Investment horizon: The changing face of the New Zealand credit market

Over recent years the New Zealand credit market has been going through something of a quiet revolution.

Tuesday, May 1st 2018, 1:15PM

by Harbour Asset Management

The borderline between bank lending and fund management is becoming blurred. Fund managers are stepping into areas traditionally dominated by banks, as regulatory reform has imposed higher capital costs on banks.

Fund managers are broadening their investment choices and the range of bonds issued has become more varied.

There is also significant innovation via peer-to-peer lending. Greater disclosure is enabling deeper analysis of fixed interest funds. All these trends provide plenty for investors to digest. While the public focus on fees has some merit, a much richer conversation is overdue.

The genesis for change came from both domestic and international sources. The collapse of finance companies in New Zealand through 2008 and the subsequent GFC prompted two key initiatives in New Zealand.

Most significantly, the establishment of the Capital Markets Taskforce led to the establishment of the Financial Markets Authority and the enactment of the Financial Markets Conduct Act, along with other legislation. The Reserve Bank’s role to support financial stability, encompassing bank regulation, has also introduced significant changes.

The big four New Zealand banks are also regulated via their parent companies, by APRA, the Australian bank regulator.

Fund Managers respond

Fund managers have responded by making changes themselves to their fixed income and broader income funds. Their focus has been on meeting investor needs for income and capital security by looking at ways to improve portfolio performance and spreading risk through more diversification. In credit markets, this effectively means looking for ways to find returns from a combination of credit assessment and active management.

In academic finance literature, the role of fixed interest investment has been to provide an offset to the volatility experienced in equity markets. High-quality corporate bonds and government stock have historically performed best when equities have their episodes of sharp weakness. However, many investors do not have a lot of appetite for equities and are more interested in having safe investments that provide better returns than bank term deposits.

To improve returns, higher yielding corporate bonds become an interesting choice. One response from fund managers has been to introduce Income Funds, which aim to produce regular income but may also generate some scope for capital gains over the medium term.

Investment in BB and BBB-rated securities and loans is where the opportunities have changed the most. In markets, this is called the ‘crossover’ ratings sector, which covers the bottom end of the Investment Grade market (securities rated AAA to BBB) and the top end of the High Yield market, where ratings range from BB to C. Standard fixed interest funds, such as the NZ Fixed Interest component of KiwiSaver funds, restrict themselves to investment grade, but there are still interesting choices in this area.

So, what are fund managers doing? For some time, they have been willing to buy NZ-based companies’ debt when issued in foreign currency, fully hedging the currency risk. Examples include Spark issuing in British Pounds, Fonterra in Chinese Renminbi or the major banks in US Dollars.

Fund managers are also dipping their toes into the Australian credit market, copying their equity colleagues who run Australasian equity funds. As this opens a deeper, broader market, choices are more diverse, particularly in the crossover sphere of BBB/BB-rated bonds.

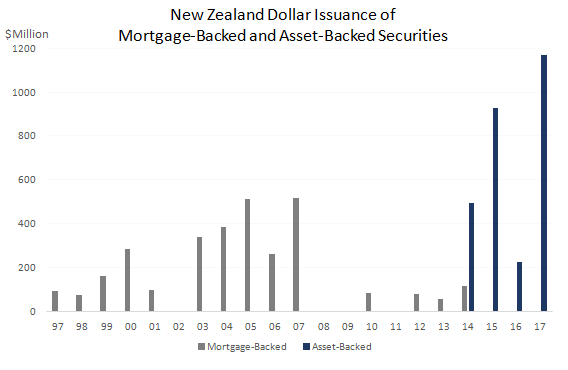

Mortgage-backed and asset-backed markets are rebuilding, having learnt from the GFC

In Australia, mortgage-backed securities(MBS) and asset-backed securities (ABS) are now issued frequently, after a period of little issuance following the GFC. In New Zealand, MBS built a presence until the GFC, but now ABS are making up a greater share of issuance. ABS are pools of consumer loans, ranging from pools of car loans or credit card loans. Also known as securitisations, securities are rated from AAA to BB, with the difference reflecting the seniority each bond has within a pool of mortgages or assets. Reflecting this hierarchy and the relative risk inherent in each tier, yields vary from around 1% above cash rates to 5% or more.

Historically, the issuers of ABS have delivered very stable performance to date.

Source: Bloomberg

Many readers will have seen the film, The Big Short, which describes the very low-quality lending and massive leverage that contributed to the GFC. We need to be vigilant and avoid those types of structures if they ever reappeared in markets.

Our view is that we can be comfortable with MBS and ABS deals when we can do significant due diligence to ensure lending standards are sound, build a strong understanding of the underlying assets, and we like the simplicity and transparency of the structures. At their core, they are highly diversified pools of loans that fund homes, car purchases, credit cards and other financing options that households across the country use and have used for many years.

Bank regulations provide some windows of opportunity for fund managers

Fund managers are also filling a gap left by the banks for funding MBS and ABS deals during the period when a pool of assets is built up. APRA rules now require banks to put capital aside to reflect the risks of securitisation funding, as they do for all their credit exposures. The cost and extent of capital required have meant that banks need to charge the securitisation vehicles a high interest rate to make a decent return on capital.

Pricing has got to the point where banks are often not an efficient lender in this market segment. Now, especially in Australia, fund managers have stepped in, as they do not face the increased capital charges the banks do. This suits fund managers, as they have some pricing power and are willing buyers of the MBS and ABS deals that subsequently get issued.

In New Zealand, the Reserve Bank is also working with the banks to create mortgage-backed securities backed by mortgages granted by those banks. Historically, the domestic banks have preferred to keep the mortgages on their own balance sheets. If banks issued MBS, this would reduce their reliance on funding markets and make them more resilient. This would also change the landscape in the local fixed interest market.

The mortgage-backed asset class, within fixed income, would more closely resemble the United States market, where the MBS sector is very large. At present, conversations between the Reserve Bank and the trading banks are in progress, with discussion focused on the structure and form of MBS deals the banks might issue. It is also conceivable that reduced funding requirements on banks would result in lower term deposit rates. This would have interesting implications across the funds management industry and for the huge proportion of the community that rely on term deposits for secure income.

Investment opportunities are also appearing for vanilla corporate bonds, but where companies are mid-sized, rather than very large. Bond deals of $25 to $75m are being supported by fund managers for companies in the BBB to BB range. Fund managers may buy just small parcels, relative to exposure levels to very large companies such as Transpower or the banks. Diversification and credit research are key. These opportunities are appearing more frequently in Australia but can be expected to expand in New Zealand.

Broader opportunities add scope for active management and require commitment from fund managers

For fund managers, these credit market developments require commitment of time and resources. Some, but not all of these opportunities fit into traditional investment grade fixed interest funds, but they are well suited to the new breed of income funds, where managers are endeavouring to deliver decent returns, but without holding high equity exposures.

It is worth emphasising that traditional investment grade fixed interest funds are not degrading the quality of the portfolio as a result of these changes. Where new developments occur, the opportunity is to deepen diversification and add value from security selection.

For wholesale and retail investors, these changes have led to a broader range of fixed interest and income funds, with a greater range of investment types than before. This adds to the scope to generate additional returns from active management and should lead to a greater dispersion of returns over time.

It is now also easier to investigate the differences across the market, due to the new reporting regime administered by the Financial Markets Authority. This disclosure enables investors to find fund managers and specific funds that more closely meet their investment objectives.

Disclaimer: This article does not constitute advice.

Important disclaimer information

| « Time to get climbing? | Italy: A bigger threat than Brexit? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |