The Big Risk: The Creditors' Revolt

“If in doubt, add more credit” seems to have become the global mantra or ‘solve all’ policy recommendation for the last 10 – 20 years. Following the 2008 Global Credit Bust, Bernanke et al simply collapsed interest rates poured excess reserves into their banking systems in the hope that the systems would create more credit.

Thursday, August 2nd 2018, 10:23AM

by Andrew Hunt

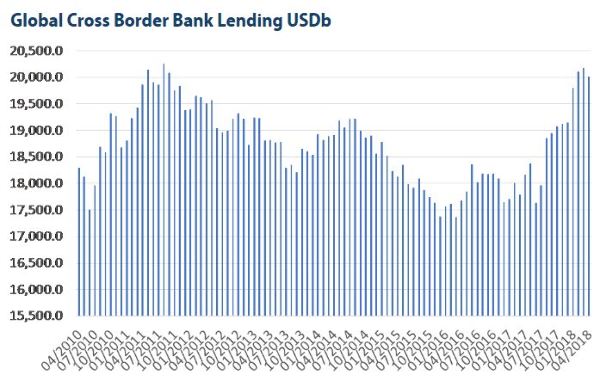

Following the 2008 Global Credit Bust, Bernanke et al simply collapsed interest rates poured excess reserves into their banking systems in the hope that the systems would create more credit. Unfortunately, the ultra-low rates in practice made it very difficult for the banks to grow their earnings in the way that their equity and option stakeholders required, with the result that the banks were obliged to alter their business models; banks in the zero / negative rate economies such as Europe and Japan were obliged either to struggle or to re-invent themselves as international banks, principally by lending dollars (in which interest rates stayed positive) to the emerging markets. Hence, we have witnessed continued slow rates of domestic credit growth in these economies but faster rates of cross-border lending, although truth be told we do not know just how much money has been lent in this way because the speed of financial innovation has overwhelmed the abilities of the statisticians – and more particularly the regulators – to keep up.

Meanwhile, in the USA, the commercial banks have been constrained by the tighter regulatory environment with regard to their conventional lending books and even to an extent with their securities divisions, but they too seem to have been obliged to expand into new areas, principally lending dollars to the aforementioned Euro Zone and Japanese banks. Again, we suspect that the margins have been slim as a result of the Fed’s policy settings but we have a feeling that volumes have been high. In particular, we note how the once ‘boring’ interbank markets have changed from unsecured lending, to repos, to complex derivative structures over the last 10 – 15 years.

International organizations such as the BIS and IMF have attempted to produce some data on this subject but we suspect that, just as in the run up to the GFC, we will not know just how much of this new credit has been created until there is a problem and the system is stress tested in some way (e.g. by defaults or simply a policy tightening).

One feature of the surge in cross border lending that we have become aware of is that the principle ‘agents’ within the processes appear to have changed. Only a few years ago, these types of credit flows were the preserve of large commercial bank treasury departments but more recently they seem to have become dominated by investment banks and even some of the big fund providers. These institutions have long sought market share and volumes - and their marketing efforts are certainly rather more polished and overt in their aims; at the very least their incentive and even ability to consider or let alone disseminate unwelcome news is rather limited. A few years ago, one major ‘treasury department’ made headlines through its activities in a variety of areas but, its operations, though huge, were quite tightly controlled and ‘consistent’. Today it is the investment banking / corporate finance department that has taken over the role of lending dollars to far-flung places and we strongly suspect that its processes are much more decentralized and that as a result layers of risk have been built on top of each other in much the same way that CDOs became CDO squared became …..

The one obvious failure of the post GFC policy regime has been its failure to produce nominal – let alone real – income growth for households. Therefore, in order for governments to achieve – or hope to achieve - the required rates of economic growth, it has been necessary to encourage households to save less whatever the condition of their existing balance sheets or their age and demographic profile. Policymakers from Draghi to Trump have bemoaned the level of saving in Germany because it is bad for growth, but the bottom line is that Germany is a rapidly ageing society that needs to build up reserves for its ‘retirement’. Hence, we have started to see the emergence of a tension between the proponents of the long term and the requirements of the short term…

In an effort to ‘solve’ this savings contradiction, policymakers have sought to raise the value of existing savings by inflating asset prices. For those that already owned assets – and in particular for those that had a high weighting to ‘risk assets’ (including property) - this has provided notional holding gains, although just how many of these will ever be realized is not yet clear. But, for those savers that did not own risk assets to any great extent, such as German savers or UK and Australasian would-be first time buyers, the result of the authorities’ pursuit of ever-higher asset prices has been that formerly prudent savers have been pushed out along the risk curve into often unsuitable vehicles or potential homeowners have been priced out of the markets, with obvious political consequences.

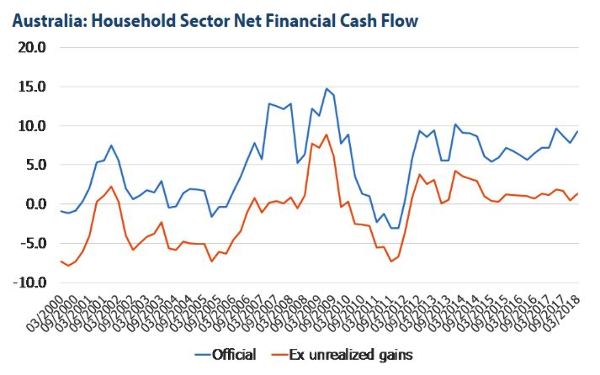

But policymakers cannot relent. We recently completed a study of the Australian economy which, through a mixture of its resource wealth and growing population, has performed relatively well in terms of its income growth over recent years. However, in order to achieve the quite rapid rates of GDP growth that it has experienced, the country has on average added two dollars of debt for every dollar that it has added to GDP. As a result, Australian households now possess debt liabilities that are the equivalent of almost ten years’ worth of their current salaries.

In theory, Australian households currently possess around AUD10 trillion of net worth but this number has been arrived at through a near doubling of the recorded value of the residential housing stock since the GFC (the housing stock is currently valued at the equivalent of five and a half times annual disposable incomes) and a 125% increase in the reported but unrealized holding gains on pension vehicles. On one side of the household sector’s balance sheet is a great deal of debt, on the other is a great deal of assets, the value of which can change rapidly.

Interestingly, we find that the government statisticians report that, despite this massive borrowing, households have remained cash flow positive over recent years but we believe that this is because they impute cash flow from unrealized holding gains. If we attempt a crude ‘hard dollar’ calculation to look at the actual flow of ‘real money, we find a very different picture….

We would be the first to admit that our estimate of household cash flow excluding imputed unrealized gains is unlikely to be exactly correct but we suspect that it is not too far wide of the mark and it serves to illustrate just how dependent households have become on high and rising asset prices to support their balance sheets and to make their positions viable. As a result, policymakers in Australia – as elsewhere – have a vested interest in inflating or at least maintaining high asset prices despite the social costs that we alluded to above. Despite the lessons of the GFC the world has, it seems, become more rather than less dependent on credit and asset prices – what the Japanese used to refer to as zaitech (financial engineering) during their bubble economy period a generation ago.

To the branch office of some investment bank that is operating within the confines of a particular country, there may seem to be no limit to how much credit can be advanced – as long as head office sends the money the credit cycle can be sustained. A few Cassandras may worry about credit quality and the potential for bad loans but in reality there tends to be few bad loan experiences during a credit boom, not least because those without income can always just keep borrowing…

However, and despite what Bernanke, Kuroda and Draghi may have wished us to believe, the supply of credit is not in fact infinite. Credit represents an asset of the financial system and where there is an asset, there must also be a liability.

In the case of the cross border largely dollar denominated credit flows that have implicitly funded growth not just in the EM but even Australasian and some of French credit growth over recent years, the ultimate ‘funding liability’ is thought to be the now huge stock of excess reserves that are owned by US banks and notionally held at the Federal Reserve. In effect, these reserves now provide the lubricating ‘settlement cash’ for the web of intra financial system loans that underpin the global credit system. However, as the Federal Reserve has begun to tighten in response to the US’s overheated economy, it has been obliged to pay interest to the banks on these reserve deposits. This is not something that has mattered during previous cycles because the level of reserves was quite small but in the post QE world, we estimate that it will soon be costing the US public sector $100 billion or more per annum to pay this interest bill.

This news has not gone down well with the ever ‘populist’ Trump Administration (since it appears that banks get given money when times are bad, and still given money when times are good…) and the revelation that roughly 40% of excess reserves in the US system are owned by the US branch offices of foreign banks has only served to create yet more political problems for the Fed. We doubt that without the ‘social implications’ of the Fed’s policies Trump would have been elected but one of the consequences of his election is that his Administration is now encouraging the Federal Reserve to shrink its balance sheet at a faster pace so as to save on the interest expenses, a move that will leave the dollar credit system ‘short’ of cash and therefore less able to fund credit growth, particularly outside the USA.

For those EM and Australasian banking systems that are dependent on their ability to source dollar funding (because of their stretched domestic loan to deposit ratios), this is potentially very big news indeed. If the Administration / Federal Reserve does indeed reduce the level of excess reserves in the US by the 75% or so that they are suggesting, then credit will likely become a lot more expensive and a lot less available in many of these economies. At this point, their post GFC models will be obliged to change quite fundamentally.

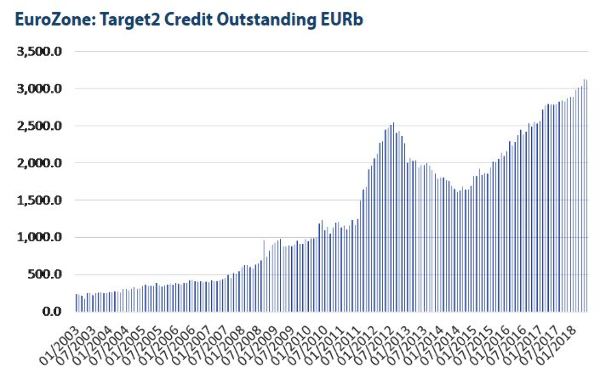

In Europe, the governments may like to hide the fact but the reality of the situation is that the Euro Zone’s very existence is only made possible by the immense (EUR3 trillion) TARGET2 credit system. TARGET2 is perhaps the ultimate shadow bank, it has almost invisibly provided hundreds of billions of Euros to the debtor countries in the EZ (France, Spain, Italy, Portugal etc) at zero interest rates. Without TARGET2, interest rates and yields in these economies would have to be very much higher and the countries would, as a result, probably have been obliged to leave the currency union. The problem for TARGET2 is however that there are only really two creditors remaining within the system. In fact, Germany and the Netherlands are now responsible for providing three quarters of the funding for all of the debtors in the system.

As a result of the ECB’s pro-debtor / anti creditor stance, these creditor nations are obliged to lend to TARGET2 at minus 40 basis points, a situation that implies that a great deal of the savings in these ageing economies actually “cost savers” a negative carry to own. Moreover, with a large chunk of their savings compelled to earn negative rates, it has become necessary for asset allocators to ‘take bigger risks’ with the remainder of the ‘portfolio’ but this has led to a series of disastrous capital losses (i.e. the role of the German banks in the US Mortgage Markets in 2006-7). All of this has led to some very ‘unhappy’ savers in Germany (and to an extent in the Netherlands as well) who feel that they are sacrificing their own future living standards (particularly their retirements) for the sake of spend thrift foreigners and ‘new arrivals’. No wonder Merkel’s pro EU coalition is in trouble and the more extreme xenophobic parties have become political forces.

However, if Merkel’s coalition fails, we suspect that whatever else occurs, Germany will be a lot less prepared to lend money to TARGET2 at negative interest rates (and the more extreme parts of the German financial system seem to be suggesting that it simply shouldn’t lend at all…). If Merkel’s faction falls from power, funding the intra Euro Zone TARGET2 credit boom may become a lot harder and the Euro will face a very different form of existential crisis to its usual debtor / credit risk types of events.

There is a view in markets that problems such as these could not possibly occur in China, where the authorities are presumed to be both omnipotent and unconstrained in their actions. In fact, much of China’s growth last year was once again reliant on credit (total credit growth in 2017 was more than USD3 trillion) and no small part of this was only made possible by the Chinese banks’ heavy use of foreign (dollar) funding. Indeed, since the latter has become rather less available, we find that China’s rate of credit growth has already slowed very sharply to the point at which we estimate that there is now insufficient credit growth to fund the private sector’s ongoing cash flow deficit.

Hence, China’s companies have been forced into a period of intense austerity and we estimate, on the basis of the bottom up data, that industrial output has shrunk by 4% over the last year, with the majority of the decline having occurred over recent months. China’s economy is already close to a recession.

Clearly, given the recent surge in corporate finance / lending by the investment banks in the EM world that we described earlier, many institutions have specific business reasons why they might not wish to investigate the current situation too closely (just as it was improper in 1999 to look too closely in the mouths of the Tech Bubble horses in case one incurred the wrath of the immensely profitable corporate finance departments; or to look at the US MBS markets in 2007 in case of offending the money-printing trading desks...) but the hard data is nonetheless quite unequivocal. Moreover, those that do risk acknowledging the data then usually express the view that China is different and that, just as was the case in 2016, the government can simply throw more credit at the economy.

In 2016, the PBoC provided more than $1.2 trillion of funding to China’s banks so that they could extend close to $4 trillion of new credit in the economy and the fiscal impulse from the government may have been as much as the equivalent of 6 – 8% of GDP. Given these events, it was not surprising that the economy enjoyed a strong 18 months from mid-2016 onwards and this certainly benefited the global economy immensely via its impact on global trade.

Given the 2016 precedent, many are asking why China simply cannot do the same again on this occasion. However, the problem is once again one of funding. China’s savers already own three or four times as much money in their overall portfolios, and relative to GDP as almost any other country in the world (hence China’s real economy accounts for around 13-15% of Global GDP but China accounts for a third of the global money supply, a glaring disparity…) Generations of financial repression have resulted in China’s savers by definition experiencing only a very narrow list of available stores of value that they can acquire – the local equity market is small, the bond market difficult to access, gold imports are limited by law, foreign assets are illegal to acquire because of capital controls and crypto currencies are banned. As a result, savers have a choice between bank deposits that offer negative real yields or property assets, and they have already shown that they are uncomfortable with this situation – hence their ongoing keen appetite for local properties and Western “labelled” consumer goods that offer a utility as a store of value as well as a consumption good.

It is our view that if China’s government were to borrow an extra $1 trillion and at the same time double the rate of private sector credit growth, then China’s economy could be provided with a recession-avoiding nominal boost. However, the problem for China would be that if it created another $4 trillion of credit, it would have to create another $4 trillion of deposits and wealth management products within a system that is already intensely satiated with such products. In fact, if the authorities allowed the creation of so many domestic money balances, we fear that they would be dumped into the local property markets (which would inflate the cost of living and so raise inflation); spent in favour of goods (a stimulatory but potentially inflationary outcome), and/or spirited abroad through whatever circuitous routes might be available but most obviously through the banking system. The resulting capital outflows would likely accelerate the rate of depreciation of the RMB, an event that would also be inflationary for prices and also ‘dangerous’ for relations with the USA. Even China’s authorities may be facing a binding funding constraint on their ability to act that is not in character unlike that faced by the West during the 1970s.

Of these three ‘primary threats’ to this latest instalment of the global credit boom, we believe that at present China is the most immediate but, as European politicians return from the summer recess, we fully expect that EZ stresses are likely to reappear from September onwards. Finally, from October onwards, we can expect both more bond issuance from the US Treasury and more pressure on the FOMC to shrink its balance sheet at a faster pace, both of which may serve to worsen the ‘global dollar shortage’. Given these threats, which are in a sense of a type and nature that the world has not faced for a long time (the last savers’ revolt was probably in the late 1970s..), we do wonder if the closing months of 2018 may be quite volatile for risk markets as we find that the end of the road that the proverbial can has consistently been kicked down starts to come more sharply into view.

Andrew Hunt International Economist London

| « Corporate Values, worth the effort? | Investing: Understanding non-financial risks » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |