have remained subdued. Furthermore, US dollar weakness following the dovish Fed statement has seen the NZ Dollar strengthen to around 3% above the RBNZ’s assumption for the June quarter. These developments help tilt the risks toward the RBNZ delivering cuts sooner rather than later, making the 28 April OCR Review very much a “live meeting”. We would ascribe around a 60% chance that the OCR is reduced 25 basis points to 2.00% in April.

A key theme common to RBNZ and US Federal Reserve decisions in March was their determination to lift inflation from its recent low levels. By keeping policy interest rates lower for longer, both central banks have given themselves a greater chance of hitting their future inflation targets.

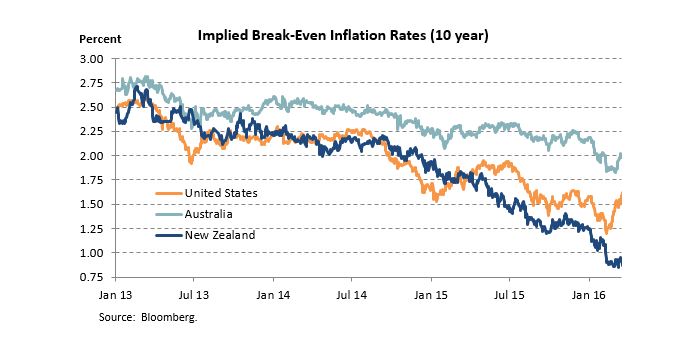

One measure of inflation expectations derived from financial market prices are so-called breakeven inflation (BEI) rates. These are broadly calculated as the difference between the yield on a traditional nominal bonds less the real yield on an inflation-indexed linked bond of a similar maturity. With the NZ 10 government bond yielding under 3% and real NZ 10 inflation linked bond yielding around 2%, NZ breakeven inflation (BEI) rate has been very depressed below 1% since the beginning of the year. This is considerably below the mid-point of the RBNZ’s inflation target.

Low BEIs have been part of a global theme through 2014 and 2015, as oil prices fell, headline inflation was stubbornly low, and fears of deflation emerged. However, in recent months a number of large global bond managers, such as Blackrock and Pimco, have recommended buying inflation linked bonds as cheap insurance against inflation lifting in the future. US breakeven inflation (BEI) rates have lifted from below 1.25% to 1.60%, in part because the US Fed is taking a more dovish stance and giving inflation a chance to rise. By global standards, current NZ 10 year BEIs of 0.85% make NZ inflation-linked government bonds appear relatively cheap, especially if the RBNZ is indeed determined to meet its inflation target in the future.

Christian Hawkesby

christian@harbourasset.co.nz

This column does not constitute advice to any person.

Important disclaimer information

| « A fund manager fee conundrum | The 'how' and 'why' of negative interest rates » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |