The 'how' and 'why' of negative interest rates

The interest rate outlook has shifted from “lower for longer” to now “very low for very long”.

Wednesday, May 4th 2016, 10:13AM  1 Comment

1 Comment

by Pathfinder Asset Management

In fact rates have gone so low that they are negative in many countries. In this commentary John Berry from Pathfinder looks at negative interest rates – in particular how central banks use them and what are they trying to achieve.

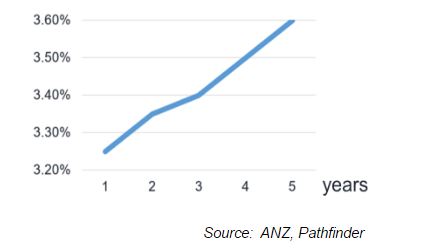

To understand how negative interest rates work it is worth doing a refresher on the yield curve. This charts the interest rates offered for investments (vertical axis) over time (horizontal axis). Below is the yield curve for NZ dollar term deposits with ANZ. An investor receives a higher rate for locking money away with ANZ for a longer term (3.60% p.a. for 5 years) than the investor receives for a shorter term (3.25% p.a. for 1 year). The ANZ curve is consistent with conventional thinking on how a yield curve should look – it is upward sloping and all of the interest rates are positive.

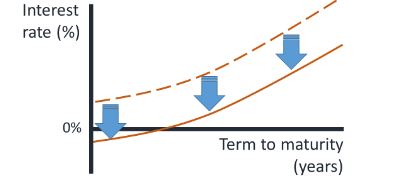

Something very odd has happened in recent times – interest rates have gone negative. Central banks have been eager to shift rates at the “front end” (shorter term rates) lower – until they have pushed them below zero. At a negative interest rate you pay a bank to hold your deposit and the bank pays you to take a loan. This is the opposite of how the world should be. Here’s how the “new” yield curve looks:

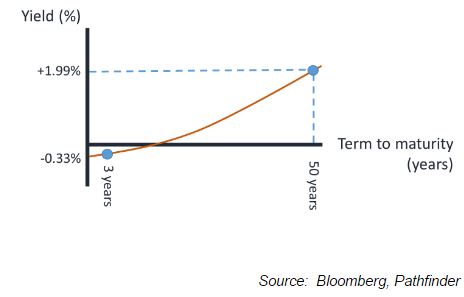

Putting some real numbers to this curve we can use French government bonds. The 3 year rate is negative (-0.33%) while the 50 year “long end“ is positive (+1.99%). This is shown below (not to scale):

Negative interest rates are no longer uncommon. For a duration of 5 years or less they are negative in countries including Switzerland, Japan, Germany, the Netherlands, Sweden and France. But not all interest rates or investments in the country are negative. Central banks set their “official” overnight rate to negative (the equivalent to New Zealand’s OCR). This imposes a cost on banks for depositing excess reserves with the central bank. As an alternative to depositing with the central bank, a bank can buy short term government bonds. The result is these are pushed negative as well (i.e. converging on the central bank rate).

Why would central banks do this?

The thinking behind the negative rates is to encourage growth in the economy. If banks are penalised for depositing reserves with the central bank, they will be encouraged to lend funds to businesses instead. This productive lending should then create jobs and growth. Lower rates could discourage offshore investment into deposits, possibly weakening the currency which again promotes growth.

But there can be unintended consequences. Will consumers be incentivised to hoard cash rather than deposit it in the financial system? (Capital Economics believe if rates went below negative 1% for savers, this would be the threshold around which behaviour changes). Will businesses want to prepay their suppliers before product is provided to avoid holding funds at negative rates? (This is the exact opposite of what Fonterra are in the headlines for with their extended 90-day payment terms to suppliers). Will negative rates fuel speculative bubbles? (There is talk of negative mortgage rates in Europe where a borrower is paid to take out a floating mortgage!)

Why would investors accept negative rates?

Paying for a bank to hold your deposit seems bizarre – but there are rational reasons why an investor may choose to do this. You may not trust the creditworthiness of corporate bonds in your country (Italy?). You may want to protect capital at any cost and invest only into a “safe haven” government bonds (Switzerland). Or as a saver you may be experiencing inflation that is more negative than your interest rate – in which case you are still ahead in “real” terms (Japan?).

Are all rates negative?

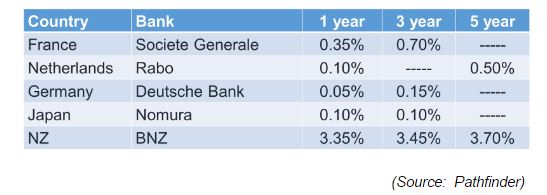

The short answer is “no”. Central bank and government bond rates can turn negative at the “front end” however rates paid to savers are positive. The table below shows bank deposit rates are miserly in Europe and Japan, but not negative. It would be hard to get excited as a saver about 0.10% for 3 years with Japanese banks – and this also explains why Japanese investors are attracted to NZ interest rates. In the table below BNZ term deposits are included to show that our low NZ rates are, on a comparative basis, actually quite high!

What about currency?

There are number of moving parts in economies and financial markets. The ultimate release valve is a floating currency. The Swiss experienced this when in January 2015 they were forced to abandon their floor of 1.20 Francs per Euro. The Franc appreciated 29% in 3 days. Despite negative interest rates, investors continue to be attracted to the safety of investing in Switzerland.

Currency was also an (unexpected) release valve for the negative interest rates in Japan. When negative interest rates were announced on 29 January this year by the Bank of Japan, the currency promptly appreciated by 10% - the exact opposite of what the Bank of Japan had intended. The central bank’s negative interest rate plan failed to deliver.

What other options do central banks have?

Returning Europe and Japan to a growth trajectory has proved to be a massive challenge for policy makers. In terms of monetary policy there are other (equally radical) ideas like the TLTRO program in Europe. The “Targeted Longer-Term Refinancing Operations” program has been relatively low profile – but may prove more effective at driving productive lending by banks. Under the recently announced second TLTRO, banks can borrow money from the central bank for a 4-year term with a rate capped at 0% (and a negative borrowing rate is possible).

This is very cheap funding for banks – effectively a subsidy for bank operations. The purpose is to make cheap funding available for banks that lend to businesses, and so encourage more productive lending. As a subsidy, it is in effect the opposite of negative interest rates (which are a penalty to banks).

Final thoughts?

Under conventional economic theory interest rates across the yield curve should be positive. We are in an unusual world where negative rates are common in the developed world. This is unchartered territory for both central banks and investors. Being untested, these policies will have unintended consequences (for example Japan’s 10% currency appreciation).

Setting negative rates may be an imaginative response to an intractable problem, but it also seems desperate. The risks of unintended consequences and unwanted changes in investor behaviour could well outweigh any possible benefits. Alternatives, such as funding subsidies to banks (i.e. the European Central Bank’s TLTRO program) are controversial but have better understood consequences.

According to Larry Fink (CEO of Blackrock) negative interest rates are “punishing” the world’s savers. With lower returns on offer, savers need to accumulate more capital for their retirement. Are negative rates moving the cost of generating growth from banks to savers?

John Berry, Director

Pathfinder Asset Management Limited

Disclosure of interest: John is a founder of Pathfinder and invests in all Pathfinder’s funds.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « Giving inflation a chance | Competition Takes Many Forms » |

Special Offers

Comments from our readers

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |

It will be interesting to listen to the commentary as various inflation-linked financial products attempt to cope with this.