Tariff Wars

A muted global market reaction so far?

Thursday, July 26th 2018, 11:51AM

by Harbour Asset Management

With no further escalation, the implications for New Zealand from the current US-China tariff war are likely to be limited.

Any escalation, however, will have a significant impact on global growth, company earnings, the stock market and the general appetite for risk.

Already, some sectors may be more impacted via supply chain disruption, competitive pricing changes and the economic spill-over effects of higher tariffs on global growth, inflation and interest rates.

In escalation scenarios, the impact is more negative for equity markets generally.

- Growth and inflation estimates modestly affected

- Escalation and a full trade war not priced into equity markets

- New Zealand relatively less impacted

- Best sectors likely to be healthcare, financials and property

The current imposition of tariffs on Chinese goods and the retaliation by China on US goods is likely to have a modest impact on growth and inflation.

Markets have not significantly reacted to this news, despite the directional signal, and the signs that escalation is a distinct possibility. A basket of 50 US stocks with the highest exposure to Chinese revenue has only underperformed by less than 5% since the tariff announcements.

Global equity markets have risen in the past three weeks and Australian resource stocks have been market performers signalling little concern regarding Chinese growth.

This lack of a response to date probably reflects the fact that the tariff news has been swamped by good US company earnings announcements, solid economic data and an easing in Chinese monetary policy.

In addition, there are many moving parts including the policy response and the movement of interest and exchange rates.

We have come along way since 1947 when the average tariff was 22% for all countries combined.

Right now, the average tariff in the US is only 1.7% and in China, it is 3.5% (down sharply from 15% in 2001 as China has embraced the WTO and global trade).

However, markets are increasingly considering the significant scope for an escalation in the tariff war and survey evidence is beginning to point to the potential for businesses to alter their behaviour. Some analysts have estimated the impact of tariffs at a sectoral level and these have interest for global equity investors, however, the growth and inflation impacts set out by for instance UBS analysts is modest.

Of most concern are estimates of the impact on Chinese growth in an escalation scenario. In that regard, the great unknown is the Chinese monetary and fiscal response.

Perhaps in a pre-emptive move in the past week, the Chinese have started to play their hand with three meaningful moves to ease monetary policy and hence lower the Chinese Renminbi.

Macroeconomic shifts also make the near-term impact of tariffs harder to estimate. Unequivocally, however, the steps taken are a poor signal for global growth and the risk for markets has risen.

Some commentators think there is a larger unquantifiable non-economic risk that goes beyond tariffs as non-tariff barriers are also likely to come to bear. For instance, a large Western Australian courier company warned its customers last week that Blackmores products into China were likely to face stepped-up customs procedures.

With trade in services at least twice as large as trade in goods, non-tariff barriers and the reaction of consumers to buy domestic or local products and services is likely to be another risk to global growth.

Economists’ estimates suggest a significant global impact if escalation occurs

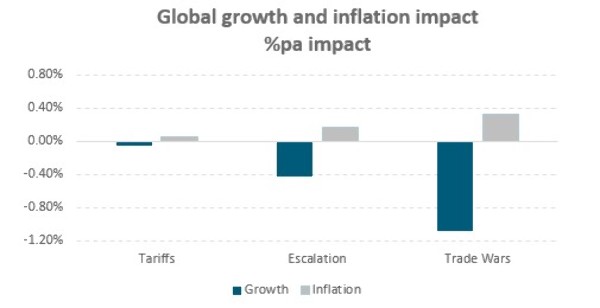

UBS economists estimate that the current first-round effects of announced tariffs would raise global inflation by only 0.05% and could impact global growth by about 0.06%.

That is perhaps why markets haven’t blinked. However, an escalation of tariffs[1] is on the cards and with the potential for almost a 0.4% to be shaved off global growth, and a more meaningful 1% off US growth and 0.6 to 0.7% off Chinese growth.

In that scenario, global inflation could rise by almost 0.2% and have a more significant impact on the current goldilocks scenario.

In that escalation scenario, a fall of 5-10% in global equity markets is estimated with the energy sector most at risk and healthcare and financials expected to be the best relative performing global sectors.

Source: UBS July 2018

UBS have also estimated a full tariff war scenario[2] which would lower global growth by over 1%, and US and Chinese growth by over 2%.

In that extreme scenario, UBS estimate a 20-25% fall in global equity prices, with slippage in the US dollar and oil prices. Harbour thinks that is an extreme scenario and the estimated impact on growth, inflation and markets is in the absence of other policy responses.

One of the interesting facts is that as much as 60% of all Chinese exports to the US come from foreign multi-nationals producing goods in China for the US market. Ironically Chinese exports of computer and electronics, transport and other electrical appliance industries are dominated by global companies with export shares of 60-87%.

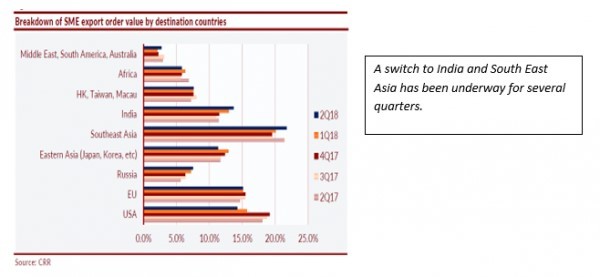

Survey evidence from Chinese companies is beginning to draw conclusions that business leaders are likely to shift their focus.

In China, companies are already changing their orientation from the US, to the fast-growing markets of India and South East Asia. In the second quarter of 2018 US export order values fell from 18% to 14%. This trend, however, has been underway for several quarters and pre-dates the recent tariff talk.

Sectors and stocks with a correlation to global growth, energy, and a supply chain relationship via China into the US, stand to be most impacted in the event of a further escalation.

UBS estimates the energy, materials and information technology sectors would be most negatively impacted, whereas healthcare, consumer durables, banks, property and diversified financials the least impacted.

What to watch for:

- Business confidence in the US has been relatively strong and global growth looks underpinned. Slippage in business confidence and export orders is worth monitoring.

- Aside from Trumps Twitter feed, actual statements from US policymakers, especially the reaction from the White House and Capitol Hill to the proposal to place tariffs on foreign cars.

- The extent of Renminbi depreciation. A further slump in the Chinese currency could push the tariff discussion to the next step.

- Job losses in either China or the US. So far Chinese employment intentions are strong as is US jobs data. A significant slowdown in job creation could point to a larger confidence issue emerging.

Overall: the impact for markets of the current tariffs imposed by the US and China are muted for growth, inflation and equity markets generally.

The NZ equity market is even more removed from the direct and even second round impacts. An escalation, however, would have a more meaningful impact, with a full-blown trade war something to be very concerned about as an equity investor.

Meanwhile, global growth still appears robust as we continue to observe a robust US corporate earnings quarter ahead of the full Australian and New Zealand company earnings announcements.

To conclude, a recent UBS report suggested the New Zealand economy and equity market could be one of the most insulated[3] in the event of a full-blown trade war between China and the US and a tit-for-tat escalation that draws Europe into the fray.

However, there is no question that a further escalation would see few places to hide from increasing uncertainty.

[1] Escalation scenario (Additional US-China tariffs + global car tariffs = 2* (25% * $50bn) + 2*(10%*$200bn) + 25% * $176bn)

[2] Trade war (= Further escalation US China = 25% * $176bn + 30% * $456bn + 30% on $155bn + NTBs to gross China up to US)

[3] “At a country level the best outperformer would be New Zealand, followed by Israel and Finland.” Trade Wars—What is the impact on growth, inflation and financial markets? A Top Down View 11 July 2018

Andrew Bascand, Managing Director & Portfolio Manager at Harbour Asset Management

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « To be or not to be? (A Conglomerate) | The Big Risk: The Creditors' Revolt » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |