Has the corporate bond market partied too hard?

Financial markets over the last few years have enjoyed the equivalent of a “long hot summer” characterised by calm weather and warm sunny days. From experience, we all know that long hot summer days can occasionally encourage excess in the form of too much sun or fun. The same excess is also a risk for financial markets and the wider economy.

Friday, February 1st 2019, 8:00AM

by Mark Brooks

Mark Brooks

Locally the good times are obvious in the number of cranes on the skylines of our major cities and in the difficulty of finding staff. The United States is also seeing similar capacity constraints as labour market surveys show there are more job openings than there are unemployed.

There is a saying that financial bull markets do not die of old age. Instead, they end due to a combination of capacity shortages constraining growth and central banks increasing interest rates to counter the risk of rising inflation.

In the United States this process in now well under way as the Federal Reserve has raised interest rates eight times already and will probably do so again in December. Higher interest rates have tightened monetary conditions in the United States and globally. This squeezes those in a weaker position, primarily those with excessive debt loads and/or economically sensitive incomes. During the Global Financial Crisis this was predominately households in the United States and in New Zealand, non-bank lenders such as finance companies.

This time round, a key area of stress is likely to be the corporate bond market. A decade of ultra-low interest rates forced many investors out of cash as it did not generate a return into other investment assets. Much of this money flowed into the corporate bond market. Globally, companies were more than happy to accommodate this demand by issuing bonds at historically low interest rates. In the United States, this has seen the corporate bond market double in size over the past decade to more than $5 trillion.

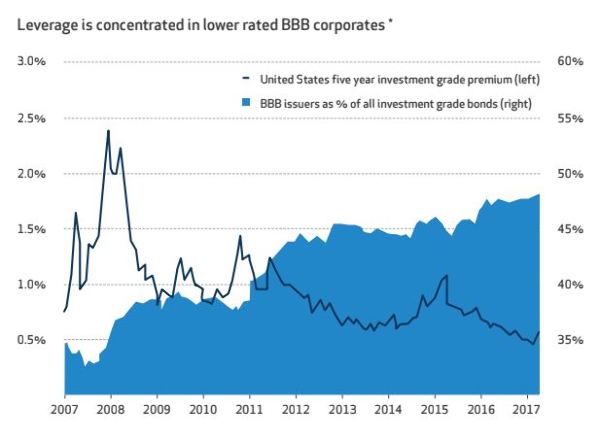

Initially the bond issuance was used to replace higher cost debt with cheaper funding but as the cycle continued, companies have increasingly used this as an opportunity to borrow aggressively to fund the purchase of their own shares. Excessive buybacks can leave a company with more debt to repay and no new sources of revenue with which to repay it. Many of the bonds used to fund buybacks have been issued by companies at the lower end of the investment grade spectrum: BBB rated bonds rather than A rated bonds (BB, B and CCC rated bonds are not considered investment grade). BBB rated bonds now account for over 48% of the United States investment grade bond universe, up from 34% at their low 10 years ago.

The pattern in New Zealand is different as we have not seen companies increase their debt levels to the same degree. However, companies have increasingly issued bonds to replace bank debt, issue subordinated debt and remove investor friendly terms from their bond documents. This makes these bonds more exposed to any slowing in the economy. In a slowing economy the combination of declining earnings and rising debt costs will see interest coverage erode and make the BBB investment grade bond universe look shaky.

At this point the reaction for many investors will be to sell these bonds. This can be more challenging for bonds. Unlike shares, the secondary market for bonds is limited and this is especially true in New Zealand. It is easy to buy a bond when it is first issued, but more difficult to sell the same bond before it matures. We therefore anticipate the markets may struggle to absorb this selling without a significant re-pricing. In anticipation of this, we have substantially reduced clients' exposure to lower quality investment grade bonds and have invested in downside mitigation strategies that are designed to limit the impact of a downturn in investment grade bonds.

* Source: International Monetary Fund. Barclays Capital. Tse Capital.

Mark Brooks is Head of Income at New Zealand Funds Management Limited (NZ Funds). His opinions are personal, and do not necessarily reflect the position of NZ Funds. Mark’s advice is of a general nature, and he is not responsible for any loss that any reader may suffer from following it.

| « Booster adds to wine portfolio | KiwiSaver funds suffer under market volatility » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |