Infrastructure investing: What, why and how?

According to Blackrock the world needs to build US$57 trillion of new infrastructure by 2030 – a huge amount that governments cannot finance alone. Combine infrastructure demand, financing needs and relatively stable long term returns, and it is easy to understand why interest in infrastructure investment continues to grow.

Monday, July 11th 2016, 8:33AM

by Pathfinder Asset Management

In this commentary John Berry looks at the, what, why and how of infrastructure. This includes thinking about where infrastructure fits in a portfolio and how NZ investors can access these investments.

What is infrastructure?

Infrastructure consists of physical structures together with associated networks and services that connect society and enable its orderly operation. Infrastructure drives a functioning modern economy, covering transport, telecommunications, schools and healthcare, as well as resources like water and energy.

Given the essential nature of infrastructure and the large capital requirements, it has often been the responsibility of governments. However as fiscal budgets have tightened and capital spending needs increased, partial or full privatization of infrastructure will be increasingly common.

Infrastructure is normally categorized as “economic” or “social”. Economic infrastructure provides the structural backbone to the economy including transport (airports, ports, roading etc), telecommunication (transmission networks, cell towers etc) and utilities (water, electricity and gas networks etc). Social infrastructure provides key services vital to the functioning of society (healthcare facilities, education, correctional facilities etc).

Individual infrastructure investments can also be analysed by their stage of development. New infrastructure projects are often referred to as “greenfield” projects. These are at a growth stage and first require designing, financing and building. They can give investors equity-like returns.

More mature or aging infrastructure projects are referred to as “brownfield”. These have already been designed and built but may require rehabilitation. These typically have long term cash flows and can provide investors with stable income-like returns.

Characteristics of infrastructure assets

An infrastructure venture is not like normal businesses. They typically have one or more special features such as:

- Inelastic demand: Infrastructure assets often provide essential services and resources. These are social needs rather than consumer wants or luxuries. With a largely captive customer base, demand can be relatively stable through economic cycles.

- Monopolistic: Large capital requirements and high barriers to entry often mean infrastructure companies face limited competition in their market or geographic region.

- Steady long term cash flows: Infrastructure assets often provide stable and predictable long-term revenue. The assets can be long life – typical life spans (before major maintenance is needed) are 60 years for electricity grids, 50 years for roads and bridges, and 10 years for telecommunication networks.

Infrastructure investment is not without risks. Because of its importance to society and monopolistic nature, infrastructure will often face political attention and regulation. Other risks of managing large plants include construction risk (particularly for greenfield projects) and on-going maintenance risk. Where leverage is high, complicated financial structuring can also bring excessive investment risk.

Portfolio benefits from infrastructure

From an investment perspective infrastructure can behave differently to other assets. Here is what they can deliver in a portfolio context:

Diversification: Infrastructure is often regarded as a separate investment category. The reason for this can be simply illustrated by comparing 5-year daily return data for the S&P Global Infrastructure Index (comprising listed infrastructure assets) to global equities (MSCI World Index), global property (S&P Global Property Index) and global bonds (Bloomberg Global Developed Sovereign Bonds Index). The resulting correlations for infrastructure are 0.13 to bonds, 0.58 to property and 0.65 to equities (note that asset correlations are not static meaning they can change over time). Infrastructure is different. This is consistent with work by Credit Suisse which concluded infrastructure has a low correlation to US equities, global bonds, treasury bonds, commodities and most other investments. A lower correlation allows investors to diversify a portfolio and so reduce risk.

Inflation hedge: Inflation-indexed revenues are common with infrastructure assets. This can be from fixed contractual price increases or monopolistic control of pricing. Deutsche Bank point out that the steady and inflation hedged nature of infrastructure cash flows also mean that infrastructure generally has a low correlation to economic cycles.

Real assets: Infrastructure comprises land and physical structures which are real and tangible assets. Like listed property this can mean less upside in an equity bull market, but also more resilience when equity markets are stressed.

Where does infrastructure sit in a portfolio?

A 2016 survey of close to 100 NZ fund managers, financial adviser groups and asset owners found that 20% intend to increase their global infrastructure holdings in the next year. Interest in infrastructure is increasing yet it can be unclear where to place it in a portfolio. Should it sit with equities, property or something else? Credit Suisse sum this question up nicely, saying infrastructure “can exhibit investment characteristics of private equity, fixed income or real estate. This means that infrastructure investment can technically be placed in several different buckets in a portfolio, depending on the characteristics of the underlying assets and the needs of the investor.”

So which bucket is the right bucket? There is no simple answer. Fisher Funds include infrastructure with property. BlackRock see infrastructure as an “alternative” asset. Others include infrastructure with equities or as a standalone class.

How can infrastructure be accessed?

Infrastructure investment can take the legal form of debt or equity. There are a range of debt securities issued by infrastructure companies traded on NZX. These can be one step above ordinary equity (i.e. capital notes or subordinated debt) to higher up the capital structure (i.e. senior bonds). Issuers include Auckland Airport, Contact, Chorus, Genesis, Infratil and Trustpower.

The focus of this commentary is equity investment rather than debt. Below we consider four different options for equity investment in infrastructure – managed funds, listed funds, direct investment and private funds,

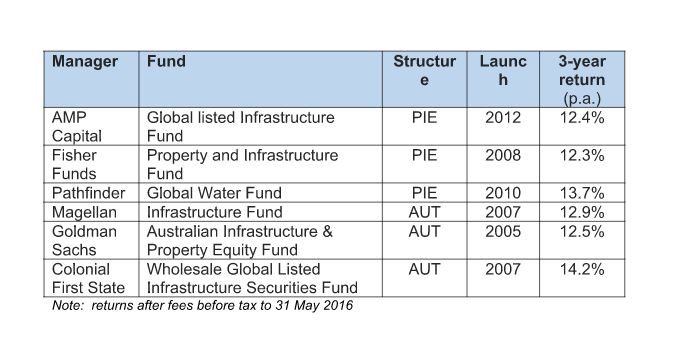

A simple approach for diversified infrastructure investment is through managed funds with retail compliant offer documents. These are typically either PIE funds or Australian Unit Trusts investing in listed securities (meaning high levels of liquidity). Examples include:

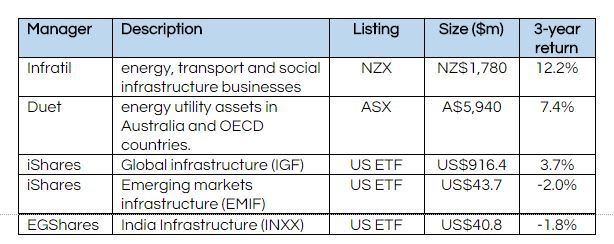

A second option is listed funds. These can be funds investing directly in infrastructure projects or in infrastructure companies. Like managed funds, the listed funds have strong liquidity for investors. This category includes a large number of both broad and specialist infrastructure ETFs listed in the US – we mention three of them below (returns in local currency terms):

A third option is listed infrastructure companies. These generally have a focused business and so will be less diversified than a listed or unlisted fund. In New Zealand examples include Genesis, Mighty River, Ports of Tauranga and Auckland Airport.

A final option is private funds that invest directly in infrastructure assets. These are essentially like private equity funds and will not suit many investors. They differ from managed funds in several ways – (1) they invest directly in infrastructure assets rather than listed infrastructure companies so are less liquid, (2) they are typically for wholesale investors only, (3) they may use a partnership (rather than PIE) structure and (4) investors commit capital and it is then paid up over time as required. In 2010 Morrison & Co launched a fund investing in public infrastructure followed by a second in 2015. Its investments in NZ have included schools and a correction facility, and in Australia include a convention centre, hospital and student accommodation.

Closing thoughts

Infrastructure consists of physical structures and associated services that connect society and enable its orderly operation. It comprises an interesting category for investors as it involves tangible underlying assets that generally provide:

- Long term, stable and predictable cash flows

- Portfolio diversification benefits

- A hedge for inflation

These attributes make infrastructure unique as an investment. It also means that different infrastructure investments can sit at different points in terms of risk and return – they can behave like private equity, listed equity, fixed income, real estate or inflation-linked investments.

For an equity investment in infrastructure there are a range of options – including managed funds, listed funds, listed infrastructure companies and private funds. Over the last decade this sector has grown globally, particularly as investors seek out new income producing options. In NZ we are likely to see this trend accelerate – with growing investor interest and more product choice.

John Berry is a founder of Pathfinder Asset Management Limited and is an independent director of Punakaiki Fund Limited. This commentary is not personalised investment advice - seek investment advice from an Authorised Financial Adviser before making investment decisions.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « Brexit - Near term and longer term views | China recreates the Mississippi Bubble » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |