Harbour Outlook: Economic Crosscurrents

Tuesday, November 14th 2023, 10:27AM

by Harbour Asset Management

- The MSCI All Country World Index (ACWI) continued its decline, posting a -2.7% loss in New Zealand dollar-hedged terms (and a 0.2% gain in unhedged NZD terms). Despite three consecutive months of negative returns, the 12-month return figure for the index stands at 9.5% in NZD-hedged terms and 10.4% in unhedged terms.

- Returns for the month were similarly weak in local markets, with the S&P/NZX 50 Gross Index (with imputation credits) falling -4.8%, and the S&P/ASX 200 Index falling -3.8% (-2.4% in New Zealand dollar terms).

- Bond indices were also negative over the month. The Bloomberg NZ Bond Composite 0+ Yr Index fell -0.2%, whilst the Bloomberg Global Aggregate Bond Index (hedged to NZD) also dropped -0.7% over the month. This came as the US market saw 10-year government yields increase to 4.9%, a level not seen since 2007, with resilience in US economic data prompting the market to largely unwind an expectation that the Federal Reserve would be cutting rates in 2024.

Key developments

New Zealand and Australian share market returns and valuations continued to be impacted negatively by further sharp increases in long-term government bond yields (New Zealand 10-year Government bond yields up to 5.6% and Australian up to 4.9%) over the month. Military action in the Middle East drove a flight to safe assets as investors feared the potential for a broadening conflict, with capital moving out of riskier investments including smaller capitalisation and pre-profitability shares. The combination of higher interest rates and geopolitics triggered wide deleveraging by hedge funds and systematic funds which added to weakness in the wider share market. During the month the annual general meeting (AGM) and quarterly update season disappointed against market expectations, contributing to further reductions in earnings forecasts.

The US economy continues to show surprising resilience, growing almost 5% in Q3 on an annualised basis. Strength is concentrated in services, rather than manufacturing. Household consumption is being supported by an ongoing reduction in household savings and 30-year mortgages providing a degree of insulation from the impact of higher interest rates. With US house prices rising in recent months, after only modest declines in H2 2022, and global equities still 4% higher YTD, household balance sheets aren't providing much impetus to reduce consumption. US Federal Reserve Chair Powell noted recently that recent strength in domestic demand may require further tightening if it slows progress on lowering inflation and loosening the labour market.

Economic performance in the rest of the world lags the US considerably. Chinese economic growth appears to be stabilising at low levels, growing 1.3% in Q3. A pickup in official PMIs in September suggests the worst may be over for the Chinese economy, but structural challenges remain when it comes to consumption and the property sector. Recent indicators suggest the euro area economy may avoid recession this year, but growth is still likely to be anaemic. As such, markets assume the European Central Bank has finished its tightening cycle.

Monetary policy is working in New Zealand and the Reserve Bank of New Zealand (RBNZ) seems happy to be on hold at 5.5%. Annual core inflation dropped from 5.7% to 5.2% in Q3. Business surveys suggest the labour market has loosened considerably, likely helped by the recent high rates of migration. Firms are no longer struggling to find labour and are instead being constrained by a lack of demand. A net 17% of firms reported lower activity in Q3 which is consistent with no GDP growth in the coming quarters. At its October Monetary Policy Review, the RBNZ noted that tight policy is working "as required" with the near-term risk that activity and inflation don't slow as much as needed offset by the medium-term risk of a greater slowdown in global demand.

What to watch

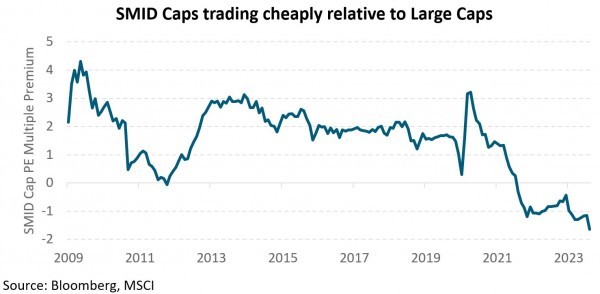

Much has been made of the rise of the “magnificent seven” comprised of Apple, Amazon, Alphabet, Meta, Tesla, NVIDIA and Microsoft. At the end of October these stocks have contributed 85% of the calendar year-to-date MSCI All Country World Index return and are 17% of the market cap. The equal-weighted MSCI All Country World Index is down 3% so far this year, pointing to the average stock falling. These factors have contributed to a large gap opening between large caps and small- and mid-cap stocks. While it might be too early to call a turnaround, as small and mid-cap stocks tend to be more interest rate and economically sensitive, the valuation story looks compelling both in absolute (13x forward earnings) and relative terms for long-term investors.

Market outlook and positioning

The move up in long-term bond yields has contributed to a pullback in share market valuation multiples. The unwind of COVID ultralow interest rates may have some residual impact for capital markets but valuations and earnings expectations are now more in line with long run ‘normal ranges’. The US has exported higher long-term bond yields to global capital markets. A higher cost of capital hurdle has impacted equity market valuations everywhere. The sharp increase in US long-term interest rates, driven by higher real rates, reflects a range of factors including upside growth surprise in the US economy, a narrative shift to 'higher for longer', and US Federal Government fiscal position/funding requirements. The persistent pressure of climbing yields has weighed heavily on equity markets, with all major indices in correction territory. Capital markets are moving from considering how high interest rates need to go to how long interest rates need to stay in restrictive territory to offset sticky inflation. With share markets now allowing for interest rates staying restrictive for longer, a pause in central bank official interest rate increases, even if the pause includes 'hawkish' conservative framing, may see a positive response from share markets.

Economic crosscurrents, with both inflation and economic growth slowing, creates a mixed backdrop for earnings in the near term. Economic activity by region remains desynchronised – the US has been strong, the Chinese economy has been weak, but is showing signs of stabilising, Europe has been weak, and New Zealand and Australia have been slowing. The US economy has been supported by Federal Government policy favouring increased renewable energy generation and onshoring/reshoring of manufacturing and production. But after a very strong third quarter, US lead indicators, including the Institute of Supply Management (ISM) manufacturing new orders index, have slipped into contraction territory, consistent with weakness in world industrial production. Given the tightness in financial conditions, there is potential for leading indicators to continue to slow.

Across New Zealand and Australia these crosscurrents are having some significant impacts for companies and sectors. Fading consumer confidence is being offset by higher migration, contributing to falling consumption per head of population. Public sector investment and works remain elevated, supporting activity but crowding out private sector activity. Business confidence is mixed. The latest Financial Stability Report from the RBNZ highlights that the five major NZ banks see risk that non-performing loans will rise to around 1% by early-2025 – more than double current levels. The risk that tightness in financial conditions causes something to crack or break means we remain wary about more cyclical exposures. We remain watchful for earnings downgrades as negative operating leverage and normalisation/reversal of pricing power emerges as the last inefficiencies of COVID stimulus rolls out of the economic system.

Within equity growth portfolios our strategy remains to position for a range of scenarios and to be selective. We continue to favour investments with structural tailwinds that are less dependent on strong economic activity. We continue to see technology disruption, de-carbonisation, and demographic changes as supporting company earnings. Two trends stand out as potential sources of near-term positive earnings risk - demographics, particularly positive migration, and generative artificial intelligence. Businesses exposed to the energy transition and the onshoring/nearshoring of manufacturing and storage of goods may face opportunities and threats. We are also favouring businesses with productivity and efficiency ‘self-help’ programmes, particularly where business reengineering introduces technology that improves both revenue and cost structures. We continue to have a bias to quality, well-capitalised businesses that are less vulnerable to a tightening in financial conditions.

Within fixed interest portfolios we retain a long duration position, meaning portfolios will benefit from a fall in interest rates. Our investment strategy is driven by the view that the OCR is likely to shift downwards in 2024. Recent data showing less pressure in the jobs market and a decline in core inflation are encouraging. Our yield curve positioning for this view is within the 1- to 5-year maturity range. With long-dated securities, we are more neutral, as we expect the US Federal Reserve to stay on hold for some time, or possibly hike rates. The issuance program for NZ Government Stock over the first half of 2024 will also be large and may hinder scope for yields to decline. We retain a holding of inflation-indexed bonds, which continue to offer a high effective yield as well as protection in the event that core inflation remains sticky. We have also lifted credit exposure, as new issues have come to market at attractive pricing.

The Active Growth Fund is defensively positioned, being overweight bonds and underweight equities. Equity yields relative to bonds, as measured by the equity risk premium, are at multi-decade lows (meaning equities look overvalued relative to bonds). We have a keen eye on our earnings models as one way to justify higher valuations is earnings growth. However, our forward-looking earnings models are showing significantly lower earnings than the market consensus (we have started to see downgrades to 2024 earnings this earnings season), which leads us to maintain our underweight to equity markets. We continue to dedicate a lot of research time to some of the extremes that exist under the surface in equity markets, which have become apparent due to the returns of many indices being driven by a very small subset of companies (i.e. the "Magnificent Seven" of Apple, Amazon, Alphabet, Meta, Tesla, NVIDIA and Microsoft).

The Income Fund’s strategy continues to favour fixed interest allocations. The current global macroeconomic outlook for soft growth and declining inflation is typically very favourable for bonds. Our expectation that the Reserve Bank will cut the OCR in 2024 is also supporting a long duration position for the fixed interest securities. This also reflects the strategy in place for our fixed interest portfolios. Weakness in equity markets has been notable over recent weeks and we have raised the equity allocation, which had been as low as 26% to 28.5%, buying a blend of growth styles and income-generating Australasian stocks.

IMPORTANT NOTICE AND DISCLAIMER

This publication is provided for general information purposes only. The information provided is not intended to be financial advice. The information provided is given in good faith and has been prepared from sources believed to be accurate and complete as at the date of issue, but such information may be subject to change. Past performance is not indicative of future results and no representation is made regarding future performance of the Funds. No person guarantees the performance of any funds managed by Harbour Asset Management Limited.

Harbour Asset Management Limited (Harbour) is the issuer of the Harbour Investment Funds. A copy of the Product Disclosure Statement is available at https://www.harbourasset.co.nz/our-funds/investor-documents/. Harbour is also the issuer of Hunter Investment Funds (Hunter). A copy of the relevant Product Disclosure Statement is available at https://hunterinvestments.co.nz/resources/. Please find our quarterly Fund updates, which contain returns and total fees during the previous year on those Harbour and Hunter websites. Harbour also manages wholesale unit trusts. To invest as a wholesale investor, investors must fit the criteria as set out in the Financial Markets Conduct Act 2013.

Important disclaimer information

| « Are equity markets due for a strong finish this year? | ChatGPT, the Magnificent Seven, Ozempic, and Higher-for-longer » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |