Antipodes offers investor choice

Manager focuses on capital preservation, identifying opportunities.

Monday, December 31st 2018, 2:40PM

ASSET: Can you explain your investment style?

Antipodes is a global asset manager offering a pragmatic value approach across long and long-short strategies. We aspire to grow client wealth over the long-term by generating absolute returns in excess of the benchmark at below market levels of risk.

At Antipodes, we believe that investment returns are primarily a function of economic performance of the business you own and the durability of this performance, that is, business resilience; and price paid or starting valuation.

Though usually efficient, markets can become selectively irrational around the continuum of change in a business’s operating environment, creating a pragmatic value opportunity to allocate capital to resilient businesses at favourable terms.

However, we also believe that long-term investment success is deeply entwined with a systematic approach to assessing returns relative to risk. We actively embrace controllable risks that offer attractive return payoffs and seek to diversify the impact of uncertainty.

In summary, we seek to take advantage of the market’s tendency for irrational extrapolation, identify investments that offer a high margin of safety and build portfolios with a capital preservation focus.

ASSET: Capital preservation is key to Antipodes. How do you achieve this?

At its core, we believe that if you manage risk well, returns will follow.

We distinguish between “controllable” and “uncontrollable” risk as different components of aggregate “investment risk”, i.e. the risk of permanent loss of capital and unforeseen downside volatility. We actively embrace controllable risks that offer attractive return payoffs and seek to diversify the impact of uncertainty.

Controllable risks can be managed at the stock level by ensuring our investments have attractive starting valuations, or margin of safety, and business resilience - as characterised by having multiple ways of winning – to offer downside protection to the extent our judgement an any stock-specific risk is misplaced. More broadly, we also consider our investments in the context of their exposures to socio-macroeconomic risks.

To diversify the impact of uncertainty, or uncontrollable risks, we aim to construct our portfolio with non-correlated clusters of opportunity. This means looking beyond regional and sector diversification to a deeper examination of the similarities between our holdings on the basis of their end-markets, irrational extrapolation and socio-macroeconomic sensitivity.

ASSET: Can you explain your approach to active currency positioning?

Most managers decide to either hedge their currency exposures back to a home currency or leave their currency exposures unhedged. At Antipodes, we do neither, instead choosing to assess the degree to which an underlying currency exposure which arises from stock selection is desired, and if not, hedge into an undervalued currency. Our assessment would include identification of significant valuation anomalies, sovereign risk assessment and a real-world reality check considering export competitiveness and relative cost of living.

The approach to examining currencies is no different to that of assessing our equity investments, i.e. we seek both a margin of safety (or lack of in the case of shorts) and multiple ways of winning (or losing in the case of shorts). Given the greater level of uncertainty that arises from currency selection, a higher margin of safety is required.

Given currency exposure is taken by virtue of our stock selection, we believe this approach delivers better outcomes for our clients.

ASSET: How does Antipodes differ from other managers?

We distinguish ourselves from other managers in three ways.

Firstly, our organisational structure and research process is designed to be scalable and align our analysts interests with those of the clients.

Secondly, Antipodes employs a quantamental approach to idea generation and risk management, i.e. an integrated approach of both fundamental and quantitative science. This has the effect of enhancing the research process and we believe achieving better outcomes for our clients.

Finally, we place a tremendous amount of effort in portfolio construction, i.e. emphasising risk adjusted returns at the portfolio by actively embrace controllable risks that offer attractive return payoffs and seek to diversify the impact of uncertainty.

ASSET: Why have you decided to launch PIE versions of your funds at this point in time?

First and foremost, its about providing New Zealand investors with choice. Following many discussions with our New Zealand based clients and in line with our ongoing commitment to this market it made perfect sense to offer access to our funds via a Portfolio Investment Entity (PIE) which is designed specifically for the local market and is administratively simple for investors.

Given the nature of our partnership with Pinnacle we are able to create new vehicles, such as PIEs, that act as access points for the same three underlying investment strategies that we’ve had since inception – Global Long-Short, Global Long and Asia Long-Short. This allows us to connect with investors wishing to access of our strategies through local vehicles while allowing the Antipodes investment team to focus on delivering investment outcomes for our clients.

ASSET: Value investing has struggled recently, when do you think it will really pay off again?

In the US, against a backdrop of relatively subdued inflation, growth is soaring, with Trump’s domestic policy analogous to burning all the furniture in the room. Whilst some indicators, such as the corporate profit cycle, industrial production, unemployment and consumer confidence suggest the economic cycle is maturing, residential/corporate investment and wage inflation is still at early or mid-cycle levels. The risk to the cycle is monetary policy, with an increasingly limited fiscal backstop.

Following the GFC, as policy rates neared zero, the Federal Reserve (Fed) actively targeted a flatter yield curve, rebalancing portfolios towards risk and duration, with the wealth effects of asset price inflation a key transmission mechanism to the real economy. The expansion of the Fed’s balance sheet flooded the US banking system with reserves such that to maintain control over the target rate of interest, the Fed began paying interest on excess reserves. Today, the US banking system is incentivised to hold excess capital, risk free, at 2.2% p.a.

The Fed’s path to normalisation is as much about allowing the market forces to dictate the shape of the yield curve as it is about managing the target rate in-line with inflation. Allowing the balance sheet to shrink - QT - is the strategy to achieve this, though the risk is that at some point we transition from a banking system with excess reserves, to one where reserves become scarce.

The Fed’s intention is to allow its balance sheet to run-off at a rate of $50b a month into the foreseeable future. As the balance sheet contracts and reserves are destroyed, the banking system will be required to compete for liquidity, signalling a return of Open Market Operations to manage the target rate. The point at which this occurs, and the Fed reaction function is a matter of substantial debate.

The requirement for reserves in the US banking system is now structurally higher – a consequence of post crisis regulatory changes to the banking system requiring banks to maintain an adequate stock of unencumbered high quality liquid assets – meaning the Fed may not be able to safely reduce their balance sheet by much without provoking strains within the system, and with it, heightened volatility across all asset classes. Should this materialise sooner than expected, and the Fed struggles to navigate the liquidity driven turbulence that may arise as consequence, the ability of the Fed (and other central banks) to pursue QT to its end may be in doubt, and with it a return to the flatter yield curve targeting regime of the past decade. Within equities, this will likely favour the status quo i.e. a stylistic preference for “structural growth” or “quality” at any price.

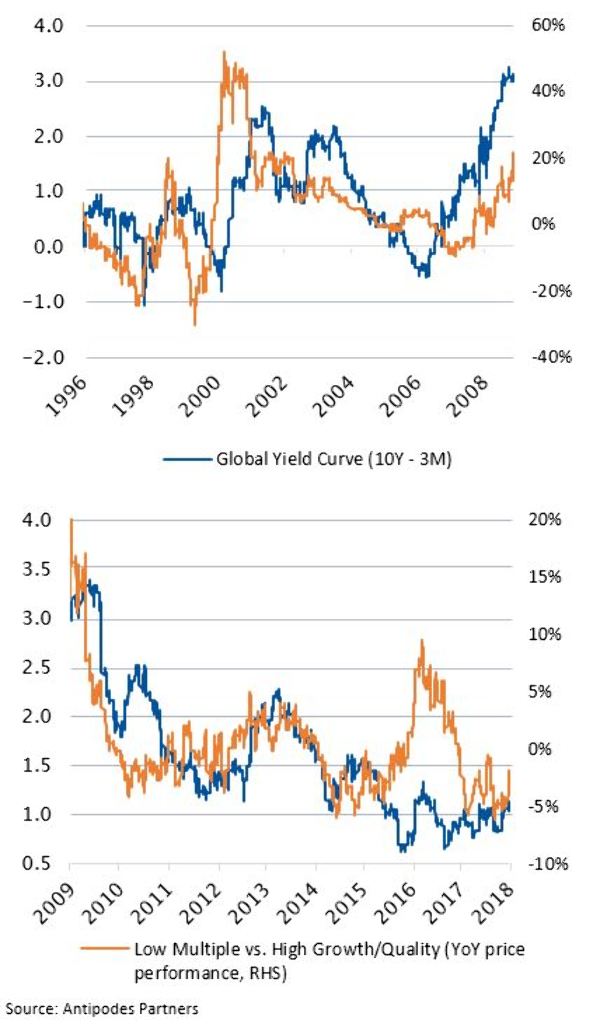

Figure 6: catalyst for a rotation into lower multiple stocks? (1995-2018)

However, a successful (even if turbulent) implementation of QT, in conjunction with reduced bond buying by other central banks, is likely to steepen the US yield curve as the influence of central banks wane, the rate hike cycle matures and the Fed risks clamping down on growth. Whilst the market has typically imputed weaker growth as meaning further balance sheet expansion and yield curve compression, a sustained and gradual Fed run-off is likely to alter this dynamic, with the natural lever of the Fed to reduce policy rates before scaling back on QT at the risk of damaging its credibility. Simplistically, with US nominal growth running at ~6% and ten year nominal yields at ~3%, long rates can be rationalised higher. The historical relationship suggests that in this environment, a stylist preference for low multiple stocks could evolve.

Until the process of QT becomes more entrenched, the more immediate implication of the Fed enduring with its commitment to tightening is a flatter, potentially negative US yield curve, and without a rebound in European growth and/or a reversal of Chinese regulatory tightening, the risk of a Fed policy mistake is very real. This risk may exacerbated by the inflationary nature of Trump’s tax cuts and trade policy (though somewhat offset by a stronger dollar), accelerating the need to tighten. Given a capital market structure that has changed profoundly post GFC, with central banks and passive liquidity acting as shock absorbers to risk assets more broadly, the progression of QT is likely to trigger increasing volatility across all asset classes. Longer term, we’d expect a successful implementation of QT to reverse the distortions of the low rate and flatter yield curve environment that has characterised the prior decade.

Antipodes Partners’ investment goal is to build portfolios with a capital preservation focus from non-correlated clusters of opportunity. In our long investments we seek both attractively priced businesses (margin of safety) and investment resilience (characterised by multiple ways of winning), with the opposite logic applying to our shorts, i.e. no margin of safety and multiple ways of losing.

Whilst the investment case will always be predicated on idiosyncratic stock factors such as competitive dynamics, product cycles, management and regulatory outcomes, we seek to amplify the investment case by taking advantage of style biases and macroeconomic risks/opportunities.

Given the divergent risks of US monetary tightening, the Fed reaction function and the global growth outlook, investors should focus more than ever on uncovering sources of idiosyncratic alpha rather than relying on momentum or passive beta. In this sense, we’re encouraged by the high level of valuation dispersion within and across markets as indicative of broad pragmatic value opportunities, both long and short.

| « Top 10 Dow Jones Industrial Average Factoids – 2018 in Review | What can the past two years tell us about markets in 2019 » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |