What contribution rate should I have in order to retire?

More specific guidance is needed from advisers if clients are to have the income they require in retirement.

Thursday, December 13th 2018, 10:41AM

by Paul van Wetering

Paul van Wetering

Let us cut to the chase, KiwiSaver was formed to ensure New Zealanders could self-provision for retirement.

Its predecessor, NZ Super, which relies on tax payers funding the generation ahead of them, is failing.

One need only reference the Westpac-Massey-Ed Centre’s annual Expenditure Guidelines study to see NZ Super’s current “inflation adjusted” payment level does not meet a “no-frills” lifestyle, or The Treasury’s projection that 27% of the population will be 65+ in 2060, up from 15% today.

Only 58% of the population is expected to be between 15 – 64 meaning every retiree will be supported by just two working age people. Today there are 4.3 working age people per each retiree (1).

About the only people not to acknowledge it are the politicians.

Financial advisers, unfortunately live in the real world and must face reality on almost a daily basis.

It is therefore amazing that after nine years, and $55 billion of savings in, the most basic question: “What contribution rate should I have in order to retire?” is too often met with a blank stare, or worse, a swift change of subject to which of the 252 funds (2) on offer is superior to the others based on a nuanced and technical difference in returns, fees, service, active, passive, or all of the above; the industry’s smoke-screen for, “I’ve no idea”.

Another industry favorite is “well, it depends” which is, as we will see, kind of true, but equally unhelpful when helping an individual select their contribution rate.

The current statutory minimum for an employee is 3%.

At this level they are able to take advantage of their employer’s matching contribution of 3% less tax, for a contribution rate (as a percentage of pre-tax salary) of 6% less tax so let us say 5%.

But while everyone acknowledges that this is too little to fund your retirement, there has been little effort to either raise the contribution rate to a safer minimum or bridge the financial literacy gap that exists.

A good starting point is the savings rates settled on by regulators in more financially sophisticated jurisdictions.

In the United States, where 401K plans were introduced in 1978, the average employee saves 7% of their income.

In the United Kingdom, where pensions which have been a feature of workplace benefits for over 100 years went compulsory in 2012, it is 8% minimum from 2019.

Australia, who bit the bullet in 1992 (an opportunity the Todd Task Force of 1992 bungled for New Zealanders), the savings rate is 9.5%, increasing to 12% by 2025.

These numbers all fall within a similar band, and are all higher than those in New Zealand.

Here is why. The starting point for everyone is their current standard of living. If one properly provisions for retirement, then the average retiring individual (or couple) should not suffer a sharp fall (or expect a significant rise) in living standards. Based on data from NZ Funds’ financial planning software, the average New Zealander wishes to retire on 61% of their current income.

Implicit in this is their retirement is topped up by NZ Super; that work-related expenses, transport, clothing etc. are replaced by leisure activities; and that children, mortgage and savings activities cease.

We have, over the last 30 years, found this a bit light and round it up to 70%.

In this way, planning to retire on 70% of your working salary broadly equates to retiring on 100% of your disposable income.

This ratio combined with the expected level of NZ Super and life expectancy determine how much an individual needs to accumulate to fund their retirement.

It is then a simple matter of selecting the right savings rates. Whether all of this savings is channeled into KiwiSaver, or spread between KiwiSaver and Superannuation Schemes (which can be accessed from 55 years of age instead of 65 years of age), is an interesting topic in itself.

The most problematic issue, the mortgage and family home, is often the most simple.

As with standard of living in retirement, most families end up owning homes which are broadly in line with their level of earning.

We estimate using our database that a family in Auckland earning $100,000 per annum would on average own a $600,000 home, while a family earning $200,000 per annum owns a $1,000,000 home. So while the dollar sums will differ on a case-by-case basis, the relative to income percentages do not.

Similarly, most families will end up paying off their mortgages before retiring, on average at age 64.

Whether a family wishes to “release” some or all of the equity they build up in their family home in order to fund their retirement is the single biggest determinate of their savings rate.

For families who do not wish to use their home in retirement, this gives them a backstop, should one or both live longer than expected, or an inheritance to leave the next generation.

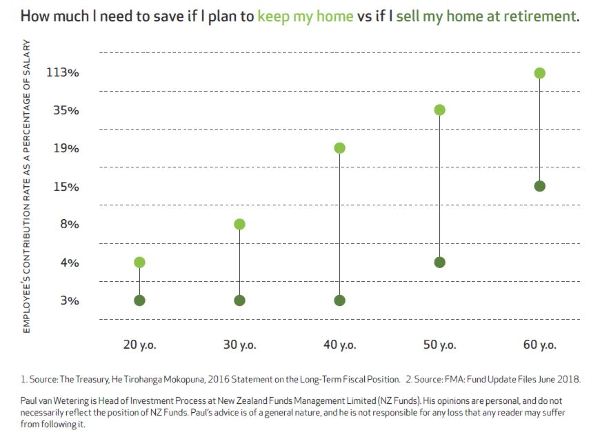

In this case, the savings ratios rise with age (as shown below). For families who wish to use some or all of their home equity to fund retirement, the retirement savings ratios are lower.

Interestingly, if you plan on using all the equity in your home in retirement, then the minimum KiwiSaver employee contribution rate is appropriate for you until the age of 50.

For everyone else who enjoys living in their home, not having to worry about living a little longer, and being able to leave something for the next generation or a cause of their choice, there is a need for them to increase their contribution rate.

As many New Zealanders do not realise this, it represents a once in a lifetime opportunity for financial advisers to make a significant contribution to their clients’ future prosperity and peace of mind.

| « 30 Years in business | Govt moves to allow early KiwiSaver withdrawal » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |